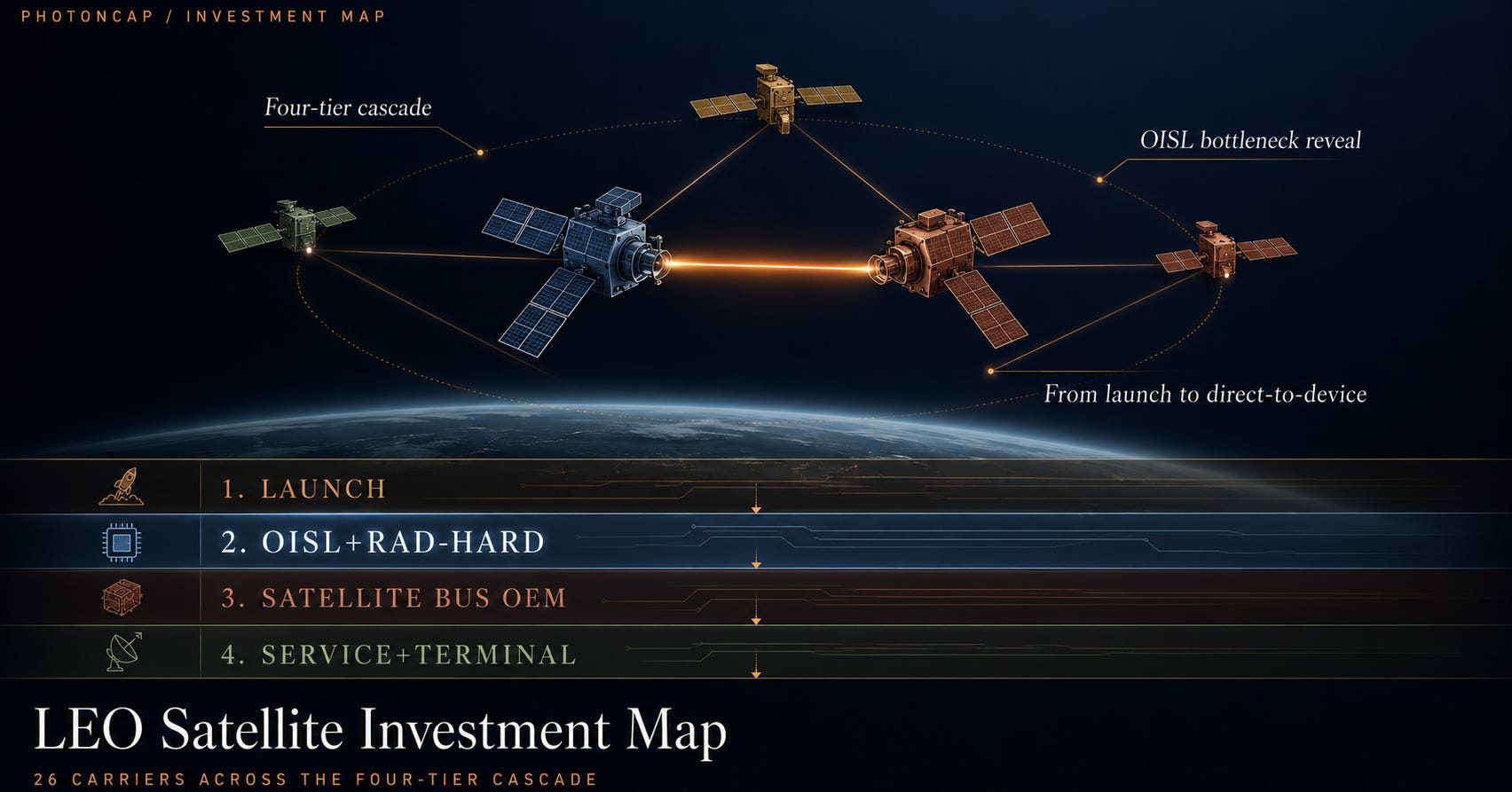

[Investment Map] 26 Companies in the LEO Satellite Cycle: From Deployment to Service

The companies that connect satellites are scarcer than the companies that launch them. $RKLB $CACI $MCHP $ASTS $MDA.TO + 21 more

LEO mega-constellations are moving from a “deployment phase” to a “service phase.” Amazon Leo (formerly Project Kuiper) began its enterprise preview in November 2025 and confirmed a mid-2026 commercial launch [1][7]. AST SpaceMobile received FCC commercial authorization for its 248-satellite direct-to-device constellation [2]. Starlink operates an active constellation of roughly 10,000 satellites by tracker count [3]. This piece evaluates 26 listed names spread across nine or more countries (North America, Europe, Korea, Japan) using a satellite-comm-cycle-specific 5-axis GVM Score, maps them onto a 4-tier cascade, and distributes them across a Catalyst Calendar through the end of 2027. Identification, mapping, and scenario analysis for the 26 names are covered in the paid section.

This is the second investment map in the PhotonCap series, following Investment Map / 15 Companies in the Glass Substrate Supply Chain. Where the first piece covered the supply chain underneath the AI datacenter core, this one looks at the layer where that infrastructure extends into space. I have been tracking the intersection of SpaceX and optics (OISL, SiPh) for a long time, and as a 2-year RKLB investor, the space cycle remains a personal interest. Recent threads have started to converge into a single thesis: Elon Musk’s mentions of space datacenters, SpaceX’s silicon photonics adoption, and the photonic semiconductor supply chain are now lining up. This piece is an extension of that work, written to push the analysis further and stay invested.

