The 8 Companies Behind Lumentum’s $808M Quarter: Why Beta Splits by Orders of Magnitude Across the InP Cycle

$LITE Q3 FY26 Earnings + InP Substrate / Epi / Laser Chip Supply Chain Analysis ($AIXA.DE, $VECO, $IQE.L, $AXTI, $ALRIB.PA, $OXIG.L, $COHR)

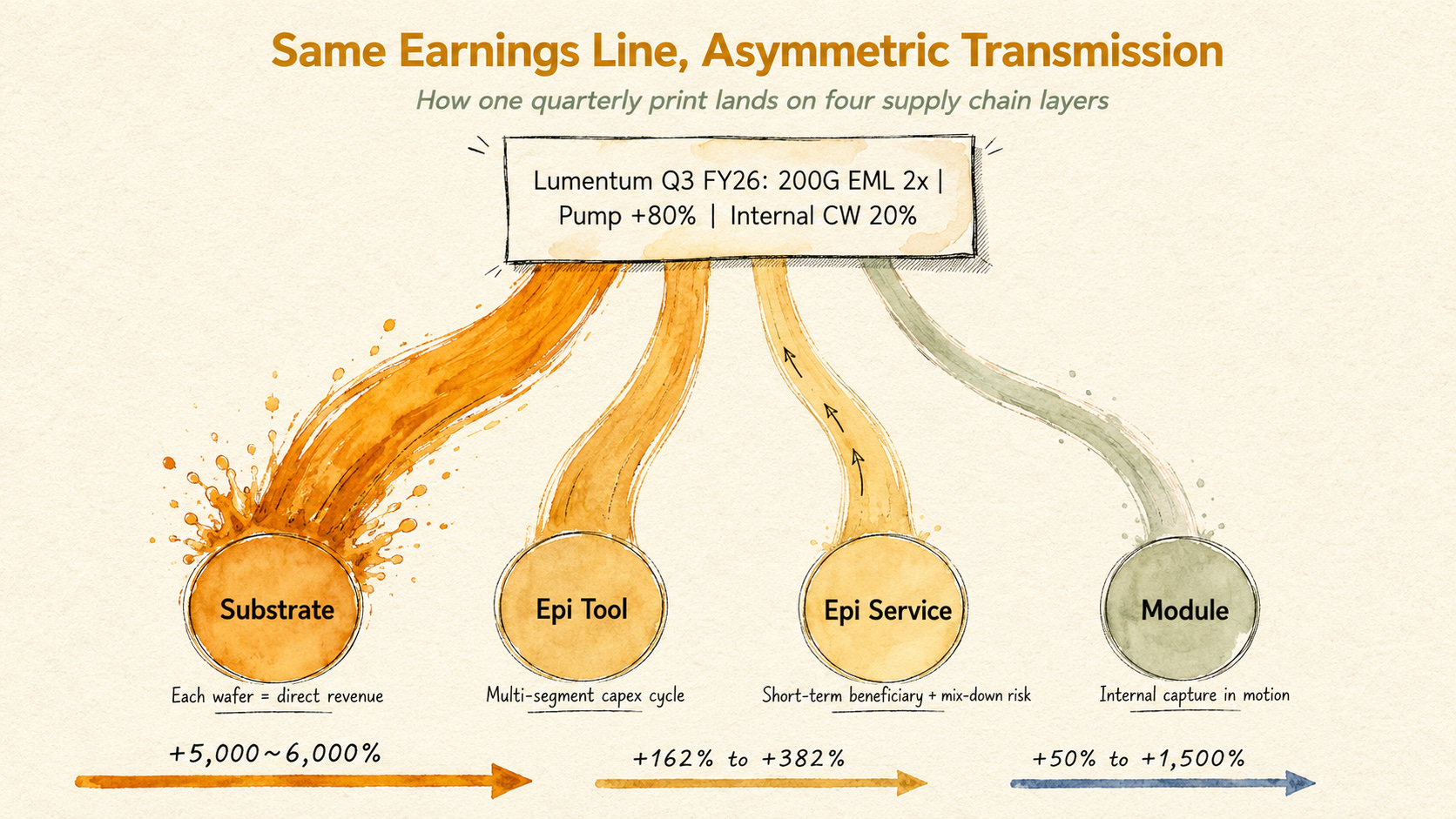

Quarterly revenue $808.4M, +90% YoY. Lumentum reported FY26 Q3 earnings after market close on May 5, 2026. 200G EML revenue doubled in a single quarter, narrow linewidth laser posted its ninth consecutive quarter of sequential growth at +120% YoY, and Q4 guidance of $960M to $1,010M puts the upper bound above $1B for the first time. This single earnings print transmits across four layers of the InP supply chain (substrate, MOCVD/MBE epi tool, epi service, laser chip OEM) and into five distinct company groups (pure-play substrate, pure-play epi service, multi-segment tool, lower-beta adjacent, internal capture), each receiving a dramatically different magnitude of beta. The same earnings headline produced +297% in one layer, +50% in another, and +5,000% in yet another. This article analyzes the structure of that asymmetry.

