$20B+ New SAM on Top of +27% Pro Forma Revenue: The Quarter Coherent Crossed from Transceiver Player to Platform

$COHR $LITE | Q3 FY26 Earnings Deep Dive

Coherent reported Q3 FY26 revenue of $1.806B, +27% YoY on a pro forma basis, an acceleration from the prior quarter. This was not a routine beat-and-raise. It was the quarter the company re-declared its SAM at $50B+ by CY2030, layered onto a +$20B+ incremental category that was not part of its previous framing. Compared with Lumentum’s +90% YoY in the same quarter, the two companies look like fundamentally different bets on the same industry cycle. This article walks through segment mix shift, the 8-quarter +530bps gross margin trajectory, the “one quarter ahead of plan” InP capacity signal, the actual structure of the NVIDIA $2B deal, and the $20B+ new SAM that re-positions Coherent as a platform rather than a transceiver pure-play.

Table of Contents

The Quarter in One Read

Why InP / EML Has Been the Cap on the Industry

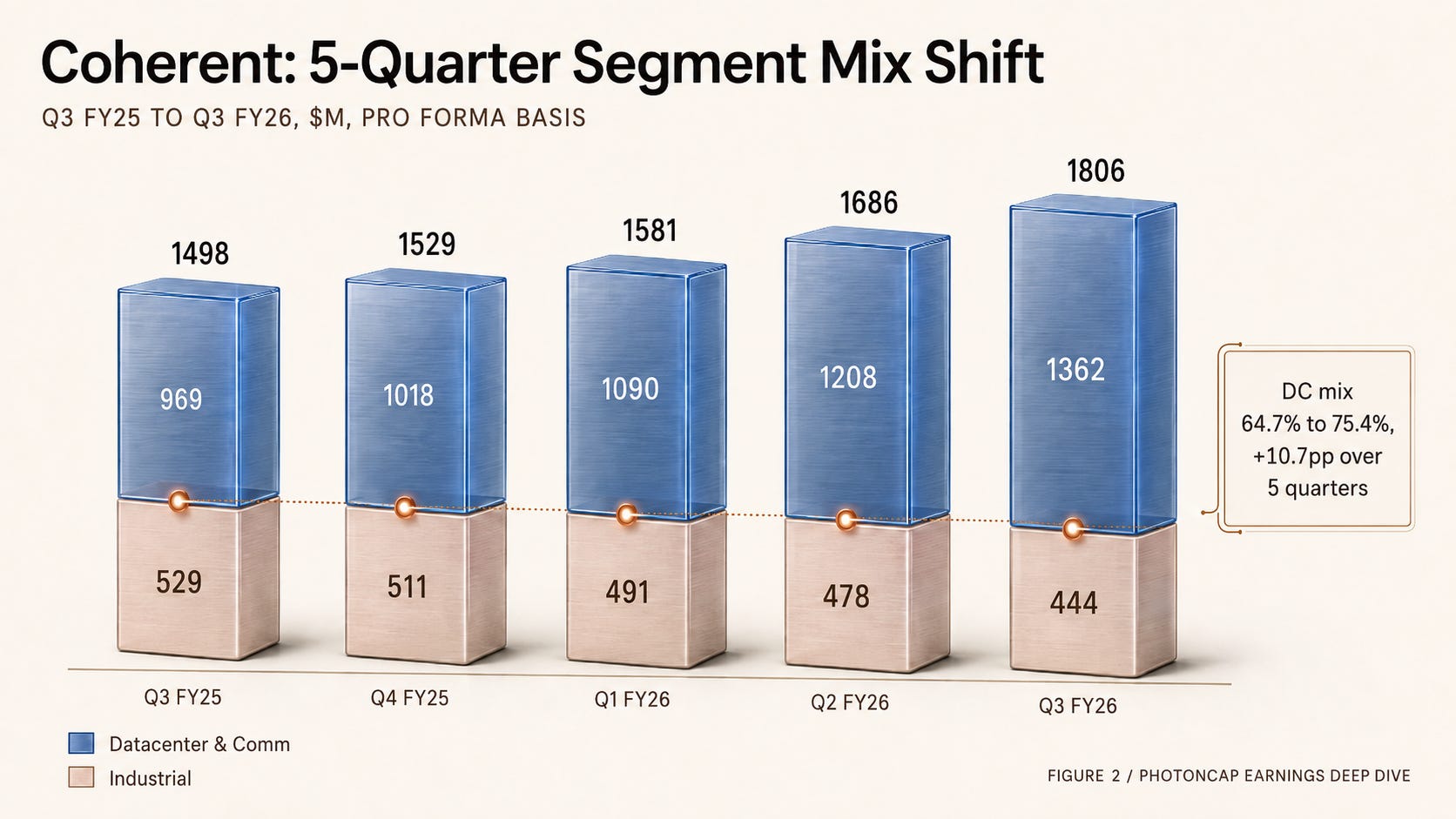

Segment Decomposition: Industrial Shrinks, Revenue Still Grows +21%

Margin Trajectory: What Happened Over 8 Quarters

“One Quarter Ahead of Plan”: The Supply Layer Signal

The Actual Structure of the NVIDIA $2B Deal: COHR vs LITE

What the $50B+ SAM Declaration Says About Platform Re-positioning

