The Largest IPO in History, One Profitable Layer: Where SpaceX Exposure Really Sits, and the Traps

$SPCX $COHR $LITE $MRVL $RKLB $CACI $NVDA | SpaceX Pre-IPO Beneficiary & Layer Exposure Analysis

SpaceX, the largest IPO in history (ticker SPCX, targeting a June 12 Nasdaq debut at a $1.75T valuation), posted a loss in its most recent fiscal year. The analysis uses the S-1 as the primary source and starts from one observation: SpaceX’s extreme vertical integration makes the pool of “supplier beneficiaries” thinner than people assume. From there it splits the upside into four layers ranked by certainty. Two conclusions. The profit and the proof sit in Layer 1 (LEO connectivity, Connectivity revenue $11.4B, 61% of the company), and the AI revenue that anchors part of the $1.75T valuation comes from idle compute that rivals Anthropic ($1.25B/month) and Google ($920M/month) rent, with the Anthropic contract cancellable on 90 days’ notice and the Google contract carrying GPU delivery conditions plus a 90-day termination right after year-end 2026. So the liquid exposure is not direct supply to SpaceX. It sits in dual-use light source and DSP names ($COHR, $LITE, $MRVL), the OISL bottleneck ($RKLB, $CACI), and the AI infrastructure bottleneck (power, CPO, cooling, $NVDA).

Intro: The $1.75 Trillion Paradox

The largest IPO in history belongs to a company that lost money in its most recent fiscal year. And the “AI revenue” sitting in the middle of that loss is money paid by rivals Anthropic and Google to rent idle compute, on contracts that can be ended on short notice. If you chase “SpaceX beneficiaries” without understanding the structure behind that $1.75 trillion number, you can walk straight into a trap by buying what SpaceX actually builds in-house. The bottleneck is outside the rocket. It separates real exposure from false supplier narratives, layer by layer, working from the S-1.

After 24 years private, SpaceX filed its S-1 on May 20, 2026, and S-1/A amendments on June 1 and June 3 (File No. 333-296070) [1]. The ticker is SPCX, listing on both Nasdaq and Nasdaq Texas. The IPO schedule and terms are per Reuters and CNBC reporting: roadshow June 4, pricing June 11, debut June 12, target price $135 per share, about 555.6 million shares, a $75B raise, and a $1.75T valuation [2]. One caveat: $135 is a target until the effective prospectus and pricing notice land, not a final price. The price box on the S-1 cover was filed blank, and going straight to a single fixed price with no range is unconventional [1][2].