Contents

Intro: A Production Cycle in Orbit

Technology Background: OISL, Rad-Hard, and InP/SiPh

Why the Cycle Is Starting Now

Other Applications on the Same Supply Chain

GVM Score, Cascade Sequencing, Catalyst Calendar

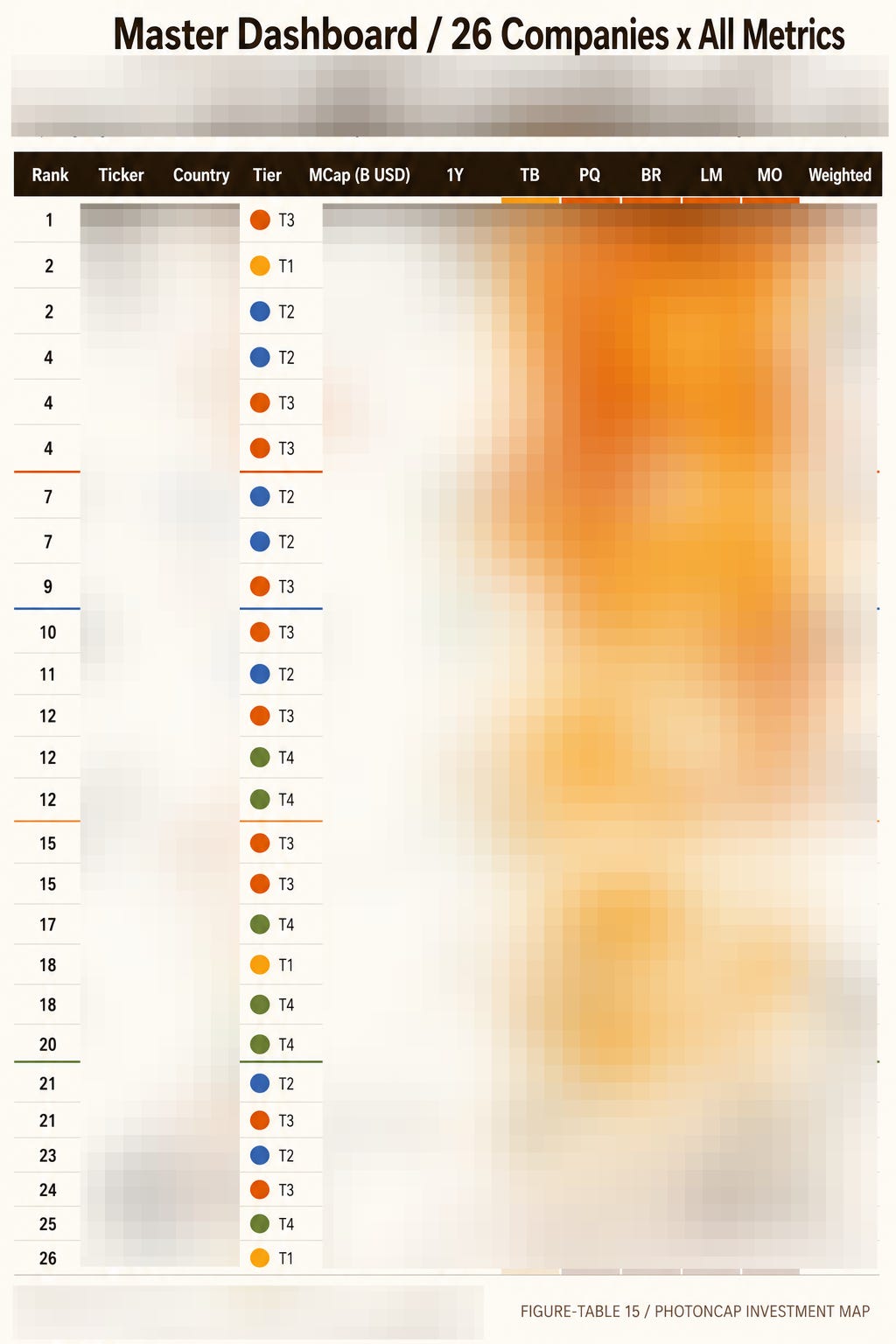

26 Carriers: Identification and Market Cap Comparison

GVM Score: Satellite-Comm-Specific 5-Axis Evaluation

Cascade Sequencing: Time-Lag Between Tiers

Catalyst Calendar: Trigger Events Through End of 2027

Company Cards: Top 5 Deep + 21 Compact

Asymmetric Outcome: Scenarios and Monitoring

Where the Framework Breaks: Hypothesis-Level Validation Signals

Watchlist: Private + Adjacent

Conclusion: The Mismatch in the Orbit Timeline

References & Sources

1. Intro: A Production Cycle in Orbit

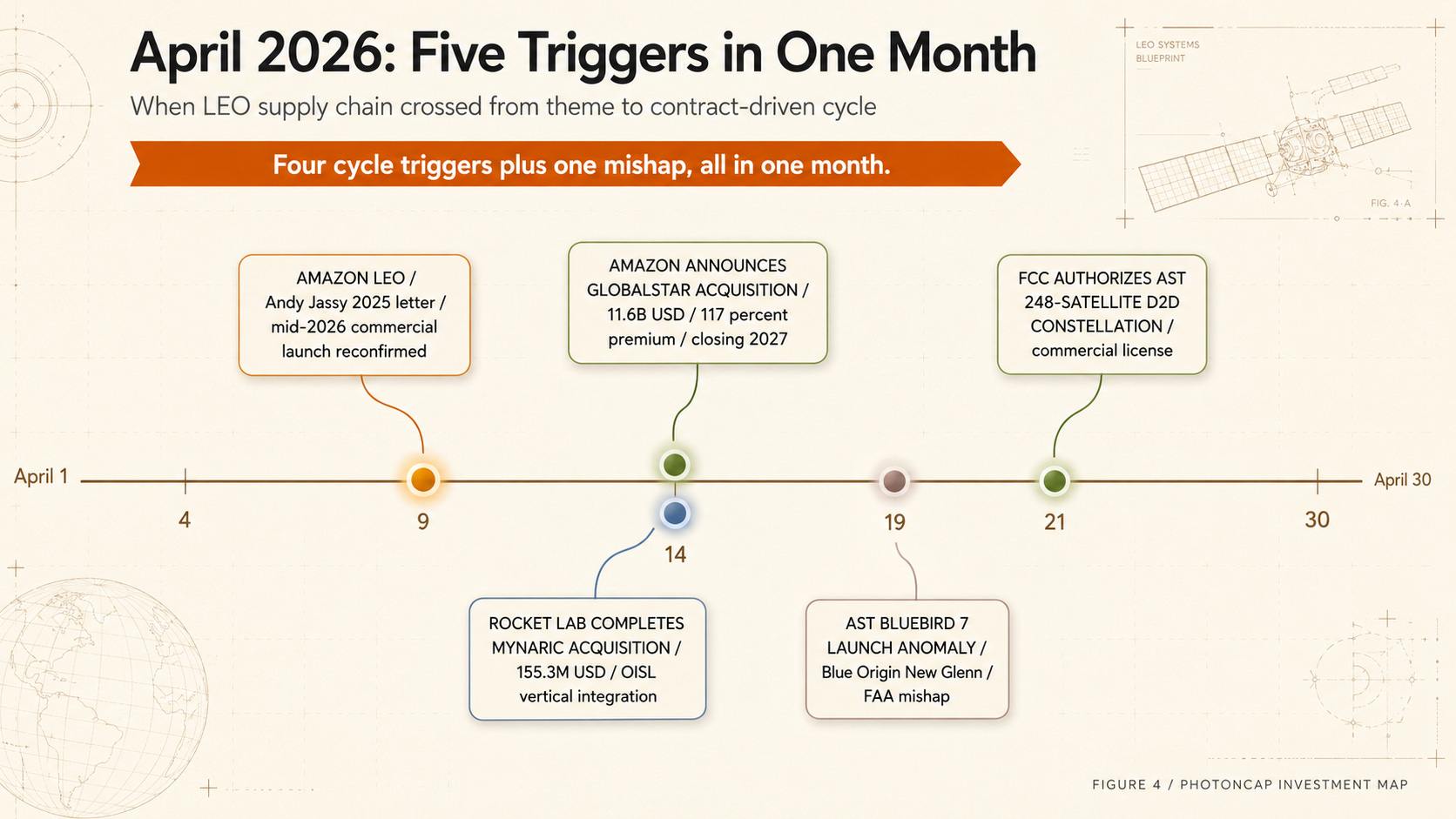

On April 14, 2026, two acquisitions were announced on the same day. Rocket Lab completed its acquisition of OISL terminal company Mynaric for $155.3M [4]. Amazon announced its $11.6B acquisition of satellite-comm operator Globalstar [17]. One internalized a bottleneck. The other locked in spectrum and infrastructure. Same day, same industry, two different layers sealed in.

That same month, names sitting on the LEO satellite supply chain moved like this. +314% off the 52-week low. +280%. +185%. +112%. The names behind those moves are unpacked in this piece.

