One Layer Below SemiAnalysis’s Meta Map: Scale-Across Is Coherent, Not CPO

$MRVL $COHR $CIEN $LITE $META | Scale-Across Coherent DCI Demand Validation

Over the past few months, PhotonCap has covered the supply side of the optical layer that links datacenters to one another (scale-across) three separate times. This week’s SemiAnalysis breakdown of Meta’s infrastructure is the first concrete blueprint showing that demand for that layer is being deployed at gigawatt scale.[1] The point is simple. There is not one optical fight inside an AI datacenter but two: inside the rack (scale-up) is a CPO fight, and between datacenters (scale-across) is a coherent DCI fight. Meta linking campuses up to 2,000 km apart signals that independent demand is opening for the latter, the coherent layer. It sits in exactly the distance band Marvell spells out for its own COLORZ 800 pluggable, 2,000 km at 600G and 3,000 km at 400G.[2] Tickers: $MRVL $COHR $CIEN $LITE, and on the demand side, $META.

Contents

Intro: why optics-investment talk stays inside the rack

Why the space between datacenters pushes toward coherent

Coherent and DWDM: more light down a single fiber

The supply map we drew three times

The scale-across coherent DCI layer: who stands here

But is this a bet on Meta alone

Scenarios and what to watch

1. Intro: why optics-investment talk stays inside the rack

A single coherent pluggable can carry 400G traffic across a 3,000 km DCI span, plugged directly into a switch or router port rather than a standalone transponder shelf. That is the reach Marvell spells out for its own COLORZ 800.[2] Why would anyone suddenly need a thing like this? The answer is in the Meta infrastructure breakdown SemiAnalysis published today.[1] When people think AI optics, they mostly look inside the rack: the NVLink that binds GPUs together, CPO (Co-Packaged Optics), and who supplies the light source (CW laser). But the money flow that surfaced today was not inside the rack. It was in the space between datacenters.

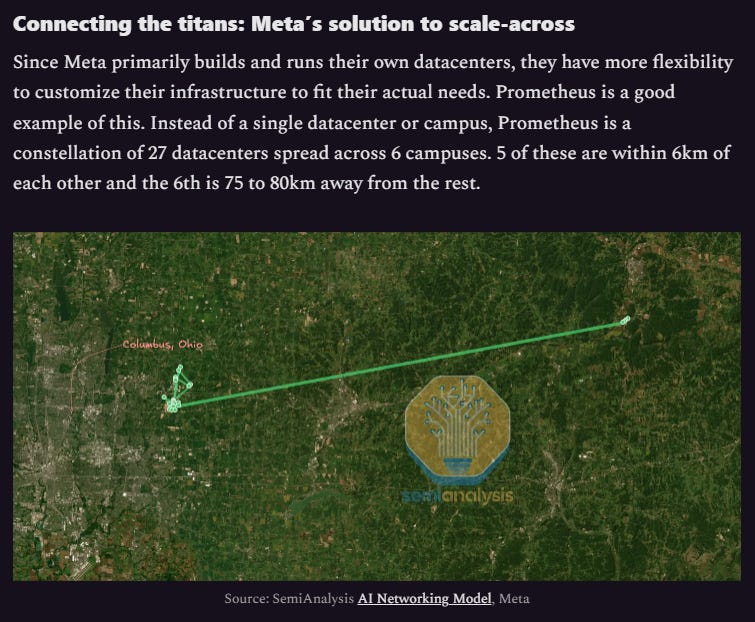

Per the Meta analysis SemiAnalysis published on July 10, Meta is building five 1GW-class “titan” clusters at once, and to use them as single training resources it has to stitch campus to campus with fiber.[1] SemiAnalysis describes this campus-to-campus segment (its L4 layer) as a mix of LR optics and DWDM-plus-ZR-optics systems, chosen by fiber distance.[1] (These figures and the naming are SemiAnalysis’s own model estimates, not values Meta has confirmed.)

