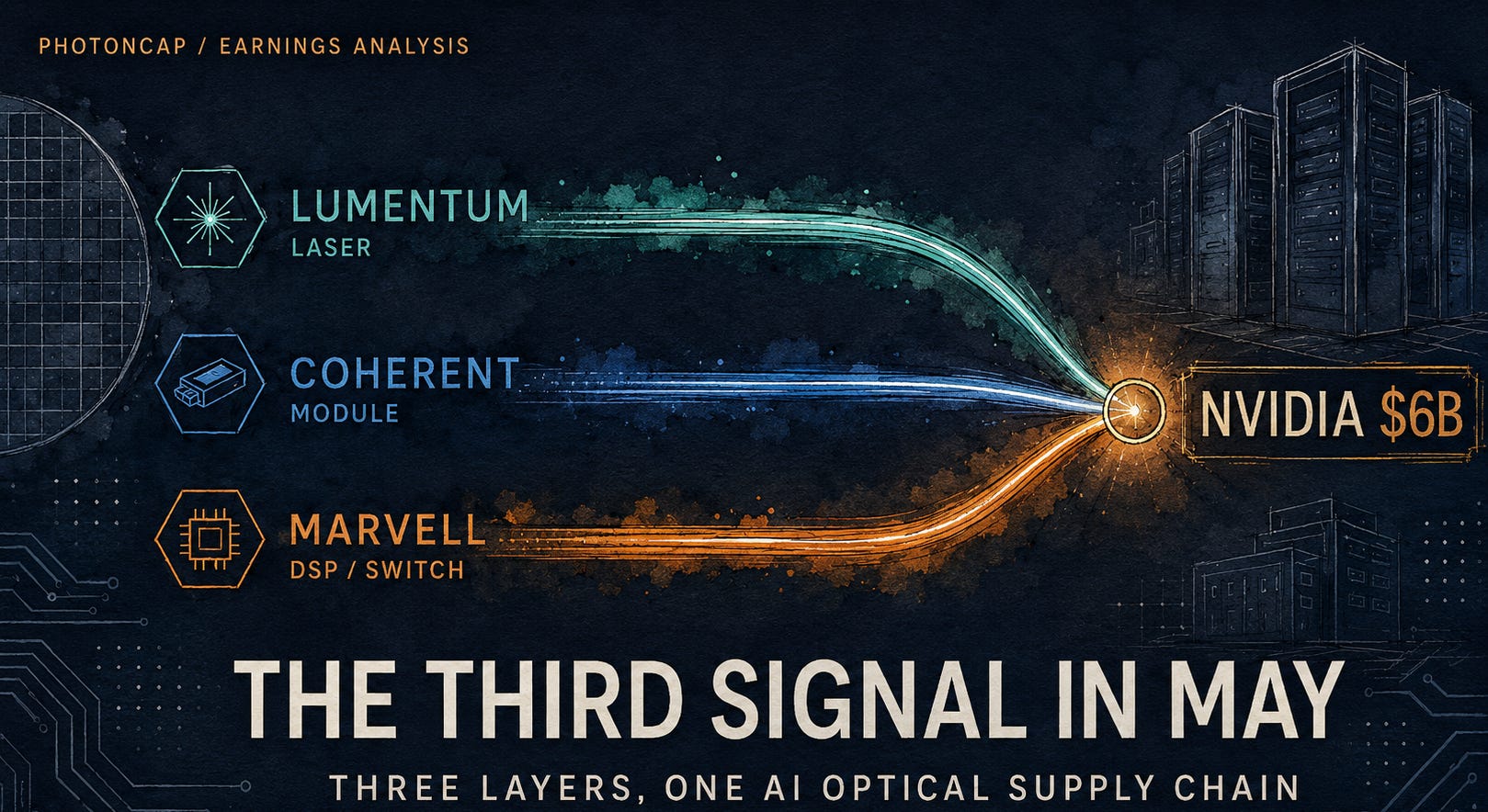

The Third Signal in May: Marvell Confirms the AI Optical Signal from Lumentum and Coherent