COHR vs LITE: Same NVIDIA $2B, Different Companies

InP Substrate Supply Chain: The Sumitomo, AXT-Tongmei, JX 6-inch Race

Broader Implication: The Optical Layer NVDA Locked In Within Two Months

Q4 FY26 Guidance, Scenarios, and Monitoring

Closing

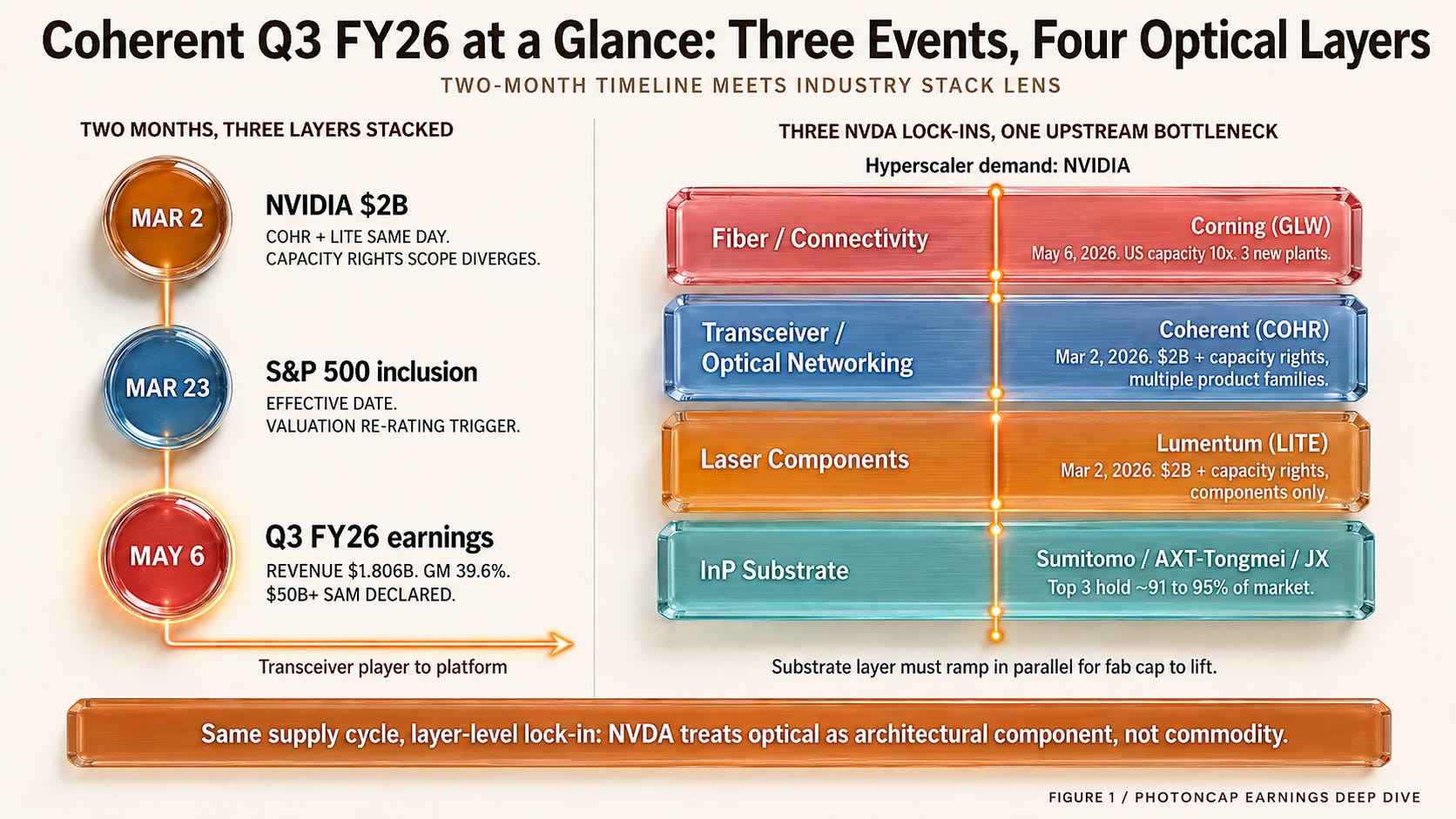

[Figure 1: Hybrid Overview - Event Timeline + Industry Stack]

The Quarter in One Read

On May 6, after market close, Coherent (NYSE: COHR) reported Q3 FY26 (March quarter).

Revenue $1.806B (GAAP +20.5% YoY, pro forma +27% YoY, +7.1% QoQ) [1]

Non-GAAP gross margin 39.6% (+105bps YoY, +530bps cumulative over 8 quarters) [1]

Non-GAAP diluted EPS $1.41 (vs $0.91, +55% YoY) [1]

Datacenter & Communications segment $1,362M (+41% YoY) [2]

Industrial segment $444M (-16% YoY) [2]

Q4 FY26 guidance: Revenue $1.91B to $2.05B (midpoint +9.5% QoQ), Non-GAAP EPS $1.52 to $1.72 [1]

This is not a single event quarter. Three different layers stacked up within two months.

March 2: NVIDIA announced a $2B equity investment in Coherent, a multi-year multi-billion-dollar purchase commitment, and future capacity rights on advanced laser and optical networking products [3]

March 23: COHR joined the S&P 500 [4]

May 6: Q3 earnings, with revenue acceleration, 105bps GM expansion, and a 1.6T transceiver ramp guide

The three layers operate on different axes. The NVDA deal locks in forward demand visibility, S&P 500 inclusion is a valuation re-rating trigger, and the earnings print is revenue realization. Most earnings calls weaken when any one of these is missing. This quarter had all three.

Lumentum (LITE) reported the same March quarter one day earlier, with $808.4M in revenue, +90.1% YoY [5]. The two companies are roughly 2x apart in absolute revenue, but LITE’s growth rate is more than 3x. And both received a $2B NVIDIA equity investment.

So the question is why the two companies that both received NVDA $2B had such different quarters, and what Coherent’s platform re-positioning actually means. That is the spine of this article.

Why InP/EML Has Been the Cap on the Industry

To understand this quarter, the location of InP/EML inside the AI optical stack matters.

Optical connectivity in AI datacenters depends on the laser source inside the transceiver. As lane speed scales from 800G to 1.6T to 3.2T, EML (Electro-absorption Modulated Laser), an InP-based laser, becomes the gating component. Moving from 100G/lane to 200G/lane does not increase EML count inside the same 8-lane configuration. What increases is the device-level burden: bandwidth, extinction ratio, yield requirement, and test complexity. Unit demand scales with optical lane count and transceiver volume, while lane speed raises the difficulty and cost per EML.