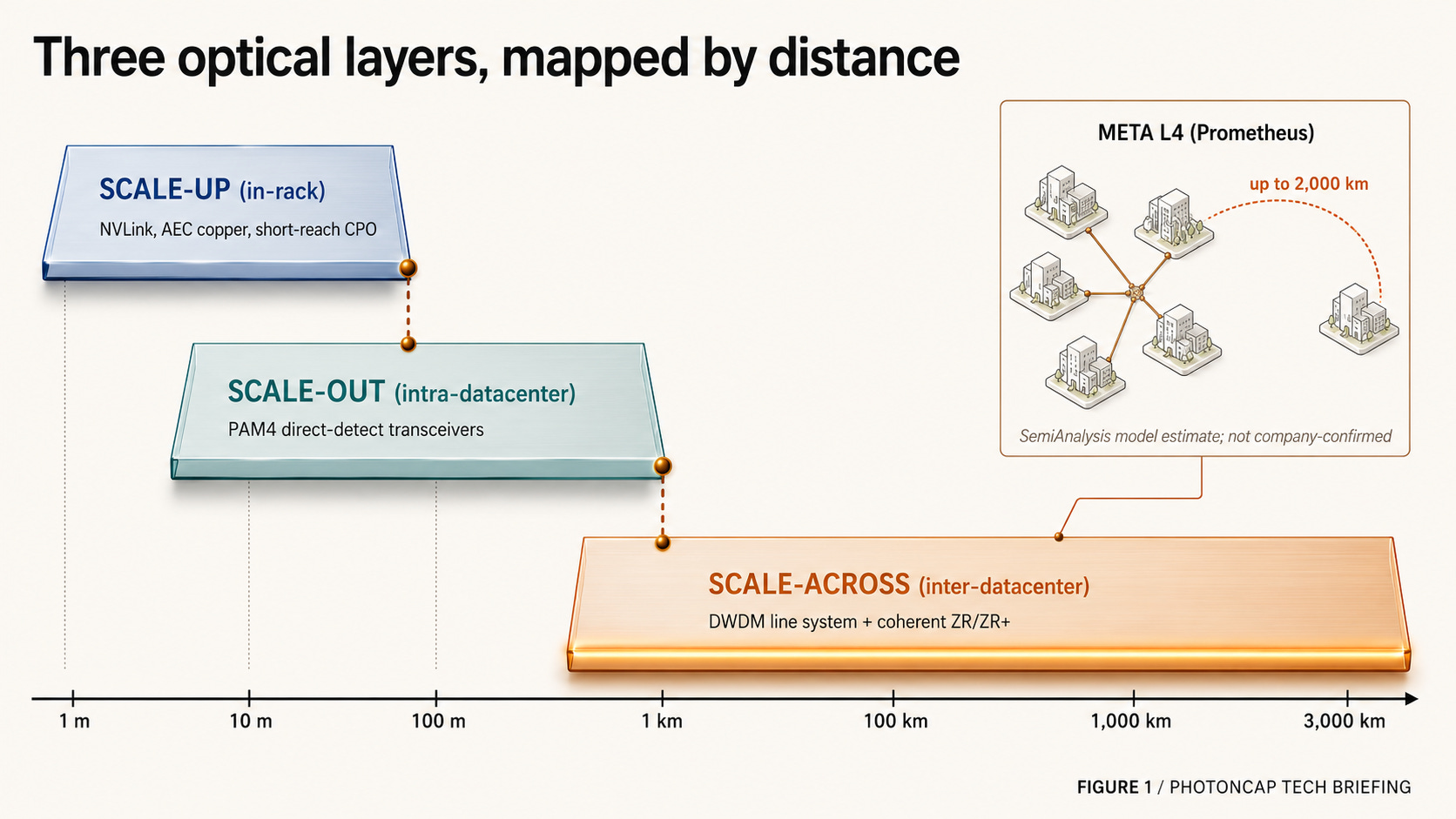

That is where the optical market splits into two layers. One is the scale-up fight, turning copper into light inside the rack. The other is the scale-across fight, connecting datacenters set tens to thousands of kilometers apart. The first points toward CPO; the second points toward coherent DCI (Data Center Interconnect). The market has mostly watched the first, but Meta’s blueprint shows independent optical capex opening outside the rack too, specifically at the campus-to-campus scale-across layer. Not every scale-across link is coherent, of course. Short campus spans still use LR optics, and around 10 to 20 km, IMDD and coherent-lite overlap. But the moment the campus-to-campus structure opens from tens of kilometers out to 2,000 km, the investable point moves off CPO and onto DWDM and ZR/ZR+ coherent DCI.

2. Why the space between datacenters pushes toward coherent

Distance sets the answer. Split the three layers by distance and it looks like this. Scale-up is inside the rack, meters to tens of meters; copper (NVLink, AEC) holds here, and short-reach optics like CPO step in at the limit. Scale-out is inside the building, hundreds of meters; that is the PAM4 optical transceiver zone. Scale-across is building to building, campus to campus, kilometers to thousands of kilometers. Once that distance runs past tens of kilometers into regional and long-haul, direct detect alone (IMDD, switching light intensity on and off) can no longer meet the economics and the performance, and DWDM line systems together with coherent ZR/ZR+, which also carries phase, move to the center. The coherent DSP that undoes the resulting distortion is the heart of this layer.