$MRVL $COHR $LITE | Interconnect Earnings + Supply Chain Layers from Laser to Foundry

Over a single month in May, the same demand signal emerged from three layers of the AI optical supply chain. Laser source (Lumentum, 5/5), transceiver/CPO (Coherent, 5/6), DSP/switch/SiPh (Marvell, 5/27). All three companies raised their forward demand visibility for AI optical interconnects, and all three secured $2B strategic commitments from the same counterparty: NVIDIA. Marvell posted Q1 FY27 revenue of $2.418B (+28% YoY), raised its interconnect growth outlook from +50% to +70%, and lifted FY28 revenue guidance to $16.5B, a $1.5B increase. This article analyzes the Marvell earnings while mapping why all three earnings paint the same picture, and where each company and layer sits within that picture.

Contents

Abstract

Three Signals in One Month

Marvell Q1 FY27: The Numbers

Why Interconnect: Scale-Out, Scale-Up, Scale-Across

Marvell Interconnect: Why +50% Became +70%

Custom Silicon and Switching

Cross-Validation of Three Earnings: Same Demand, Different Layers

Supply Chain Layer Map: Beneficiary Positioning

SiPh Foundry Layer: Who Actually Fabricates Silicon Photonics?

Polariton and LWLG: The Boundary of Modulator Physics

Scenario Analysis

Monitoring Points

PhotonCap’s View

References & Sources

Three Signals in One Month

On May 5, Lumentum reported earnings. 200G EML revenue doubled sequentially. Narrow linewidth laser revenue grew +120% YoY for the ninth consecutive quarter. Pump laser revenue grew +80% YoY, and optical components across the board were described as sold out. CPO ultra-high-power lasers showed ramp/PO visibility for the first half of 2027. And NVIDIA invested $2B. [1]

The 8 Companies Behind Lumentum’s $808M Quarter: Why Beta Splits by Orders of Magnitude Across the InP Cycle

Quarterly revenue $808.4M, +90% YoY. Lumentum reported FY26 Q3 earnings after market close on May 5, 2026. 200G EML revenue doubled in a single quarter, narrow linewidth laser posted its ninth consecutive quarter of sequential growth at +120% YoY, and Q4 guidance of $960M to $1,010M puts the upper bound above $1B for the first time. This single earnings print transmits across four layers of the InP supply chain (substrate, MOCVD/MBE epi tool, epi service, laser chip OEM) and into five distinct company groups (pure-play substrate, pure-play epi service, multi-segment tool, lower-beta adjacent, internal capture), each receiving a dramatically different magnitude of beta. The same earnings headline produced +297% in one layer, +50% in another, and +5,000% in yet another. This article analyzes the structure of that asymmetry.

The next day, Coherent reported. OCS TAM guidance was raised to over $4B, CPO incremental TAM to over $15B. InP 6-inch wafer production capacity was being doubled by the following quarter, with plans to more than double again by CY27. The prior quarter had already shown datacenter book-to-bill exceeding 4x, and Q3 expanded the backlog to record levels with order visibility extending to CY28. NVIDIA invested another $2B here as well, with multi-year purchase commitments and capacity access rights for advanced laser and optical networking products. [2]

$20B+ New SAM on Top of +27% Pro Forma Revenue: The Quarter Coherent Crossed from Transceiver Player to Platform

Coherent reported Q3 FY26 revenue of $1.806B, +27% YoY on a pro forma basis, an acceleration from the prior quarter. This was not a routine beat-and-raise. It was the quarter the company re-declared its SAM at $50B+ by CY2030, layered onto a +$20B+ incremental category that was not part of its previous framing. Compared with Lumentum’s +90% YoY in the same quarter, the two companies look like fundamentally different bets on the same industry cycle. This article walks through segment mix shift, the 8-quarter +530bps gross margin trajectory, the “one quarter ahead of plan” InP capacity signal, the actual structure of the NVIDIA $2B deal, and the $20B+ new SAM that re-positions Coherent as a platform rather than a transceiver pure-play.