Contents

Intro: What $808M in a Quarter Means

Five Key Signals from Lumentum’s Earnings

What OFC 2026 Showed Six Weeks Earlier

The Structure of the InP Cycle: Why All Five Signals Move the Entire Supply Chain

Five Groups, and One Unexpected Company

Company Identification + Large-Cap Comparison

Five-Group Classification + Differentiation + Company Analysis

Scenarios + Monitoring + Closing

References

1. Intro: What $808M in a Quarter Means

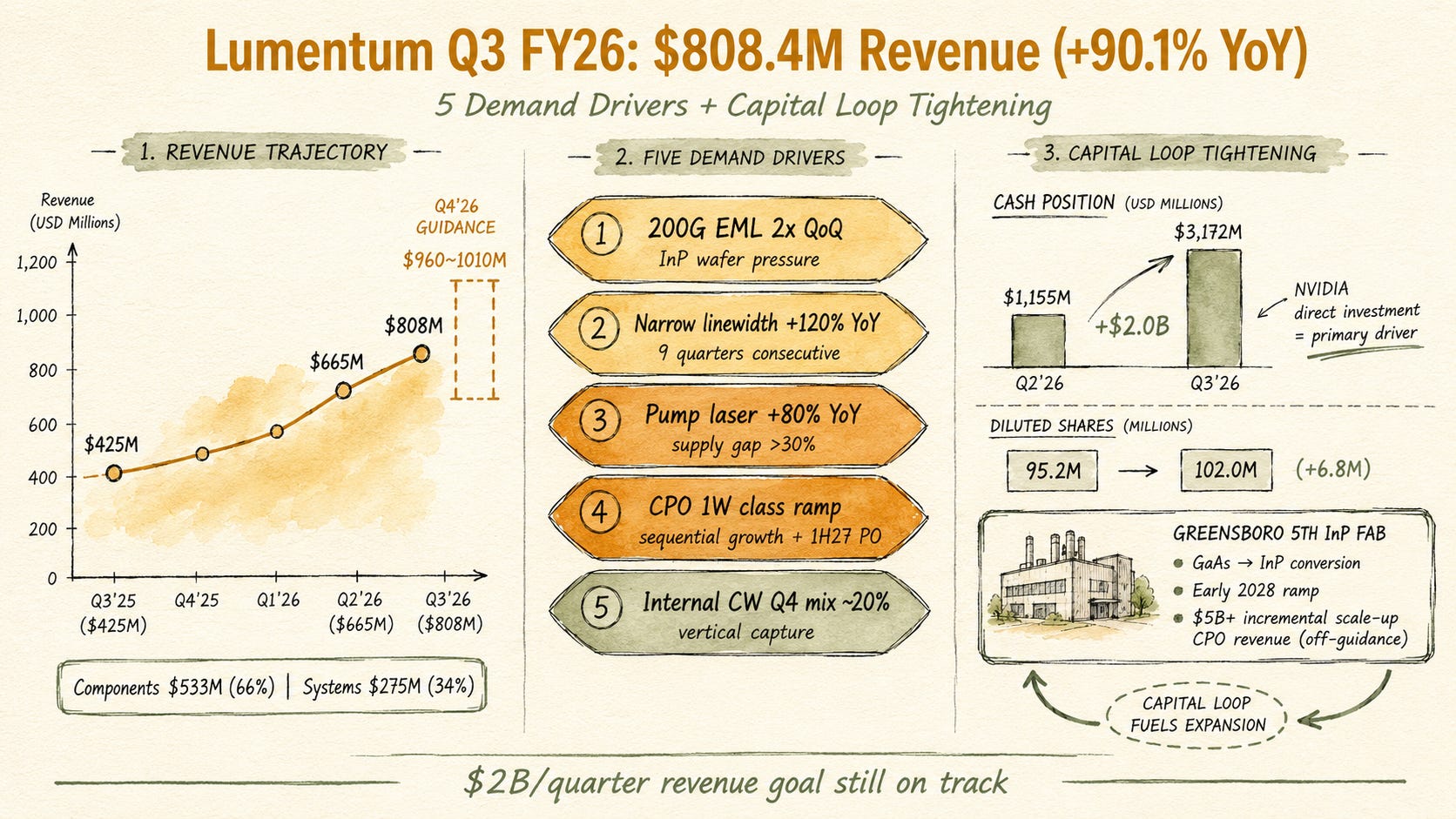

Quarterly revenue $808.4M, +90.1% YoY. After market close today, Lumentum (NASDAQ: LITE) reported FY26 Q3 results [1].

Revenue: $808.4M (+90.1% YoY), near the top of $780M to $830M guidance

Non-GAAP EPS: $2.37, exceeding the $2.15 to $2.35 guidance range

Non-GAAP OPM: 32.2% (+700bps QoQ)

Q4 Guidance: Revenue $960M to $1,010M (upper bound crosses $1B for the first time), OPM 35% to 36%, EPS $2.85 to $3.05

As of writing, LITE closed at $1,002.65 with a market cap of $71.55B (May 5, 2026, Robinhood) [2]. The trailing one-year stock return is approximately +1,500% [3]. However, in after-hours trading following the earnings release, LITE dropped to around $940 (roughly -6%) before recovering to the $975 range (author’s direct observation, May 5, 2026 PT). EPS and Q4 guidance came in strong and revenue landed near the top of guidance, but the stock reacted first to sell-the-news dynamics and dilution concerns. The significance of this pattern will be revisited in the company analysis section.

What makes this number interesting is that it is not just a Lumentum story. Lumentum doubling its 200G EML quarterly revenue means the InP wafer area carrying those EMLs came under strong pressure. EML integrates a DFB laser section and an EAM section on a single chip, so die-area burden and epi/process/test complexity trend higher than for a simple CW DFB laser. When revenue doubles on top of that structural complexity, wafer-start and epi capacity both face simultaneous pressure. That said, ASP, yield, and die-size mix all interact, so revenue growth and wafer utilization growth do not map 1:1. The same single earnings headline therefore sends a message simultaneously to the companies that make InP wafers, the companies that deposit epi on those wafers, the companies that sell MOCVD and MBE tools, and the companies that OEM laser chips on top of it all.

