Compute Is the New Oil. So Who Builds the Drilling Rigs?

$FORM $AEHR $KEYS $TER $AIXA $VECO | The supplier-agnostic layer where compute financialization concentrates beta

In the same month, CME and ICE both announced compute futures tied to GPU rental rate indices, and compute began turning into a cash-settled exchange commodity.[1][2] Put SpaceX’s Cursor acquisition, the Oracle-OpenAI $300B/4.5GW deal, and Microsoft-OpenAI’s end of exclusivity in one frame, and the unit the market prices is shifting from chip ASP to contracted compute.[3][4][5] The thesis here is simple. Contracting GW eventually translates into wafer starts one layer down, and no matter who wins at the chip and compute layer, the supplier-agnostic layer everyone passes through is deposition, etch, bonding, probe, burn-in, ATE, and metrology. If compute is oil, part of the money is made not at the oilfield but in the rigs that drill it and the tools that inspect it.

($NVDA $ORCL $MSFT $CME / $FORM $AEHR $KEYS $TER $ATEYY $AIXA $VECO $ALRIB $OXIG $IQE $AXTI)

Intro: The Exchanges List Compute

The same exchanges that trade crude, corn, and bitcoin are now moving to list compute. In May, CME partnered with Silicon Data to announce compute futures based on a GPU on-demand rental rate index, set to launch later this year and pending regulatory review.[1] The contracts are cash-settled rather than physically delivered, and days later ICE brought its own GPU futures based on Ornn’s Compute Price Index, so the two largest exchanges moved the same way in the same week.[2] CME called compute the new oil of the 21st century.[1]

The phrasing may sound large, but when an exchange attaches a forward curve to an asset, that is the market admitting the asset has become a commodity big and volatile enough to need hedging. And this admission did not come from nowhere. The unit had been shifting for the better part of a year.

Last September, Oracle signed a five-year, $300B, 4.5GW deal with OpenAI, where the unit was not a count of chips but gigawatts.[4] A month later, Microsoft gave up its right of first refusal as OpenAI’s compute provider while still securing an incremental $250B Azure commitment.[5] And this June, days after its IPO, SpaceX acquired Anysphere, the parent of the AI coding tool Cursor, in a $60B all-stock deal.[3] It did not buy a chip company. It bought an application that consumes compute and turns it into revenue. The three share one thing. The price tag is no longer written in chip ASP. It is written in contracted compute.

The market still reads this change as a story about GPUs, cloud, and power infrastructure. But the moment compute lists on a futures market, the real question shifts from “who sells the GPU” to “who holds the bottleneck in compute production.” From that angle, a layer of equipment and test sits below NVIDIA, below cloud, and further inside than power. This article looks for the beta in that lower layer.

That lower layer is the deeper sublayer of what I covered as Layer 3, Ground AI Compute, in The Largest IPO in History, One Profitable Layer. In that piece I flagged this layer as the one with the weakest SpaceX uniqueness among the four, because the upside in GPU, power, cooling, and optical interconnect belongs not to SpaceX alone but to all of AI capex. The constraint the S-1 named for ground AI was also power, cooling, and land. This article goes one step below that, to the manufacturing and test equipment layer that turns compute into actual chips and optical engines. Whether the final winner is SpaceX, OpenAI, or Oracle, or NVIDIA or a custom ASIC, the winner’s identity is not the key variable for this layer. The point is that as long as compute capacity grows, everyone passes through this physical production layer. That industry-wide upside has to land somewhere. This article starts there.

Takeaway: An exchange attaching futures to GPU rental rates and big tech contracting compute by the gigawatt are two faces of the same event. The unit the market prices is moving from the chip to compute capacity.

Buying GW Means Buying Wafers

Move down one layer. Compute capacity is not an abstract number but a physical quantity. A gigawatt is roughly the deployed silicon area times power density. Some of the demand compresses through performance (node scaling), but what scaling cannot compress, volume has to carry. One accelerator is area on a wafer, and laying down more accelerators raises wafer starts.

So Oracle’s 4.5GW deal, viewed one layer down, is a wafer starts deal, and Microsoft’s $250B Azure commitment and the compute SpaceX wants to fill by combining xAI and Cursor all converge on the same place.[4][5] At the chip and model layer, whether NVIDIA wins, a custom ASIC wins, or xAI wins, all of them pass through the same manufacturing capacity.

Compute financialization also speeds this up. The exchanges describe the futures market as a way to give data centers price protection.[2] Once a forward curve exists, GW buildout becomes bankable, easier financing means faster expansion, and faster expansion means more wafer starts. The fact that this buildout is currently supply-constrained by material and labor shortages, with reports of some Oracle-linked OpenAI data centers slipping toward 2028 even as Oracle says its contractual milestones remain on track,[6] is exactly what makes price protection through a forward curve meaningful. Making compute a commodity grows demand for the equipment that produces that commodity.

A familiar analogy fits here. An oil price can be hedged with futures, but the rigs and oilfield services that pull the oil are not hedged, they absorb the cycle directly. It is the same setup as the gold rush, where the person selling pickaxes made steadier money than the person digging for gold. So where is compute’s pickaxe, compute’s drilling rig?

Takeaway: Contracted compute translates one layer down into wafer starts. And compute financialization makes buildout bankable, which amplifies that translation. No matter who wins the chip war, there is a supplier-agnostic manufacturing layer everyone passes through.