Then, on May 27, Marvell reported Q1 FY27 earnings.

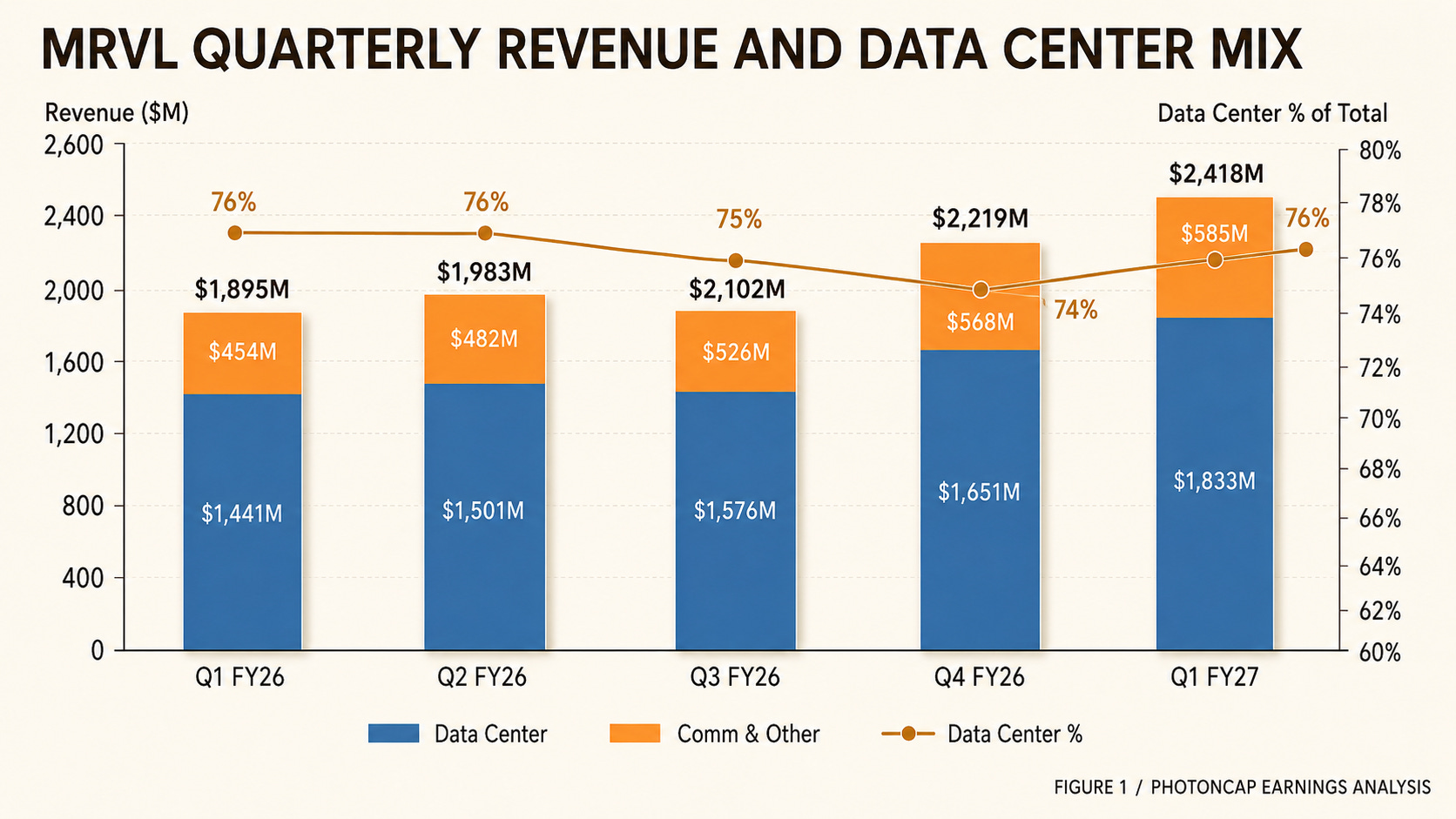

Revenue $2.418B. Up +28% year over year, $18M above the midpoint of guidance. Data center revenue $1.833B, representing 76% of total. Non-GAAP EPS $0.80, up +29% YoY. Operating cash flow $639M, a company record. [3]

The numbers alone are a solid beat. But what actually mattered in this report was not the results themselves.

It was the scale of the guidance raise.

Q2 revenue guidance of $2.7B. More than $100M above the $2.6B consensus. Full-year FY27 revenue outlook raised to roughly $11.5B, up more than $500M from the prior quarter. FY28 raised to $16.5B, up $1.5B from the previous outlook. [4]

And the core driver behind this raise was interconnect. FY27 interconnect growth outlook moved from +50% to +70%. In CEO Matt Murphy’s words: “We are seeing exceptional AI-related bookings.” [4]

NVIDIA invested $2B here too. Optics partnership, NVLink Fusion integration, AI RAN. [3][5]

Within a single month, the same signal emerged from three layers. The laser source company reported capacity constraints. The transceiver company reported record backlog and order visibility extending into CY28. The DSP/switch company raised its interconnect growth rate by 20 percentage points. And all three were pulled into NVIDIA’s $6B optical supply-chain blueprint.

This is not a simple demand confirmation. It is a structural signal that NVIDIA is aligning the entire optical interconnect supply chain around its own platform architecture. In the early GPU ramp, advanced node and CoWoS bottlenecks dominated the conversation. In the inference/scale-up phase, the optical interconnect supply chain is becoming part of the platform architecture itself.