But that message does not arrive at the same magnitude everywhere. One layer responded at +297%. Another at +50%. Another surged to +5,000%. This asymmetry is the starting point for this article.

[Figure 1: Lumentum Q3 FY26 earnings at-a-glance. Segment ($533M / $275M) + 5 drivers + capital flow ($1.16B to $3.17B with Greensboro 5th InP fab)]

2. Five Key Signals from Lumentum’s Earnings

According to the press release and supplemental presentation [1][5], five drivers powered this quarter.

(1) 200G EML quarterly revenue doubled in a single quarter. Both 100G and 200G EML hit record quarterly shipments, with 200G EML revenue more than doubling sequentially. This matters beyond the headline number because of EML’s structural complexity. EML integrates a DFB laser section and an EAM section on a single chip, so die-area burden and epi/process/test complexity trend higher than for a simple CW DFB laser. Doubled EML revenue therefore signals strong pressure on InP wafer-start and epi capacity, though ASP, yield, and die-size mix prevent a 1:1 conversion from revenue growth to wafer utilization growth. In the earnings call, Hurlston added another data point: EML units are on a trajectory to increase 50% or more in the December 2026 quarter compared to December 2025 [25]. The sequential doubling is a QoQ number; the +50% is a YoY base. Both point to strong pressure on InP wafer area. Q3 laser chip shipments themselves doubled year over year. Japanese wafer fab capacity is fully allocated and trading at premium pricing. Critically, the company had disclosed a 30%+ EML supply gap in the prior quarter call, and this quarter acknowledged the gap has widened [25]. Wafer fabs running at double the rate still cannot keep up with demand.