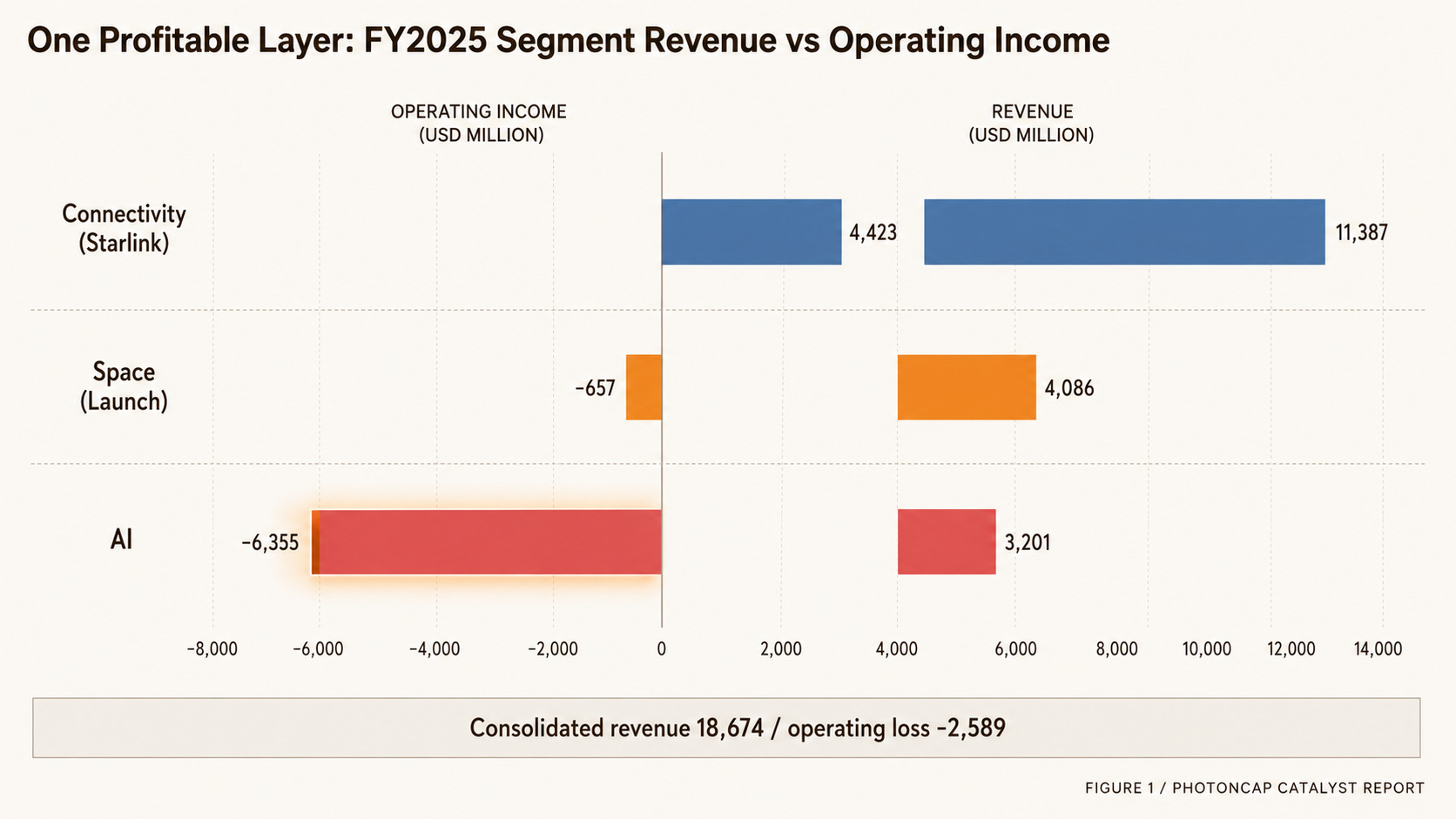

The paradox lives in the numbers. FY2025 consolidated revenue was $18,674M, with an operating loss of $(2,589)M and a net loss of $(4,937)M [1]. 2024 was a profit year at $791M net income, but financials that retroactively fold in the xAI merger (effective February 2, 2026) flip 2025 into a loss [1]. So the largest IPO in history belongs to a company that lost money in its prior fiscal year.

[Figure 1: FY2025 segment revenue and operating income ($M). Starlink is 61.0% of revenue and the only profitable segment, but the AI operating loss drags the consolidated result into the red.]

The premise of this piece is simple. A retail investor cannot easily buy SpaceX equity itself at a reasonable price. Elon Musk controls the vote as a controlled company, and the valuation sits near the top tier of US-listed megacaps (though below the very largest names like Microsoft) [2]. So the question is not “should I buy SpaceX,” but which of the layers SpaceX validated and lifted is tradable as a listed name.

Glossary (for this whole piece)

The recurring acronyms used throughout:

SDA (Space Development Agency): a US Space Force agency. It orders a low-orbit military mesh network (PWSA) by Tranche and adopted optical links (OISL) as the inter-satellite comms standard. The anchor buyer of OISL demand.

ISL / OISL: ISL (Inter-Satellite Link) is the link between satellites. OISL (Optical ISL) is the laser variant, with high bandwidth, low interference, and low probability of intercept versus RF, using a 1550nm InP light source.

OCT (Optical Communication Terminal): the terminal hardware that implements OISL. Only a few firms have been adopted by, or have a supply history with, SDA PWSA.

rad-hard (radiation hardened): semiconductors that survive space radiation (SEU bit flips, TID cumulative dose). They form a separate market.