If three earnings are painting the same picture, it is not coincidence. It is structure.

Coherent, Lumentum, Marvell, and Now Corning: NVIDIA’s 4 Photonics Bets and the Path of Light

NVIDIA made four direct investments into photonics companies in 2026. Coherent and Lumentum got $2B each on March 2, Marvell got $2B on March 31, and on May 6 Corning got a $500M warrant deal plus a multi-year commercial partnership. The first three sit in the transceiver, laser, and DSP layers, the companies that generate, control, and interface with light. The fourth one, Corning, makes the medium that light actually travels through: optical fiber, cable, and connectors. This article walks through why NVIDIA’s fourth bet went to a different layer, and why the connectivity layer matters as much as the transceiver layer.

Marvell Q1 FY27: The Numbers

Before diving into the analysis, here are the Q1 numbers.

Q1 FY27 revenue came in at $2,418M, up +28% from $1,895M a year ago and +9% from $2,219M the prior quarter. Data center revenue was $1,833M (YoY +27%, QoQ +11%), and Communications & Other was $585M (YoY +29%, QoQ +3%). Non-GAAP gross margin was 58.9% (prior quarter 59.0%, year-ago 59.8%), non-GAAP operating margin was 35.0% (prior quarter 35.7%, year-ago 34.2%). Non-GAAP EPS was $0.80 (YoY +29%, QoQ flat). Operating cash flow hit $639M, a company record, up +92% from $333M a year ago and +71% from $374M the prior quarter. [3]

[Figure 1: Marvell Quarterly Revenue and Data Center Mix Trend]

Data center now accounts for 76% of revenue, more than three-quarters of the total. Marvell has crossed the threshold where investors should analyze it primarily as an AI infrastructure company.