(2) Narrow linewidth laser posted nine consecutive quarters of sequential growth, +120% YoY. And Lumentum introduced a new category: “scale-across.” Narrow linewidth lasers go into coherent transponders and DCI (Data Center Interconnect) applications, all built on InP DFB lasers. In the call, Lumentum bundled narrow linewidth and pump lasers into a scale-across category. This is the third axis after scale-out (more lanes per transceiver) and scale-up (intra-rack link intensification): when hyperscalers hit the power and space limits of a single building and move to multi-building distributed architecture, scale-across provides the high-bandwidth synchronization infrastructure. Narrow linewidth lasers deliver the precision needed for 1.6T speeds and higher-order modulation, pump lasers handle multi-rail optical amplification, and WSS (Wavelength Selectable Switch) manages traffic routing. The company stated this category is the largest contributor to gross and operating margin expansion [25]. The +120% YoY therefore connects directly to the +700bps QoQ OPM jump to 32.2%.

(3) Pump laser revenue grew +80% YoY, and this is where the strongest supply signal emerged. Pump lasers are III-V laser components used in EDFAs (Erbium-Doped Fiber Amplifiers) and inline optical amplifiers, with material mix varying by wavelength. 980nm pumps typically use GaAs/AlGaAs/InGaAs Fabry-Perot structures, while 1480nm pumps use InGaAsP/InP. Rather than mapping +80% entirely to InP wafer beta, the accurate read is that scale-across plus subsea optical amplification cycles are pressuring the broader III-V laser supply chain. Hurlston acknowledged in the call that pump laser supply constraints are more severe than EML constraints, and that this gap emerged as unanticipated [25]. The company has reached the stage of turning away customer orders. Multi-rail architecture acts as a multiplier for pump laser content. Lumentum plans to ramp pump capacity at the Rose Orchard facility in phased steps over the next four quarters [25], with output step-up velocity faster than EML. This is less a datacenter cycle and more a telecom backbone plus AI scale-across cycle accelerating simultaneously.

(4) CPO (Co-Packaged Optics) ultra-high-power CW laser at the 1W class entering production. Laser chip ramp is already in sequential growth. CEO Hurlston stated in the press release that meaningful revenue begins “exiting CY 2026” [1]. The earnings call went further: CPO ultra-high-power laser chip manufacturing ramp already entered sequential growth in fiscal Q3, and the company has begun fulfilling multi-hundred-million-dollar purchase orders for 1H 2027 delivery [25]. This is not “revenue will come” but “revenue is already ramping sequentially.” Simultaneously, the ELS (External Laser Source) module format is being developed as a turn-key solution for multiple CPO customers. Hurlston specified that for non-primary customer engagements, the ELS module is the key entry point [25]. Output doubled in one year: 400mW (2025) to 800mW SHP / 1W class (2026) [11]. CPO ultra-high-power laser chip manufacturing ramp is already in sequential growth, with December quarter meaningful revenue and 1H 2027 multi-hundred-million-dollar PO fulfillment proceeding on schedule [25]. Above that, the second layer of vertical integration (laser to ELS module) is in progress.

(5) 1.6T transceiver Q4 ramp plus internal CW laser integration already started in fiscal Q3. This is the most important single line. The supplemental (p.3) notes that 1.6T transceiver Q4 FY26 ramp will proceed alongside early-stage internal CW laser integration [5]. The call went further: Lumentum already began supplying its own CW lasers to some of its cloud transceivers in fiscal Q3, with approximately 20% of Q4 guidance transceiver mix using internal CW lasers [25]. The trigger for this internal capture is revealing. The original plan was to introduce internal lasers in calendar Q2 2026, but EML line tightness forced a delay. This time, external CW laser supply also tightened, prompting re-acceleration of internal conversion [25]. Internal capture is not purely a margin optimization strategy; it is also a response to external supply pressure. This inflection directly affects supply chain distribution.

Capital structure also shifted significantly. The balance sheet shows a large footprint [5].

Cash and short-term investments: Q2 $1,155M to Q3 $3,172M (+$2,017M)

Shareholder’s Equity: Q2 $847M to Q3 $2,973M (+$2,126M)

Q4 guidance diluted shares: 95.2M to 102.0M (+6.8M)

Cash increased approximately $2B in a single quarter. CFO Wajid Ali identified the primary driver in the call: NVIDIA’s direct investment [25]. This is not market inference but an official company disclosure. Simultaneously, approximately 7M additional shares are projected in Q4 guidance. Where this capital goes was also clarified: a fifth InP fab in Greensboro, North Carolina was acquired in mid-March, converting an existing GaAs facility to InP [25]. Some existing tools can be reused. Ramp timing is early 2028, and this capacity is incremental to current guidance numbers. Hurlston specified additional revenue potential of $5B or more in incremental scale-up CPO revenue [25]. On top of the quarterly $2B target, a separate capacity layer is being prepared.