This Much Anyone Can Map

Everything so far is routing you can draw from public material alone. Compute became a commodity, GW comes down to wafer starts, and below that sits a supplier-neutral manufacturing layer. Anyone who reads the headlines can reach this point.

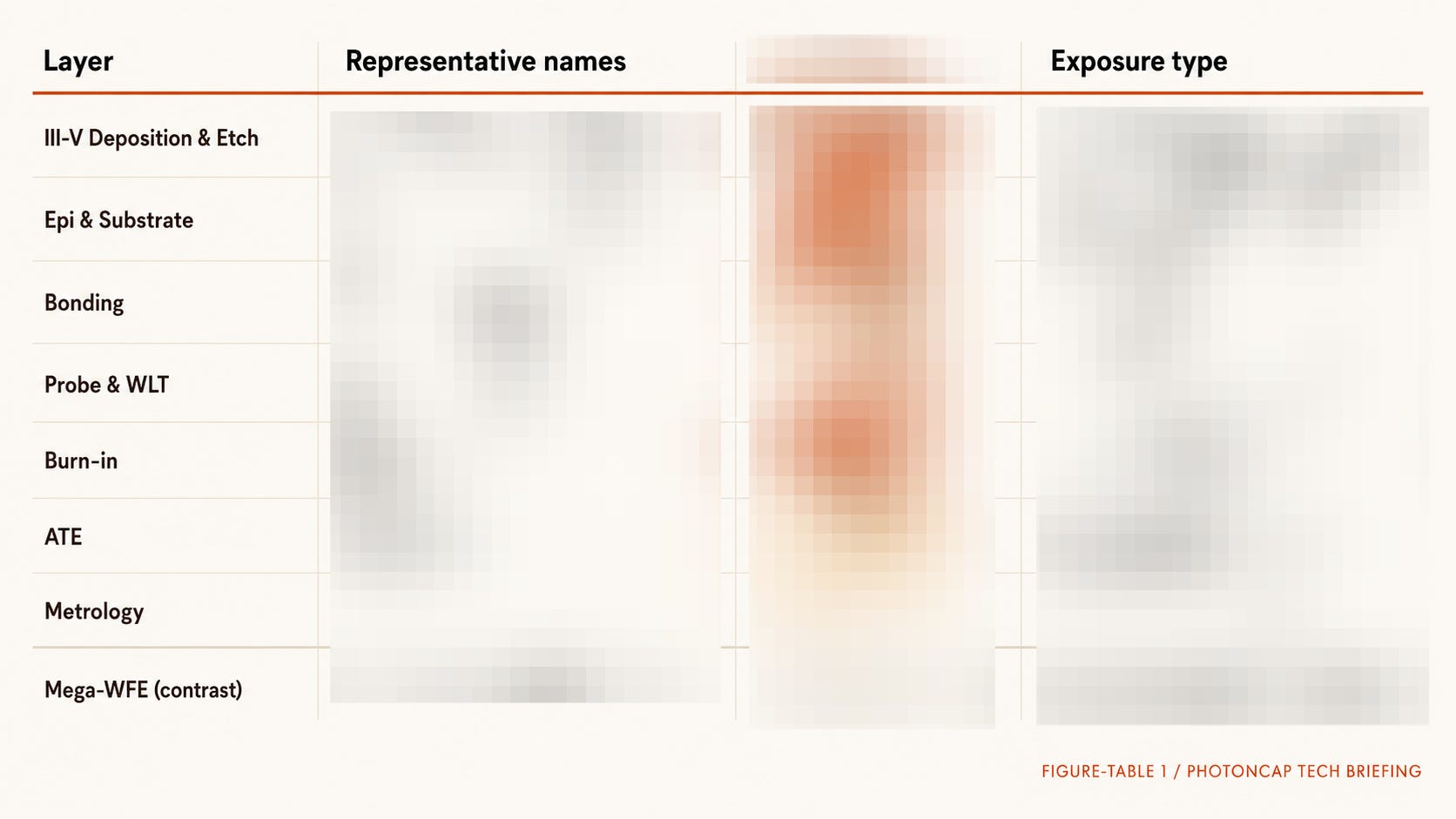

The supplier-agnostic layer in this article is not an abstract AI infrastructure layer. It is the manufacturing, packaging, and test equipment layer that turns compute into a physical product, actual chips and optical engines. To keep it from sounding vague, here is the outline first. The path that turns compute into chips breaks into seven segments. III-V deposition and etch, epi wafers and substrates, bonding, probe and wafer-level test, burn-in, ATE, and metrology. PhotonCap has covered these segments separately over time. Deposition and epi in The 6 Companies Behind Coherent and Lumentum, bonding in Seven Bonding Companies for HBM4 and CPO, and test in The Silicon Photonics and CPO Testing Bottleneck and The Three Pillars of SiPh Wafer Test. This article rebuilds those segments, seen separately until now, under the single frame of compute financialization. The paid section below identifies which companies sit in each segment, and where the beta is most concentrated.

The real difference is what comes next. Do you take this cycle through the broadest WFE names like Applied Materials and LAM Research, or through the specialized equipment and test companies attached more tightly to the compute production bottleneck? Both ride the same cycle, but the revenue impact can differ by an order of magnitude. Where the beta concentrates, the answer may run against intuition.

Three things get worked out below. First, exactly what equipment makes up the layer everyone passes through regardless of the chip and compute winner, and which names stand on which side. Second, why dense packaging grows this layer faster than “count,” the mechanism of that super-linearity. Third, which names survive even in a scenario where compute prices fall.