Cash flow stands out. The $639M record operating cash flow is nearly double the year-ago figure of $333M. Cash on hand sits at $3.84B, reflecting the Celestial AI + XConn acquisitions ($1.27B) and the $2B preferred stock issuance to NVIDIA. [3][4]

Non-GAAP gross margin of 58.9% dipped slightly from 59.0% the prior quarter and is 90bp below the year-ago 59.8%. This is a mix effect from growing custom silicon share. Management noted that “product mix will remain key determinants of our gross margin.” [3]

The Guidance Raise: Pay Attention to the Magnitude

The most important part of this earnings report is not the results, but the size of the forward guidance increase.

FY27 revenue outlook moved from roughly $11B to roughly $11.5B, up $500M. FY28 moved from roughly $15B to $16.5B, up $1.5B. Data center growth rates were raised from roughly 40% to roughly 50% YoY for FY27, and FY28 was newly guided at roughly 55% YoY. Interconnect growth moved from +50% to +70% for FY27, and FY28 custom went from “double” to “more than double.” [4]

In a single quarter, the FY28 revenue outlook went up by $1.5B. That is the entire annual revenue of most mid-cap semiconductor companies.

Most of this raise came from data center, and within that, from interconnect. Data center revenue grew +46% in FY26, is projected at +50% for FY27, and +55% for FY28. The growth rate is not just rising. It is accelerating. [4]

Q2 guidance of $2.7B also beat the $2.6B consensus, and Q3 is already expected to hit $3B. Murphy said he expects “at least 10% sequential growth in Q2, Q3, and Q4.” Marvell has entered a phase where quarterly revenue is stepping up 10% QoQ. [4]

FY28 non-GAAP operating margin is expected to reach the upper end of the 38% to 40% target range, while non-GAAP opex growth is projected at mid-to-high teens, well below the 45% revenue growth rate. This is the phase where operating leverage starts to show up in real numbers. [4]

Supply chain investment is aggressive. Marvell plans $1B in supply-chain prepayments during FY27, sharing its demand forecast with suppliers and backing it with cash to secure capacity. COO Christopher Koopmans noted that “we have not been in an unconstrained environment since 2020.” [4]

Acquisitions moved fast as well. Celestial AI (photonic fabric, EAM modulator) and XConn (scale-up switching) both closed in February. Polariton Technologies (plasmonic silicon photonics) was acquired in April. All three acquisitions are directly tied to interconnect. [4]