The call also reaffirmed the quarterly $2 billion revenue goal, articulated at OFC and still on track [25]. That is approximately 2.5x the current $808M quarter. With the Greensboro fab’s $5B+ incremental scale-up CPO revenue potential stacked on top, the company’s multi-year trajectory is a three-stage ramp structure: current quarter to $2B quarterly to additional CPO scale-up layer.

The strongest emphasis throughout was on supply control. Lumentum disclosed that long-term agreements for substrate have already been secured [25]. The 30%+ supply gap for EML and pump lasers sits within the company’s control envelope (capacity ramp), while substrate (external wafer purchases) is locked in via LTA. For supply chain companies, this is a significant signal: LTAs at this stage involve prepayment, take-or-pay, and volume plus price floor structures [25], meaning external substrate and epi companies are moving toward multi-year revenue and margin visibility. Counterparties were not disclosed, but the pattern is structural to the entire InP supply cycle, not unique to a single company.

One-line summary of Q3 FY26: The external supply cycle for InP-based optical components is accelerating, while Lumentum simultaneously begins pulling that InP demand internally. And the ramp trajectory toward quarterly $2B is already being locked in at the contractual layer. These three dynamics happening concurrently are the starting point for supply chain analysis.

3. What OFC 2026 Showed Six Weeks Earlier

The five drivers from this quarter were actually previewed six weeks earlier at OFC 2026 (Los Angeles, March 16 to 19) in portfolio form. OFC General Chair Tetsuya Hayashi (Sumitomo Electric) summarized in the wrap-up: “1.6T moving closer to real-world deployment across the AI networking ecosystem” [10].

Lumentum demonstrated a 1.6T DR4 OSFP pluggable transceiver prototype at OFC 2026, using four 400G differential EML lasers [11]. At the same booth (#1439), an 800mW SHP (Super-High-Power) laser was announced: 1310nm device delivering over 1W optical output at 25C, 800mW+ at 50C, less than 100kHz linewidth, greater than 40dB SMSR. A 16-channel DWDM UHP laser source was also demonstrated in an ELSFP (External Laser Source Form Factor Pluggable) module, with 200 GHz grid centered at 1310nm, approximately 24 dBm per channel, CW-WDM MSA compatible [11]. Lumentum explicitly used the phrase “advanced components, world-class packaging, and high-volume manufacturing expertise,” signaling production-stage readiness rather than R&D demonstration. Output progressed from 400mW UHP laser (2025) to 800mW SHP / 1W class (2026): a 2x jump in one year reaching production stage.

Coherent demonstrated its 1.6T transceiver portfolio at the same OFC across four platforms simultaneously: SiPh PIC + high-power InP CW laser + 200G InP EML + 200G GaAs VCSEL [12]. A 6.4T slot CPO was demonstrated using an in-house high-power InP CW laser external light source. A new 12.8T XPO MSA form factor was announced (12.8Tbps liquid-cooled module, rack-level 204.8Tbps front-panel density). One additional development stands out: a 400G InP modulator running on silicon [12]. This signals hybrid integration of InP modulators onto SiPh platforms. SiPh is not unidirectionally replacing InP; InP is extending into the SiPh modulator domain in a bidirectional coupling. This paradox will be revisited in the scenario analysis.

OFC 2026’s portfolio started transmitting into earnings revenue this quarter, Q3 FY26. This is the commercial-stage entry signal for the InP cycle.

4. The Structure of the InP Cycle: Why All Five Signals Move the Entire Supply Chain

Let’s step back and address the basics. Why does AI optical networking require InP, and why do all five drivers above converge on a single InP wafer?

InP is the active material that directly generates light in optical communications. Silicon has an indirect bandgap and cannot efficiently produce light. Datacenter transceivers operating at 1.3 and 1.55 micrometer wavelengths therefore build their EMLs and CW DFB lasers almost entirely on InP wafers [4]. Short-reach VCSELs at 850nm and 940nm use GaAs, and SiPh transceivers process their modulators on silicon, but the light source still depends on an external InP CW laser. Every layer in an optical transceiver that produces light sits on III-V compound semiconductors.