Since 2020, LEO mega-constellations have mostly been in the “we’re launching satellites” stage. Starlink put dozens of satellites up every month, the market got as far as “oh, satellite internet works,” and that was about it. For a supply chain investor, the layer that mattered was elsewhere. Not the launch vehicle. Not the satellite bus itself. The optical inter-satellite link (OISL) terminal that connects satellites to satellites, and the rad-hard semiconductors that survive the radiation environment. That is the bottleneck of this cycle.

In April 2026, four things landed in the same month. Amazon Leo reconfirmed its mid-2026 commercial launch [7]. Rocket Lab completed its $155.3M acquisition of OISL terminal specialist Mynaric [4]. Amazon announced its $11.6B Globalstar acquisition [17]. The Space Development Agency (SDA) accelerated Tranche 2/3 awards following its Tranche 1 first launch in September 2025 [5]. The transition from “R&D awards” to “repeat production awards” is happening right now.

Core thesis: As LEO mega-constellation transitions from “deployment phase” to “service / production phase” in 2026, the cycle alpha is unlocked not in launch vehicles but in the Tier 2 bottleneck made up of OISL terminals and rad-hard semiconductors. The 5 axes of the GVM Score are Technology Bottleneck, Program Qualification, Backlog-to-Revenue, Launch Manifest Depth, and Multi-Orbit Readiness.

The scope of this piece: 26 listed names exposed to the production cycle, a private watchlist, and supply chain positioning. The 26 names span the US, Korea, France, Germany, the UK, Japan, Italy, Luxembourg, and Canada (nine or more countries), with market caps ranging from roughly $220M to $136B. About 620x apart in size, all exposed to the same cycle.