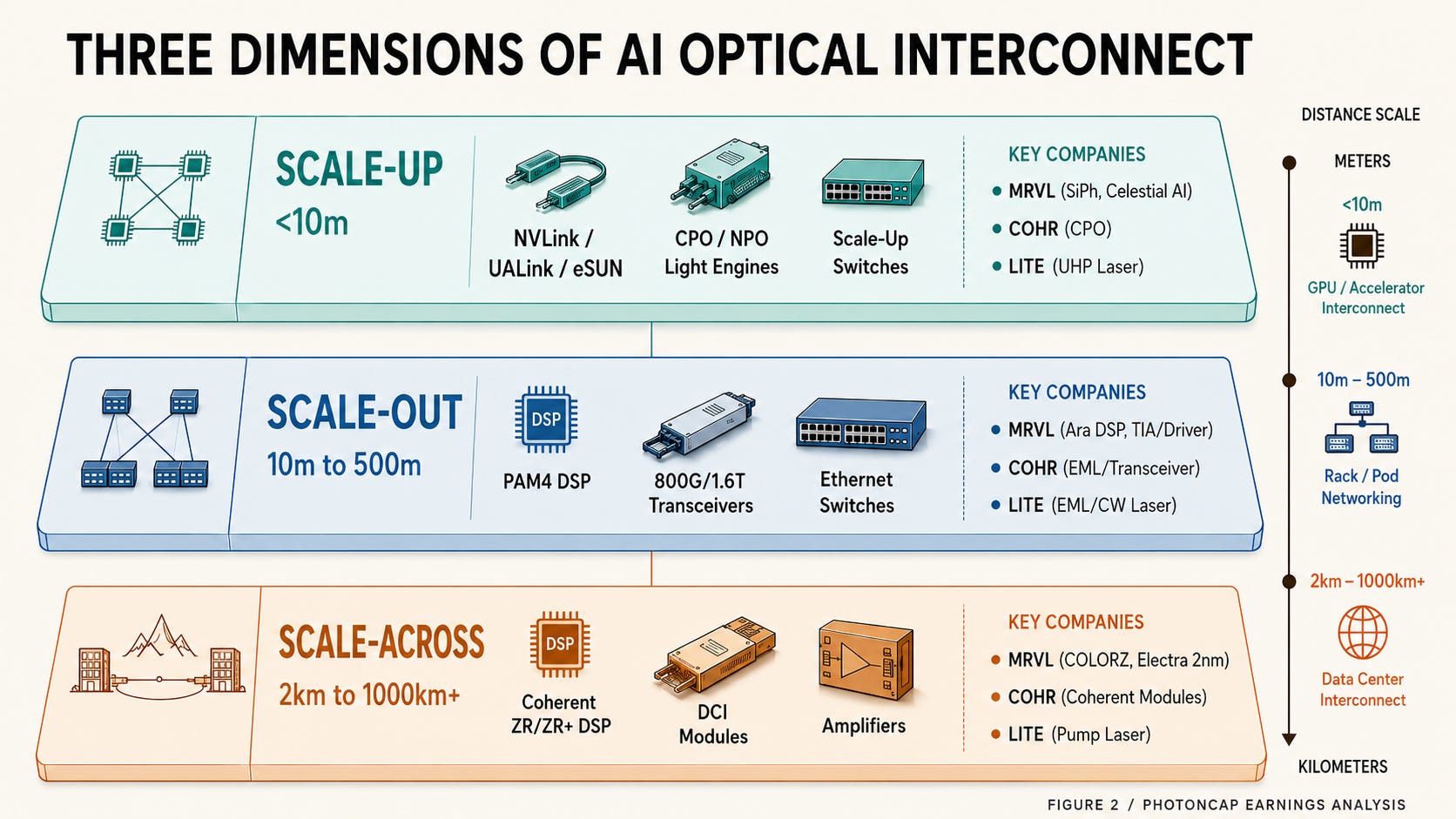

Why Interconnect: Scale-Out, Scale-Up, Scale-Across

To understand Marvell’s guidance raise, you need to understand how AI data center network architecture is changing. We analyzed the three scaling dimensions in detail in a previous PhotonCap article, “NVIDIA’s $2B Marvell Bet and Celestial AI’s ‘25x Bandwidth’ Claim: What’s the Denominator?”, and we carry the same framework forward here.

In the early days of AI, compute and memory were the bottleneck. More GPUs, faster HBM. But as complex workloads like reasoning models, mixture-of-experts, and Agentic AI have emerged, the bottleneck has shifted to networking. [4]

Three dimensions of interconnect are expanding simultaneously.

Scale-out: Server-to-server connectivity. Traditional Ethernet-based. Transitioning from 800G to 1.6T. Marvell’s PAM4 DSPs and Coherent/Lumentum transceivers go here.

Scale-up: GPU/XPU-to-GPU/XPU connectivity within a single compute domain. Protocols like NVLink, UALink, and eSUN. This is the primary battleground for CPO (Co-Packaged Optics) and NPO (Near-Package Optics). Coherent’s CPO modules, Lumentum’s ultra-high-power lasers, and Marvell’s SiPh light engines all target this market.

Scale-across: Data center to data center connectivity. When AI clusters span multiple buildings due to power and space constraints, the backend AI network must extend across buildings too. DCI (Data Center Interconnect) modules are the key product here, and Marvell is leading with integrated coherent DSP + module solutions. [4]

[Figure 2: Scale-Out / Scale-Up / Scale-Across Architecture and Component Map]

What matters is that optical interconnect share is rising across all three dimensions. Scale-out sees higher optics ASP from the 800G/1.6T transition. Scale-up is hitting copper’s bandwidth ceiling, making optical solutions essential. Scale-across is optical by nature.