NTN / D2D (direct-to-cell): NTN (Non-Terrestrial Network) is satellite-based 3GPP communication. D2D connects existing smartphones directly to satellites.

InP / SiPh / CPO / LPO: InP (indium phosphide) is the III-V semiconductor for 1550nm lasers. SiPh (silicon photonics) integrates optical devices onto a silicon chip. CPO co-packages the optical engine next to the switch, and LPO is a linear-drive optical module that drops the DSP.

EDFA / dWDM: EDFA is a 1550nm C-band optical amplifier, and dWDM multiplexes many wavelengths into the same band to grow capacity.

FD-SOI (Fully Depleted SOI): a process favorable for radiation tolerance. ST’s STM32V8 was announced as 18nm FD-SOI and is cited as a candidate commercial chip (COTS) for space.

MFU (model FLOPs utilization): the effective utilization rate of compute resources in an AI cluster.

IRIS²: Europe’s sovereign multi-orbit (LEO/MEO) satellite network program.

The Core Claim: Why Most “SpaceX Supplier Beneficiaries” Are Closer to Traps

The word running through the entire S-1 is extreme vertical integration. SpaceX designs and builds its own Merlin and Raptor engines, satellites, user terminals, inter-satellite lasers, even custom silicon for Starlink [1]. It has gone further and started to sell its own space lasers to outside parties, supplying mini laser terminals to Muon Space and integrating into Vast’s Haven-1 [3]. The surge in silicon photonics, dWDM, and EIC roles in its job postings reads as a signal that SpaceX is building optical comms in-house, something we analyzed earlier (SpaceX-xAI: the silicon photonics underneath the valuation). In optical comms, then, SpaceX is closer to a competitor and a supplier than a customer of outside OCT vendors.

SpaceX-xAI: The $1.25T Valuation Built on Silicon Photonics

0. Prologue: The Real Meaning of “Inaccurate”

That is the first filter for beneficiary analysis. A company that builds its own rockets, satellites, lasers, and terminals has a much thinner pool of outside suppliers worth calling “beneficiaries” than people assume.

But the S-1 also names the points where the vertical integration stops. The real exposure is right there.

GPU: “We do not have long-term or material contracts with our direct chip suppliers and procure all GPUs on a purchase-order basis. Our direct chip suppliers depend on a small number of advanced fabs” [1].

Power: “We depend significantly on natural gas and gas turbine technology to operate our data centers” [1].

Optical interconnect, cooling, power equipment: gigawatt-scale clusters built with outside equipment.

To summarize: SpaceX builds its own rockets, satellites, lasers, terminals, and orbital operations, but it buys GPUs, power generation, advanced fab capacity, and data center infrastructure. So the liquid beneficiaries cluster in two places.

The LEO / optical comms theme: SpaceX validated the technology and grew the market, but the flow is not SpaceX revenue. It is the rival LEO camp and SDA’s proliferated architecture that ride it.

The AI infrastructure bottleneck: power, heat, optical interconnect, GPU. SpaceX and xAI are just one buyer in this huge AI capex wave, and the upside overlaps with the general AI infrastructure trade.

The center of gravity is worth stating up front. On certainty and profitability, the part with verified fundamentals concentrates in Layer 1 (LEO), and Layer 4 (orbital AI) has almost no verifiable financial basis at this stage. This piece weights its analysis in that order. Below, each layer is cut in order of certainty.

Layer 1: LEO Connectivity (Now, Profitable)