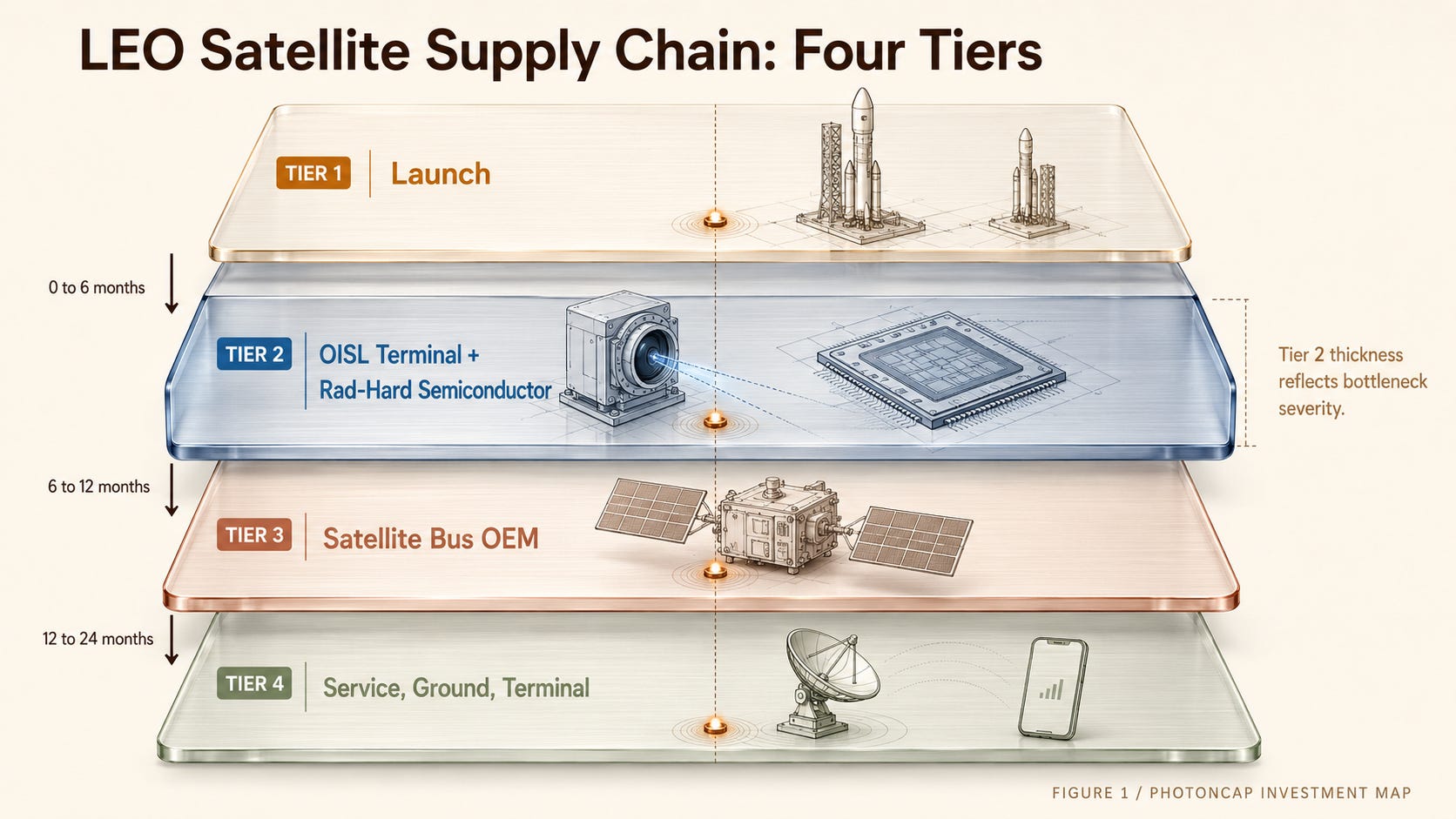

[Figure 1: LEO satellite supply chain / 4-tier schematic, no company names]