The key to this cycle is the transition from 4-inch to 6-inch InP wafers. Simple arithmetic gives approximately 2.25x the area, but when edge exclusion, automation, usable area, and yield improvements are included, a single wafer yields four times or more devices under the same process. This was stated in Coherent’s March 2024 announcement [7] and Oxford Instruments’ November 2025 release [8]. Die cost drops 60% or more. The 6-inch transition therefore creates a multi-year greenfield capex cycle for deposition tool companies: 4-inch era tool sets cannot handle 6-inch production.

Mapping Lumentum’s five drivers onto this structure:

(1) 200G EML quarterly revenue doubled signals strong pressure on InP wafer-start and epi capacity. EML integrates a laser and modulator on one chip, so die area, process complexity, and yield sensitivity can all increase relative to CW DFB. Direct beneficiaries include InP substrate companies (such as AXT), InP epi companies, and epi tool companies (such as Aixtron MOCVD).

(2) Narrow linewidth laser +120% YoY feeds the same InP DFB layer.

(3) Pump laser +80% YoY spans III-V more broadly (GaAs/AlGaAs/InGaAs or InGaAsP/InP depending on wavelength). This pressures the broader III-V supply chain rather than mapping directly to InP wafer beta alone.

(4) CPO ultra-high-power CW laser, CY26 revenue start is InP DFB CW laser. If CPO adoption accelerates, EML-centric InP demand could be reallocated toward CW laser and ELS architectures. However, if absolute transceiver volumes grow faster, total InP wafer demand continues to increase. The separation of absolute demand from per-unit demand begins here.

(5) Lumentum internal CW laser integration maintains InP wafer demand but shifts it from external InP suppliers to Lumentum’s internal operations. Coherent is moving in the same direction. CEO Anderson stated in the Q2 FY26 call that “internal indium phosphide sourcing [will] increase as a proportion of total supply” [9]. Coherent has ramped 6-inch InP lines at Sherman, Texas and Yarfalla, Sweden to 80% of target capacity, maintaining external partnerships for supply resilience and customer requirements while increasing internal share [9].

Lumentum Driver Direct Beneficiary Indirect Beneficiary Potential Displacement 200G EML doubled InP substrate, InP epi, MOCVD tool Etch/depo tool (none) Narrow linewidth laser InP substrate, InP epi MOCVD tool (none) Pump laser III-V substrate (GaAs + InP), III-V epi, MBE/MOCVD tool (none) (none) CPO CW laser CY26 InP substrate, InP epi, MOCVD tool ELS / packaging EML-heavy demand mix (long-term) Internal CW integration Lumentum/Coherent in-house InP (none) External InP epi service

[Figure 2: InP supply chain 4-layer diagram (substrate, epi tool/service, laser chip OEM, transceiver/module). Asymmetric arrows showing different beta thickness per layer.]

The same earnings headline arrives as “absolute volume surge” in one layer, “internal capture signal” in another, and “CPO transition signal” in yet another. This is the starting point for why beta splits by orders of magnitude.

5. Five Groups, and One Unexpected Company

Everything up to this point is visible by following Lumentum’s earnings release and publicly available 6-inch InP transition data. The consensus already recognizes that the AI optical cycle is an InP cycle. The real question is: where in the supply chain is the strongest beta right now?

The real differentiation starts here. Within the same InP supply chain, one-year stock returns range from +50% to +5,000%, splitting by orders of magnitude. Beta per layer has been completely different since the AI optical cycle began in 2024.

This asymmetry is not simply a matter of “which company is better.” It is a matter of the same cycle transmitting through layer structure with different multiple effects. Five distinct groups form:

Pure-play InP volume beta (substrate): nearly 100% exposure to a single layer. Every wafer directly becomes revenue.

Pure-play epi service: an external III-V epi foundry exposed to a single layer. Short-term upside and mix-down risk coexist.

Multi-segment beneficiary: InP is a portion, but other cycles (LED legacy, power, quantum, advanced packaging) are simultaneously strong. Combined capex tool cycle beta.

Lower-beta adjacent: deposition/etch tools where InP/photonic mix is small, diluting beta.

Internal capture (winner side): the layer pulling external supply internally. This becomes mix-down risk for some external suppliers.

Among these five groups, one contains a company paradoxically exposed to the most direct mix-down risk. The Lumentum plus Coherent internal integration signal is simultaneously good news and bad news for that company. This is the entry point for this article.

This is the boundary of what earnings data and public disclosures can show. How the same cycle splits into orders-of-magnitude-different beta, which companies belong to which group, who the real internal capture card is, who faces mix-down exposure, and where each group’s valuation currently stands requires sorting the data layer by layer.