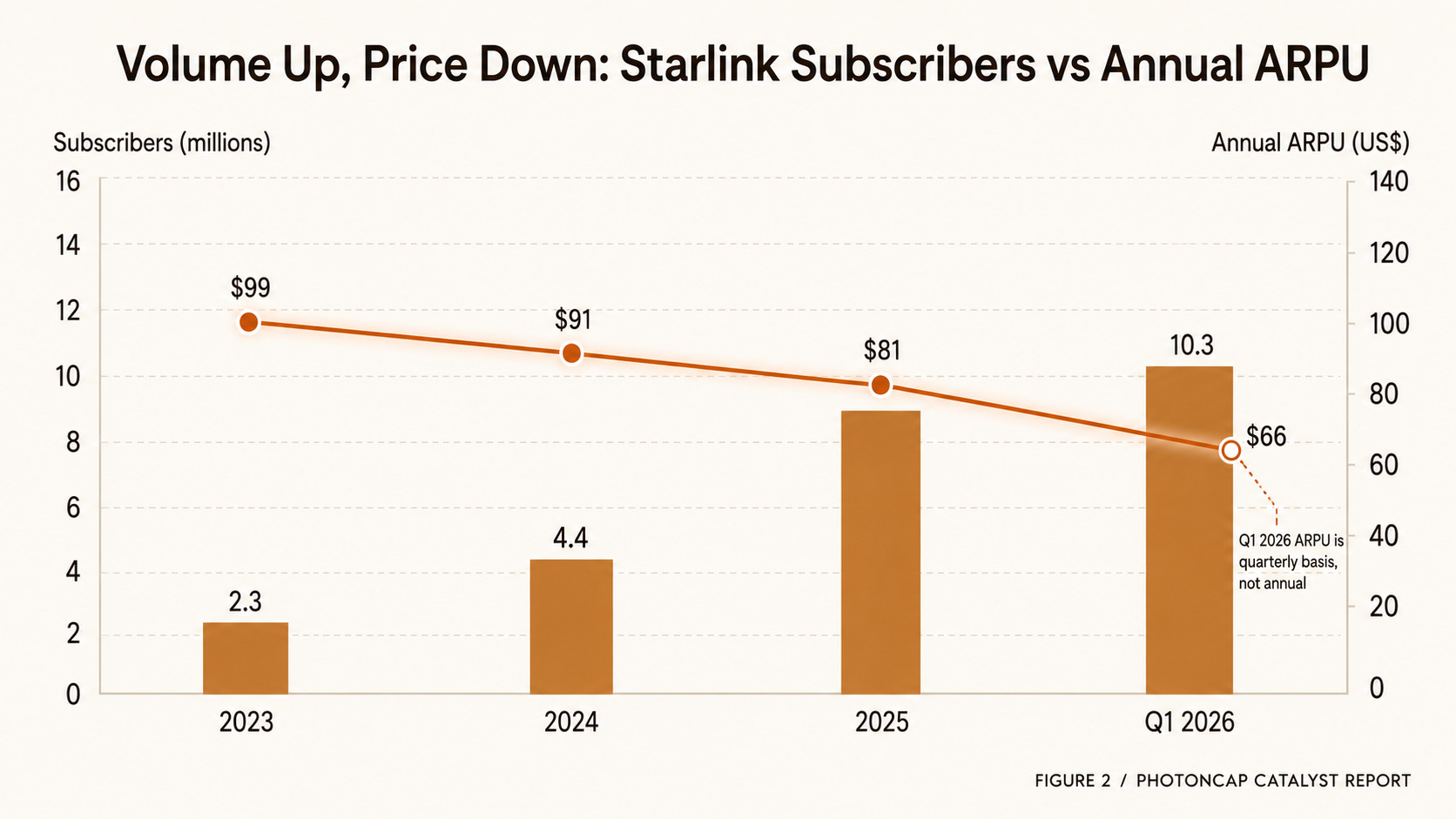

Starlink is SpaceX’s only GAAP-profitable engine. FY2025 Connectivity segment revenue was $11,387M (+49.8% YoY), with operating income of $4,423M (+120.4%) and Segment Adjusted EBITDA of $7,168M (+86.2%) [1]. That is exactly 61.0% of company revenue. Subscribers more than doubled on a quarterly basis, from 5.0M in Q1 2025 to 10.3M in Q1 2026, with roughly 9,600 satellites across 164 countries, about 75% of all maneuverable satellites worldwide [1].

ARPU has a trap, so the notation has to be split. Annual ARPU fell 18.2%, from $99 in 2023 to $91 in 2024 to $81 in 2025, while quarterly ARPU dropped 23.3%, from $86 in Q1 2025 to $66 in Q1 2026 [1]. That is the result of trading subscriber volume for ARPU. There is reporting of a May 2026 price increase aimed at defending unit pricing [2]. The quality of the profit is good, but the pricing pressure is a real risk.