Matt Murphy put it this way: “It is increasingly clear that optics is the future of data center connectivity.” [4]

And the supply chain building this optical connectivity stack is exactly what reported through three consecutive May earnings calls. Lumentum makes the lasers. Coherent makes the transceivers. Marvell makes the DSPs and switches.

The emergence of Agentic AI is an additional demand accelerator. According to Murphy, in traditional 1-shot inference a single query hits an AI model once. In Agentic AI, a single user request triggers multiple agents querying AI models multiple times across different parts of the AI cluster. Data traffic volume, reach distance, and latency requirements all go up. Across scale-out, scale-up, and scale-across simultaneously. CPU deployment also increases, pulling NIC, PCIe switch, and retimer demand along with it. [4]

This is not simply a story about “optical demand is strong.” The direction of AI workload evolution itself is consuming optical bandwidth structurally.

The question is which layers within this supply chain capture how much of the benefit. Even within the same cycle, beta differs by layer. Even within the same layer, the beneficiary path diverges by technology choice.

What the three earnings confirmed is the existence of demand. What needs to be analyzed next is how that demand distributes across each layer of the supply chain, and who holds what position within it. When Marvell’s interconnect guidance rose from +50% to +70%, which sub-segments drove those 20 percentage points? How does Lumentum’s EML capacity constraint affect Marvell’s DSP shipments? Are Coherent’s CPO ramp and Marvell’s SiPh light engine targeting the same market or different ones? These are the questions.

The Wafer That Used to Roll Around My Lab Is Now an AI Data Center Bottleneck: Soitec and the Investment Case for the Photonics-SOI Monopoly

As AI data centers accelerate the transition from electrical to optical interconnects, demand for SOI (Silicon-on-Insulator) wafers, the critical substrate for silicon photonics (SiPh), is growing rapidly. This article analyzes Soitec’s (EPA: SOI) technological moat (3,500+ Smart Cut patents, no competitor with meaningful Photonics-SOI volume identified from public sources), financial profile (FY2025 revenue of €891M, Photonics-SOI approaching €100M scale), and the reality behind the SiN platform threat narrative. Soitec’s stock rallied from its December 2025 low of €23 to €78 as of April 15, 2026, a YTD gain of +213%, as the market began pricing in its SiPh/CPO positioning. But the actual Photonics-SOI revenue scale-up is still in its early innings. The real test comes over the next 2 to 3 years as 1.6T/CPO ramps accelerate. Related tickers: $SOI (EPA), $SLOIF (OTC), $GFS, $TSEM