2. Technology Background: OISL, Rad-Hard, and InP/SiPh

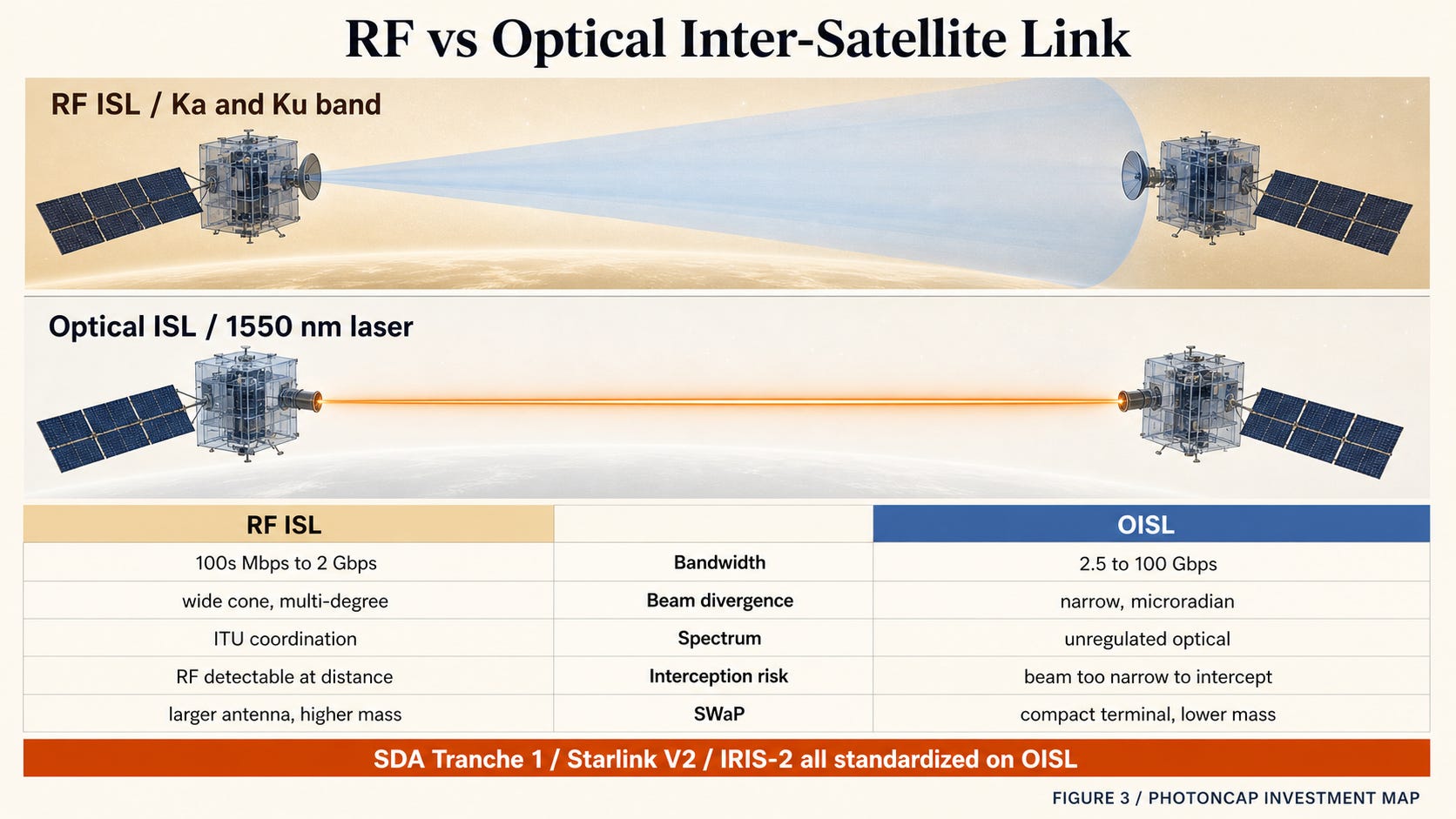

Why OISL, Not RF

There are two ways for satellites to exchange data with each other. Radio (RF inter-satellite link) and laser (optical inter-satellite link). Early constellations used RF. Either via ground station hops, or via Ka/Ku-band RF cross-links between satellites.

The bandwidth gap is the issue. RF ISL caps out at hundreds of Mbps, maybe 1 to 2 Gbps at best. OISL today runs at 2.5 to 100 Gbps, and the SDA spec is rising from 2.5 Gbps class to next-generation 10 Gbps [5]. Starlink V2 Mini onward carries OISL terminals. SDA has locked OISL as the standard from Tranche 1.

The difference is not just carrier frequency. It also comes from aperture efficiency, beam divergence, link budget, and pointing stability. RF ISL is constrained by spectrum allocation and antenna aperture, while OISL uses narrow beams and a higher optical carrier to deliver much higher point-to-point throughput. On top of that, no spectrum interference, hard to intercept (extremely narrow beam), and better SWaP (size, weight, power).

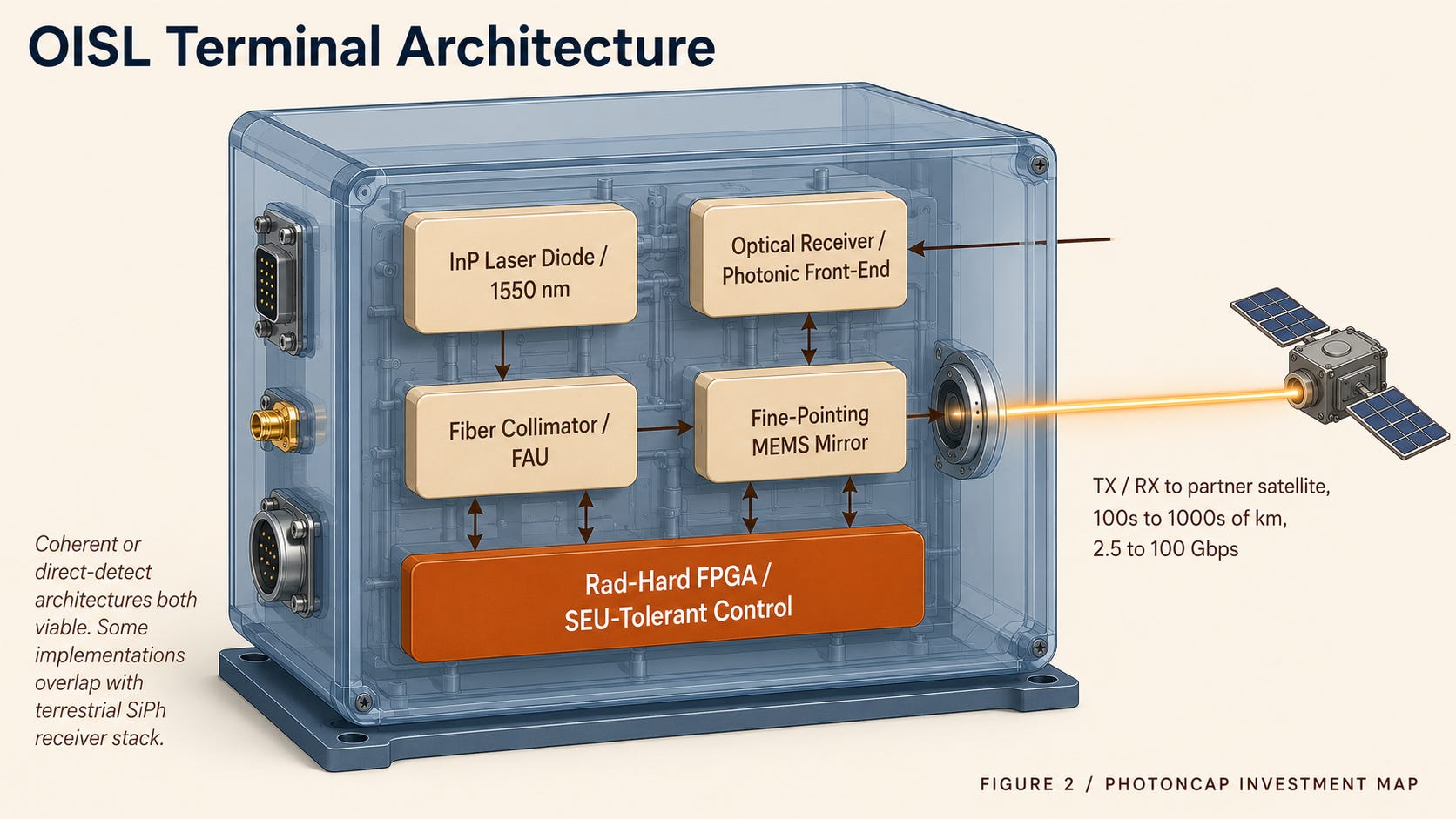

What Goes Inside an OISL Terminal

Open up an OISL terminal and there are five core parts.