You cannot mix annual $81 and quarterly $66 in the same sentence. Anyone who follows the source will catch it.

[Figure 2: Starlink subscribers and ARPU trend. Subscribers grew from 2.3M at the end of 2023 to 10.3M in Q1 2026, while annual ARPU fell from $99 to $81 over the same span.]

Layer 1 beneficiaries: why they belong under “theme”

Because of the vertical integration filter, the names below are classified as LEO / optical comms theme exposure, not “direct supply to SpaceX.” SpaceX validated OISL and grew the market but builds it in-house, so the upside flows toward SDA, the rival LEO camp (Amazon Leo and others), and IRIS².

Optical comms / OISL value chain: the OISL terminal bottleneck concentrates in a small set of OCT vendors that have actually been adopted by, or have a supply history with, SDA PWSA. In April 2026, Rocket Lab ($RKLB) acquired Mynaric for $155.3M, thinning the independent OCT pool, and what remains centers on Tesat-Spacecom (an Airbus subsidiary), Skyloom (private), and CACI ($CACI) [4]. The structure rides SDA and rival-camp demand, not SpaceX supply. We cover the 26 names organized by GVM Score and a 4-tier cascade in the 26-name LEO satellite cycle investment map.

[Investment Map] 26 Companies in the LEO Satellite Cycle: From Deployment to Service

![[Investment Map] 26 Companies in the LEO Satellite Cycle: From Deployment to Service](https://substackcdn.com/image/fetch/$s_!lPvt!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc1928833-682c-4872-9ef1-c3bf54eb9fca_1704x893.png)

LEO mega-constellations are moving from a “deployment phase” to a “service phase.” Amazon Leo (formerly Project Kuiper) began its enterprise preview in November 2025 and confirmed a mid-2026 commercial launch [1][7]. AST SpaceMobile received FCC commercial authorization for its 248-satellite direct-to-device constellation [2]. Starlink operates an active constellation of roughly 10,000 satellites by tracker count [3]. This piece evaluates 26 listed names spread across nine or more countries (North America, Europe, Korea, Japan) using a satellite-comm-cycle-specific 5-axis GVM Score, maps them onto a 4-tier cascade, and distributes them across a Catalyst Calendar through the end of 2027. Identification, mapping, and scenario analysis for the 26 names are covered in the paid section.

Light source / DSP (dual-use): Coherent ($COHR), Lumentum ($LITE), and Marvell ($MRVL) sit across the same 1550nm / InP / high-speed DSP technical axis, giving them thematic exposure to both ground AI optics and space OISL. They are the intersection exposed to Layer 1 and Layer 3 at once, which makes them the key crossover of this cycle. For the detailed value chain, see the SpaceX-xAI silicon photonics value chain.

SpaceX-xAI: The $1.25T Valuation Built on Silicon Photonics

0. Prologue: The Real Meaning of “Inaccurate”

Semiconductor / control (Samsung, STM, and others): per ST’s official release, the STM32V8 is an 18nm FD-SOI MCU selected by SpaceX and used in the Starlink mini laser system [5]. ST describes the product as based on its Crolles 300mm fab and a Samsung Foundry partnership [5]. That said, the fab allocation for individual Starlink volumes is not separately confirmed, so any Samsung-side benefit is treated only as a supply-chain theme.

The key conclusion here is one line. A SpaceX beneficiary is not “a company that supplies SpaceX.” It is a company standing at a bottleneck SpaceX cannot build itself. That bottleneck is power, GPU, optical interconnect, and the OISL of LEO camps other than SpaceX.

That is the end of the free section. The paid section covers these. The real structure of the Anthropic ($1.25B/month) and Google ($920M/month) compute contracts that hold up the AI revenue, and why this revenue is structurally less durable than the headline number suggests [1][6]. The layer-by-layer sorting and the dual-use names that span two layers. The date-stamped catalyst calendar. And the boundary between the names this analysis treats as “theme exposure” and the ones it classifies as “blocked by vertical integration.” It is an angle a public earnings-call recap does not give you.