Concretely, an 800G transceiver typically uses 8 lanes x 100G, while 1.6T uses 8 lanes x 200G or 4 lanes x 400G. In an 8-lane 1.6T transceiver, 8 EMLs are required. The EML count itself is proportional to the optical lane count per transceiver. Lane speed is not a multiplier on EML count. Going from 100G to 200G per lane does not add EMLs to the same 8-lane configuration. What increases is the modulator bandwidth, extinction ratio, yield requirement, and test burden on each EML device. On top of that, transceiver count per hyperscaler datacenter scales with GPU rack count. EML unit demand scales multiplicatively with (lanes per transceiver x transceiver count), while the spec and cost burden per EML rises as a separate function of lane speed.

The constraint is that EML/InP has been globally supply constrained. In compound semiconductors, InP has smaller wafer size than GaAs or Si (traditionally 3-inch) and higher crystal defect density, so yields are low. The way to unlock it is the migration to 6-inch InP wafers, which is the technical inflection point where yield and throughput improve together.

Why 6-inch is an inflection. Wafer area scales with the square of diameter, so moving from 3-inch to 6-inch gives roughly 4x more potential die per wafer. Coherent has explicitly stated in IR materials that 6-inch lines run at higher yields than 3-inch lines [2]. Actual good die uplift depends on device layout, edge exclusion, defect density, and line maturity. Since wafer processing time does not scale linearly with die count, per-die cost falls in a step function. In compound semiconductors, this kind of wafer size migration resets the capacity curve for the entire industry once it happens.

Coherent is ramping 6-inch InP device / platform production across three sites: Sherman (Texas), Järfälla (Sweden), and Zürich (Switzerland). Lumentum is constructing a new InP fab in Greensboro [5]. Note that bulk InP substrate supply itself sits in a separate upstream layer that requires supplier qualification and committed supply. Both companies have spent the past year repeating the same message on earnings calls: demand is there, capacity is not. PhotonCap’s earlier Lumentum FY26 Q3 piece (on InP supply chain beta transmission) focused on the cap itself. This COHR quarter is the moment that cap visibly starts to lift.

The 8 Companies Behind Lumentum’s $808M Quarter: Why Beta Splits by Orders of Magnitude Across the InP Cycle

Quarterly revenue $808.4M, +90% YoY. Lumentum reported FY26 Q3 earnings after market close on May 5, 2026. 200G EML revenue doubled in a single quarter, narrow linewidth laser posted its ninth consecutive quarter of sequential growth at +120% YoY, and Q4 guidance of $960M to $1,010M puts the upper bound above $1B for the first time. This single earnings print transmits across four layers of the InP supply chain (substrate, MOCVD/MBE epi tool, epi service, laser chip OEM) and into five distinct company groups (pure-play substrate, pure-play epi service, multi-segment tool, lower-beta adjacent, internal capture), each receiving a dramatically different magnitude of beta. The same earnings headline produced +297% in one layer, +50% in another, and +5,000% in yet another. This article analyzes the structure of that asymmetry.

In this Q3 earnings call, the single most important line from Coherent is this.

“On track to double internal InP output by year-end and more than double again by 2027” [2]

It sits on slide 6 of the investor presentation. On the earnings call, management reportedly commented that this doubling is roughly one quarter ahead of the original plan (call commentary, transcript-based).

In an industry where InP supply was the cap, supply ramping faster than plan does not mean “we built too much, who will buy it.” It means orders are stacked beyond capacity. Demand visibility did not pull supply visibility forward. The opposite happened. Demand was already there, and revenue recognition is paced by how fast supply unlocks.

This connects to LITE’s +90% YoY. Both companies are riding the same supply tailwind in the same window. LITE has a smaller starting revenue base and a near pure-play datacenter portfolio, so the same supply unlock shows up as a larger YoY percentage. COHR has revenue more than 2x LITE’s, and it is also simultaneously divesting its Industrial-adjacent businesses, so the headline growth rate looks lower. On a pro forma basis at +27% YoY, COHR actually accelerated from the prior quarter. Both are different expressions of the same cap lifting.