InP laser diode: 1550 nm class light source. Same InP (indium phosphide) base used in terrestrial fiber-comm transceivers

Optical receiver / photonic front-end: converts 1550 nm optical signal to electrical. Coherent or direct-detect architectures both possible. Some implementations overlap with SiPh receiver stacks

Fiber collimator / FAU (Fiber Array Unit): optical alignment

Fine-pointing MEMS mirror or FSM: beam pointing between satellites. Tracks at micro-radian precision over hundreds to thousands of kilometers

Rad-hard FPGA/ASIC: the processor that controls all of the above. Operates without SEU (single-event upset) in the space radiation environment

Items 1 and 2 are the ones that matter. The technology stack of InP laser, 1550 nm photonic receiver, fiber coupling, and precision pointing all goes through space qualification and ends up inside the OISL terminal. Coherent, Lumentum, and II-VI (now Coherent) legacy lines build both terrestrial datacenter transceivers and space laser terminals. Different applications on the same supply chain. PhotonCap has been tracking this stack’s SpaceX exposure early. SpaceX’s adoption of laser ISLs was first identified in the community in SpaceX, the Secret Behind the $800 Billion Valuation: Space Connected by Lasers, and Finding Hidden Beneficiaries, and the company’s silicon photonics adoption was analyzed within hours of the relevant job descriptions appearing in SpaceX-xAI: The $1.25T Valuation Built on Silicon Photonics.

SpaceX, the Secret Behind the $800 Billion Valuation: Space Connected by Lasers, and Finding Hidden Beneficiaries

The Real Reason the Market is Obsessed with SpaceX (Despite Musk’s Denial)

SpaceX-xAI: The $1.25T Valuation Built on Silicon Photonics

0. Prologue: The Real Meaning of “Inaccurate”

Rad-Hard Semiconductors: Why a Separate Layer

Terrestrial semiconductors can be used in some LEO missions with screening, shielding, redundancy, and fault-tolerant design, but mission-critical control electronics often require radiation-tolerant or radiation-hardened parts. High-energy particles (protons, heavy ions) hit transistors directly and cause bit flips (SEU), and accumulated radiation dose (TID) drifts threshold voltage until the chip dies. So rad-hard FPGA/ASIC forms its own market. Microchip Technology’s RT PolarFire and BAE Systems’ RH12 (built on GlobalFoundries 12 nm FinFET) are examples in this market [6].

Characteristics: low-volume production, high margins, long qualification cycles (5 to 7 years), strong customer lock-in. Once a chip gets in, it stays in for the life of the program.

[Figure 2: OISL terminal block diagram / InP laser + SiPh receiver + MEMS mirror + rad-hard FPGA]

[Figure 3: RF ISL vs OISL comparison / bandwidth, SWaP, security, interference]

3. Why the Cycle Is Starting Now

LEO satellite constellation has been a topic for over ten years. Iridium has been around since the 1990s, OneWeb went bankrupt in 2020 and came back, Starlink started launching in 2019. So why is 2026 a turning point from a supply chain investing perspective. Four triggers landed in the same month. Just April.

First, Amazon Leo’s commercial launch reconfirmation (April 9). After rebranding from Project Kuiper to Amazon Leo and starting an enterprise preview in November 2025, Amazon CEO Andy Jassy’s April 9, 2026 shareholder letter reconfirmed the mid-2026 commercial launch and revenue commitments from enterprise, government, and telco customers [7]. Amazon disclosed that its Kirkland satellite manufacturing facility was designed for peak capacity of 5 satellites per day production (annual capacity of roughly 1,000 satellites, author estimate) [7]. Launches use ULA Atlas V, Arianespace Ariane 64, Blue Origin New Glenn, and even SpaceX Falcon 9, and after the LE-02 launch in late April 2026, roughly 302 production satellites are in orbit [8]. Amazon has filed for a 2-year extension of its FCC first-deadline (1,618 satellites by July 30, 2026, half of the constellation) to 2028.

What this means for the supply chain: once Amazon goes into a monthly launch cadence, repeat demand emerges across satellite component classes such as OISL, rad-hard electronics, phased-array antennas, solar arrays, and propulsion. The shift from one-off R&D purchases to repeat production demand is the starting point of the supply chain investing thesis.

Second, Rocket Lab’s Mynaric acquisition completed (April 14). That same week, Rocket Lab completed its acquisition of Munich-based OISL terminal specialist Mynaric AG [4]. $155.3M in aggregate consideration (cash plus 2,277,002 RKLB common shares). Mynaric’s CONDOR Mk3 terminals were already going into Rocket Lab’s SDA Tranche 2 Transport Layer-Beta program as the OISL component, and this acquisition internalized that capability. Rocket Lab’s SDA position now consists of Tranche 2 Transport Layer-Beta 18 satellites ($515M, January 2024) plus Tranche 3 Tracking Layer 18 satellites ($816M, December 2025), totaling $1.3B+ in SDA prime contracts [4].

This acquisition reshaped the OISL market structure. There were four SDA-qualified OISL terminal suppliers: Mynaric, Tesat-Spacecom US, Skyloom, and CACI [9]. With Mynaric absorbed into Rocket Lab, the count of independent OISL suppliers dropped by one, and Rocket Lab became the only listed company that vertically integrates launch, spacecraft, and OISL.

Third, Amazon’s Globalstar acquisition announcement (April 14). That same day, Amazon announced its $11.6B acquisition of satellite-comm operator Globalstar at $90 per share (or 0.3210 Amazon shares) [17]. A 117% premium to the late October 2025 close. The deal absorbs Globalstar’s L-band and S-band spectrum licenses, 24 operational LEO satellites, and 24 global ground gateways in one move. The company that was the backbone of Apple iPhone Emergency SOS (with 85% of Globalstar capacity reserved for Apple) now becomes the direct-to-device infrastructure for Amazon Leo. Closing expected in 2027. Bloomberg reported that Amazon stated it “will launch a direct-to-device service” in 2028 [19].