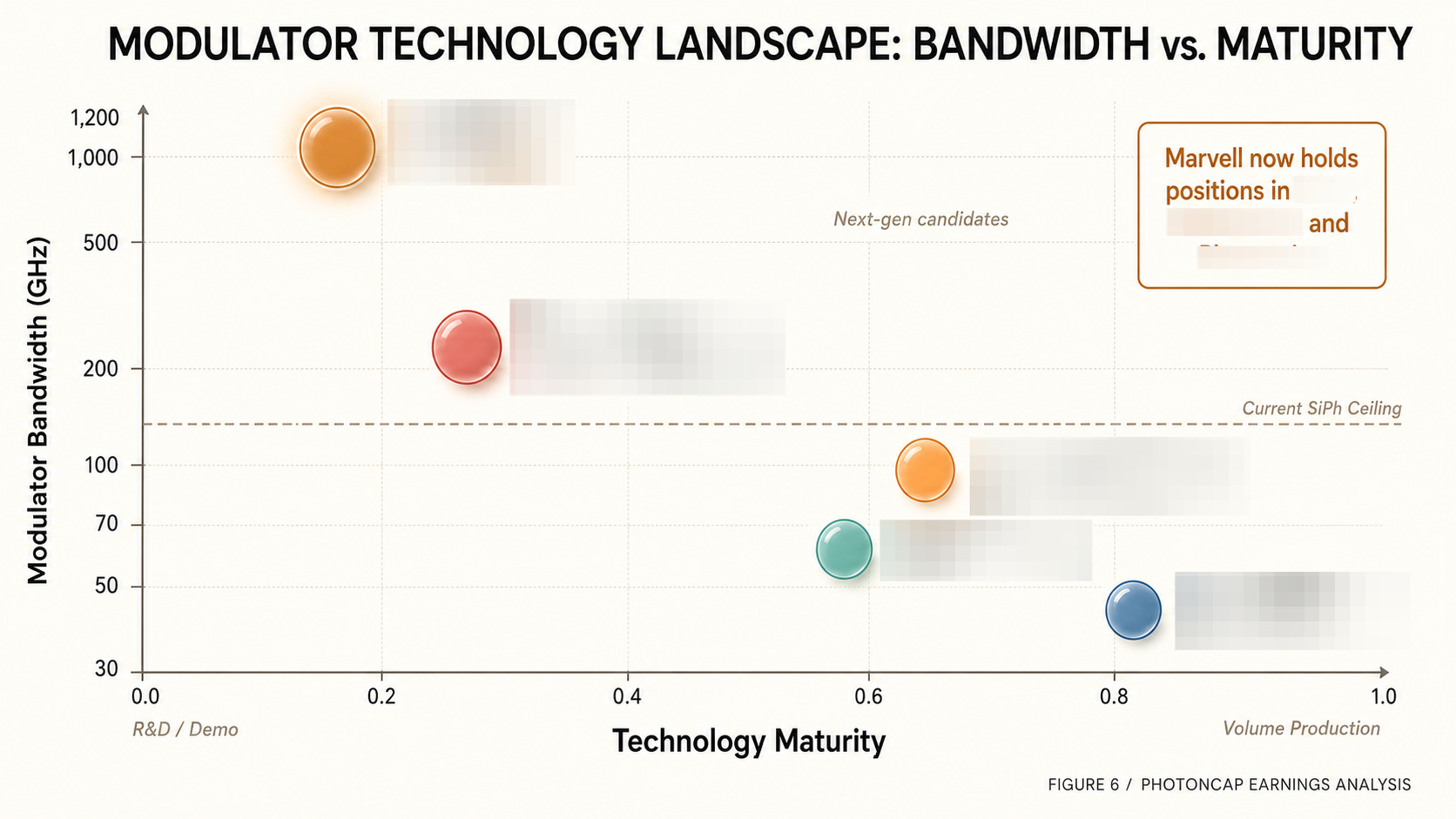

One more thing. Polariton Technologies, which Marvell acquired in April, makes plasmonic-based modulators. Modulator bandwidth exceeding 1THz, 10x that of conventional SiPh. This is technology that surpasses the physical bandwidth ceiling of current silicon photonics modulators (roughly 70 to 120GHz), and there is another company trying to solve the same problem with different physics. The structure of this competition and its investment implications are analyzed in detail in the paid section.

We also cover the foundry layer that actually fabricates SiPh chips. GlobalFoundries, TSMC, Tower, X-FAB, UMC, and Samsung are competing for SiPh platform dominance, and when CPO/NPO deploys at scale, this foundry layer could become a new supply chain bottleneck. X-FAB’s Microsystems & Photonics revenue hit +42% YoY to an all-time high, and its stock recently surged. These foundries’ SiPh platform choices also affect the technology strategies of downstream customers like Marvell, Broadcom, and Celestial AI. The technical differences and competitive dynamics across foundries are mapped in the paid section.