The difference is in starting size and segment structure, and more importantly, in how each company frames its own SAM. Both received NVIDIA $2B equity, but the COHR deal has a line that does not appear in the other company’s announcement. That single line is what re-positions COHR from a transceiver player to a platform company this quarter.

One additional point worth raising. In the same quarter, NVDA went beyond COHR and LITE. On May 6, the same day as COHR’s earnings, NVDA announced a multi-year commercial and technology partnership with Corning, including 10x expansion of US optical connectivity capacity and three new plants in North Carolina and Texas. Within two months, NVDA placed simultaneous commitments across three layers of the optical stack: EML / laser (LITE), transceiver / networking (COHR), and fiber / connectivity (Corning). This is not a single-company bet. It is a layer-level supply lock-in pattern.

One layer deeper still is the InP wafer substrate layer. COHR runs 6-inch InP device / platform production across Sherman, Järfälla, and Zürich, while LITE is expanding Greensboro. Bulk InP substrate wafer itself is sourced from upstream suppliers under separate qualification and committed supply arrangements. The global InP wafer market is extremely concentrated, with the top three (Sumitomo Electric, AXT / Beijing Tongmei, JX Advanced Metals) holding roughly 91 to 95% of the market depending on the source. AXT itself has already been the subject of two PhotonCap deep dives. Part 1, “AXT Inc. (AXTI) Deep Dive: The Hidden Bottleneck in AI Optical Interconnects“ (March 2, 2026), mapped the InP supply chain and AXT’s vertical integration. Part 2, “A Company With $88M in Annual Revenue Just Got a $6B Market Cap: What AXTI’s Q1 Changed, and What It Didn’t“ (May 4, 2026), examined Q1 results (InP revenue $13.6M, +70% QoQ, GM 29.9% with a 36pp YoY swing, backlog $100M+) and the asymmetry between narrative and valuation. This COHR quarter shows how the same industry cycle connects from fab level back to substrate level.

The 6-inch race carries two implications for the broader cap. First, the period when EML / InP supply was the binding constraint is in the process of unwinding. Second, the industry is entering a phase where multiple layers of the stack (substrate, epi, processing, module) can ramp in parallel, not just one company at a time. For the ramp curve from 1.6T to 3.2T and 6.4T to remain unbroken, both fab-side ramp at COHR / LITE and substrate-side ramp at Sumitomo / AXT-Tongmei / JX have to function together. COHR’s “one quarter ahead” signal suggests substrate supply has not yet become an immediate blocker for its fab-side ramp, though it does not by itself prove that the industry-wide substrate ramp is fully on schedule.

Optical exposure can no longer be valued as a single transceiver multiple. Layers with capacity rights attached have to be separated from layers without. What differs across stocks is which layer a company sits in, whether it is inside a named NVDA deal scope, and whether the portfolio is pure-play or platform. The company-level breakdown sits past the paywall.

[Figure 2: COHR 5-quarter segment revenue mix shift]

So far: Q3 earnings headlines (+27% pro forma, +55% EPS), the shared supply-unlock signal across both companies, the framing that the same NVDA $2B landed differently in the two companies, the pattern that NVDA placed simultaneous commitments across three optical layers (COHR + LITE + Corning) within two months, and the substrate-level Top 3 supplier structure.

From here: COHR’s 5-quarter segment decomposition, the two drivers behind the 8-quarter +530bps gross margin trajectory, the actual scope difference inside the NVDA $2B “capacity rights” clause (LITE’s OCS backlog is not named inside the disclosed NVDA deal scope), the 6 new growth engines under the $50B+ SAM declaration with their specific timing, the Sumitomo + AXT-Tongmei + JX 6-inch race quantitative comparison, how the broader thesis propagates to adjacent optical companies, and a quantitative COHR vs LITE scorecard with Q4 guidance scenarios.