The implication: Amazon is signaling entry into the D2D (direct-to-device) market alongside LEO broadband. With spectrum, satellites, and ground stations secured at once, additional demand emerges for D2D supply chain components (antennas, beam-forming ASICs, rad-hard semiconductors). The market read this deal as a commitment to both satellite broadband and D2D cellular.

Fourth, SDA Tranche 1 first launch + Tranche 2/3 acceleration. The Space Development Agency, under US Space Force, is building a LEO military mesh network (Proliferated Warfighter Space Architecture). Tranche 1 first 21 satellites launched on September 10, 2025 (built by York Space Systems, on SpaceX Falcon 9) [5]. Tranche 1 total (150+ satellites) runs as a 10-month launch campaign, and Tranche 2 Transport Layer Beta first launch is scheduled for September 2026 (ILC). Tranche 3 Tracking Layer was awarded December 19, 2025: $3.5B / 72 satellites across four primes [5]. However, Tranche 3 Transport Layer is paused under Pentagon review. SDA is the anchor buyer of OISL demand.

Additional: AST SpaceMobile FCC authorization plus launch incident (same week). On April 21, 2026, the FCC issued AST SpaceMobile authorization for SCS (Supplemental Coverage from Space) and direct-to-device commercial service across its 248-satellite constellation [2]. The deadlines: 124 satellites by August 2, 2030; full 248 by August 2, 2033. But two days before the authorization, on April 19, BlueBird 7 was placed in a lower-than-planned orbit on the third Blue Origin New Glenn flight after a second-stage burn anomaly, and was classified as expected to de-orbit [10]. AST announced an expected $30M insurance claim, and the FAA placed New Glenn under mishap classification (grounded). Both the bull case and the risk of the D2D cycle landed in the same week.

April was the month LEO supply chain shifted from a simple theme to a contract-driven cycle. Amazon Leo commercial launch reconfirmation, the Globalstar acquisition, the Rocket Lab-Mynaric acquisition, the imminent SDA Tranche 2 ILC, and the ASTS FCC authorization plus launch incident all landed simultaneously.

[Figure 4: April 2026 Cycle Trigger Map / five events, four triggers plus one mishap]

4. Other Applications on the Same Supply Chain

If you look at the satellite-comm cycle as just LEO broadband, the picture shrinks. There are at least four applications sitting on the same OISL, rad-hard, and launch supply chain.

1. LEO broadband (Starlink, Amazon Leo), now. The largest volume driver. Starlink active constellation roughly 10,000 satellites, Amazon Leo 3,236 satellites planned. These two constellations create the production demand for OISL, antennas, solar panels, and propulsion.

2. Direct-to-Device (AST SpaceMobile, Amazon/Globalstar, Starlink Direct-to-Cell), 2026 and later. Satellite broadband through existing smartphones. With Amazon’s $11.6B Globalstar acquisition, a hyperscaler entered the D2D market directly [17]. Globalstar’s L+S-band spectrum plus Amazon Leo’s constellation equals D2D infrastructure. AST SpaceMobile is going for broadband-class D2D independently. SpaceX secured its own D2D spectrum through a $17B EchoStar AWS-4 + H-block acquisition in September 2025 [15]. Demand for antennas and beam-forming ASICs.

3. Defense mesh networks (SDA, IRIS²), 2026 to 2030. The US SDA’s Proliferated Warfighter Space Architecture plus Europe’s IRIS² (Infrastructure for Resilience, Interconnectivity and Security by Satellite). SDA Tranche 2 ILC is September 2026. IRIS² signed a €10.6B 12-year concession contract with the SpaceRISE consortium (led by SES, Eutelsat, Hispasat) on December 16, 2024, covering a 290-satellite multi-orbit constellation, first launch in 2029, services starting 2030 [20]. For defense use, OISL is required (anti-intercept and low-latency). The largest customer for rad-hard semiconductors.

4. Cislunar / deep space, 2028 and beyond. NASA Artemis, Lunar Gateway, deep space relay. Volumes are small but unit pricing is extremely high, and flight heritage stacks up here.

The baton passes from “LEO broadband to D2D cellular to defense mesh to cislunar / deep space.” The first application creates volume; the next application expands TAM.

The key point: the same exact product is not repeated, but the technology stack of InP laser, coherent receiver, fine-pointing optics, and rad-hard control electronics gets reused across LEO broadband, SDA mesh, IRIS², and cislunar relay as the baton passes. Companies with high Technology Bottleneck scores have a high probability of carrying their qualification and flight heritage forward to the next program even when the first application changes.

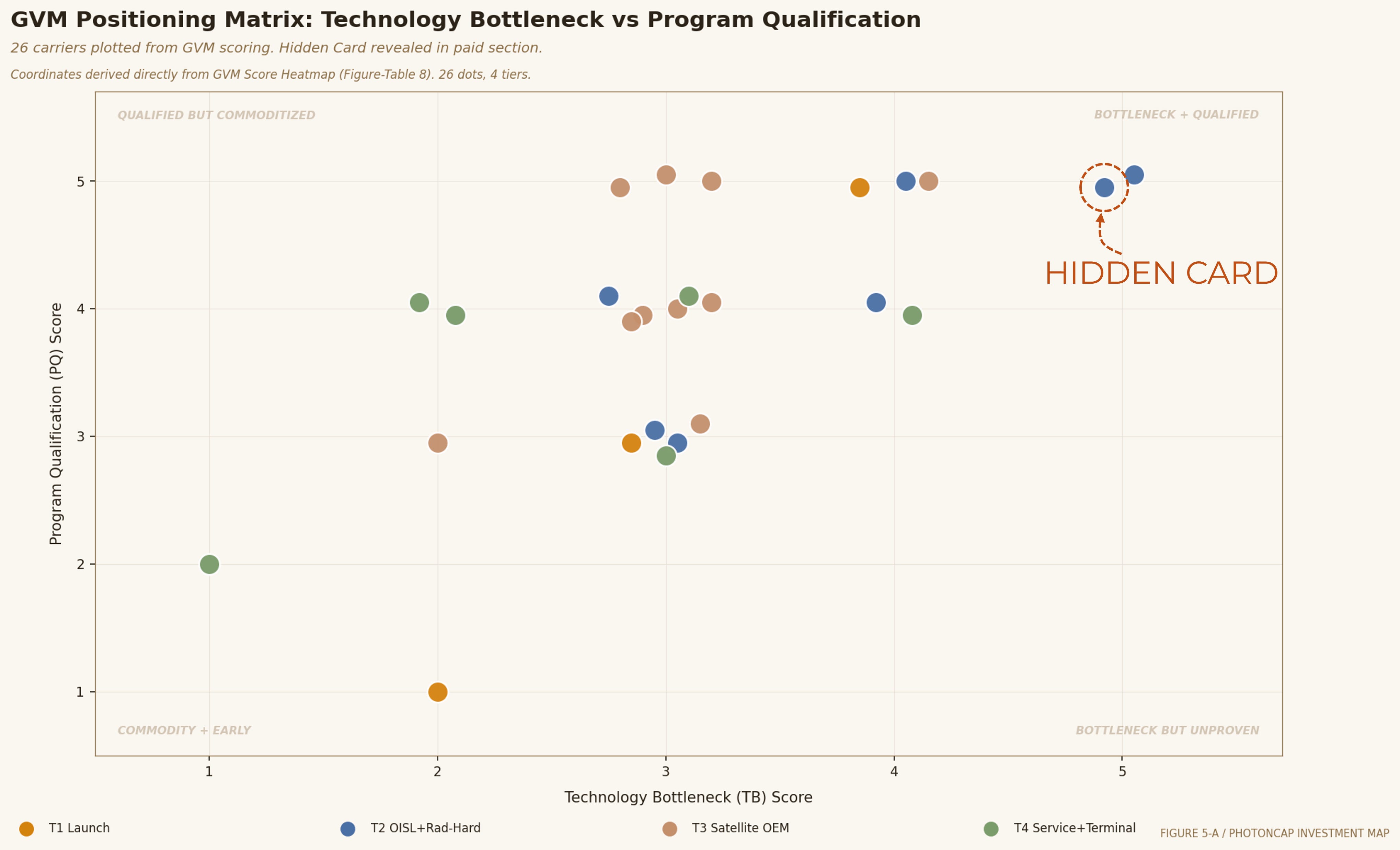

5. GVM Score, Cascade Sequencing, Catalyst Calendar

The market saw the LEO satellite cycle as a “theme.” ASTS rallied, RKLB rallied, the “space-related stock” label was traded back and forth. But when the cycle moves from “deployment phase” to “production phase,” theme pricing breaks. Spread widens between companies with the same LEO exposure but different analytical quality.

The paid section of this piece applies three frameworks simultaneously to the 26 names.

Framework 1: GVM Score (Global Value Map, 5-axis). Each company is scored 1 to 5 across Technology Bottleneck, Program Qualification, Backlog-to-Revenue, Launch Manifest Depth, and Multi-Orbit Readiness. Total range 5 to 25. The exact difference between a 1 and a 5 on each axis, and which axes carry more weight by cycle phase (phase weighting), are unpacked in the paid section.

Framework 2: Cascade Sequencing (4-tier with time-lag). Tier 1 (Launch) to Tier 2 (OISL + Rad-Hard) to Tier 3 (Satellite OEM) to Tier 4 (Service / Terminal). One feature: this cascade is closer to parallel than sequential. Hyperscalers (Amazon) are placing orders into Tier 2 and Tier 3 simultaneously, and SDA is overlapping Tranche awards. Where this parallel structure creates alpha across tiers is the core analysis of the paid section.

Framework 3: Catalyst Calendar (through end of 2027). Catalyst events landing roughly 19 months from 2026 Q2 to 2027 Q4 are plotted on a timeline. Amazon Leo commercial service, Neutron maiden flight, SDA Tranche 2 ILC, IRIS² prime contractor selection, ASTS commercial service ramp, Amazon-Globalstar deal closing, SDA T2 Gamma launches. Which company’s catalyst lands when, assembled.

This is as far as public materials alone get you.

The real difference starts here. What score each of the 26 names received on each of the 5 axes, and how the ranking flips when phase weighting is applied. Where the valuation gap sits across the four tiers. And one structural inefficiency the market has not priced in yet.

If you split the 26 into four groups:

“Vertically integrated launch”: launch + spacecraft + OISL inside a single company

“OISL bottleneck holder”: a handful of companies supplying flight-proven OISL terminals globally

“Satellite production prime”: large defense / space OEMs producing satellite buses for SDA / commercial constellations at scale

“D2D service bet”: early revenue or pre-commercial-scale. Optionality on service ramp

The market gave a premium to “vertically integrated launch” and “D2D service bet.” RKLB sits at P/S of roughly 93x (TTM revenue $602M, market cap $56B). ASTS sits at hundreds of x P/S on FY25 revenue. But within the “OISL bottleneck holder” group, there is a name that is GVM top tier yet still priced at defense-IT multiples by the market. Its 1-year return diverges sharply from other names in the same GVM cluster. The market has not yet separated OISL scarcity as a distinct valuation factor.

And there is one more Hidden Card. Among the 26 names, there is one with a high TB (Technology Bottleneck) score but with space revenue under 5% of total, so the market reads it purely as a “terrestrial semiconductor cycle recovery” play. That name’s space revenue ramps when constellation production volume kicks in around 2027 to 2028. The time gap between the terrestrial semiconductor cycle and the space semiconductor cycle is creating its mispricing.

What these names are, why the TB x PQ combination is the cycle alpha, and how phase weighting flips the ranking, are unpacked in the paid section.

[Figure 5-A: Positioning Matrix / Hook Version (dots only, no names, CACI position with dashed amber Hidden Card ring)]