The physical reason is latency. Light travels slower in fiber than in vacuum, about 208,000 km per second. SemiAnalysis notes that the one-way latency to a site 100 km away is already roughly 500 microseconds on the speed-of-light limit alone,[1] a floor physics sets no matter how good the gear is. A simulation the Corning team presented at OFC 2026 points the same way: in data-parallel training, the optimal distance between two clusters is roughly 10 to 100 km, and beyond that, communication starts to crowd out computation.[3]

So the training method itself splits. Synchronous pretraining stays inside one region, while workloads that can be coupled loosely, like RL (reinforcement learning, where a model learns to solve tasks from reward signals rather than by copying labeled answers), get spread across the globe under an asynchronous strategy.[1] This is where the investable point turns. It means the traffic between campuses is defined by bandwidth and distance, not ultra-low latency. Since you cannot hit ultra-low latency anyway, you send latency-tolerant workloads and instead push as many bits as far as possible per fiber. Coherent DCI is exactly the gear that solves that problem.

3. Coherent and DWDM: more light down a single fiber

At the link level, the reason coherent moves to the center over longer distances is simple. IMDD (direct detect), used at short range, tells 0 from 1 by light intensity alone. It is simple, so it is cheap and low power, but as distance grows, fiber dispersion (different wavelengths arriving at different times) and loss smear the signal. Coherent carries phase along with intensity, and a powerful coherent DSP at the receiver mathematically reverses that distortion. It costs more, but the payoff is holding a far longer span than plain IMDD and pushing per-fiber capacity much higher. That said, spans of hundreds to thousands of kilometers usually run on top of a DWDM line system with optical amplification (EDFA or ILA, in-line amplifier) and ROADMs in place. A coherent module does not mean “thousands of kilometers with no amplification”; it means maximizing bits per fiber on top of that line system.

DWDM (dense wavelength division multiplexing) rides along with it, carrying dozens of wavelengths down one fiber at once. Since laying new fiber between campuses is so expensive, wringing the most bits out of a strand already in the ground is the core of the economics, and coherent plus DWDM is the direct way to raise bandwidth per fiber. This used to live in the large transponder boxes of carrier backbones, but the function has moved into small pluggable form factors like QSFP-DD and OSFP. That is the backdrop for IP-over-DWDM, plugging a coherent module straight into a router. As datacenter traffic grew to carrier scale, that function moved into datacenter gear.

Figure 1: Scale-up / scale-out / scale-across layer map by distance, with Meta’s campus-to-campus (L4) structure overlaid

This much is the physics and the structure. An optical layer links datacenters, and in a hyperscaler’s actual blueprint that layer is growing to gigawatt scale. And this is not something that surfaced only today.

PhotonCap has already covered the supply side of this layer three times.

4. The supply map we drew three times

First, in our piece mapping NVIDIA’s March optical investments across the scale-up / scale-out / scale-across layers (NVIDIA optics piece), we defined the scale-across band as “2 km to 3,000 km, coherent ZR/ZR+ required” and placed Marvell’s COLORZ ZR/ZR+ line there.

Second, in our piece on Marvell’s acquisition of the Swiss plasmonics startup Polariton (Marvell Polariton piece), we flagged that Marvell IR named the acquisition target, in so many words, as scale-across, DCI, ZR/ZR+ coherent, and 3.2T and beyond. Polariton POH is the device-level IP for long-reach coherent modulation inside the Marvell stack.

The Truth Behind Marvell-Polariton: Is LWLG the First Candidate, or Just a Backup Bet?

On April 22, 2026, Marvell acquired Polariton Technologies, an ETH Zurich spinoff. The press-release target: “3.2T and beyond.” Marvell acquired Polariton’s POH slot architecture, device IP, and engineering team. But the chromophore that operated the public record device remained outside Marvell’s disclosed acquisition perimeter.

Third, in our Marvell earnings piece (Marvell earnings piece), we set a monitoring point: COLORZ 1.6T ZR/ZR+ DCI module sampling in the second half of 2026, built on a 2nm coherent DSP, and whether Marvell takes the early lead in the scale-across market.

The Third Signal in May: Marvell Confirms the AI Optical Signal from Lumentum and Coherent

Over a single month in May, the same demand signal emerged from three layers of the AI optical supply chain. Laser source (Lumentum, 5/5), transceiver/CPO (Coherent, 5/6), DSP/switch/SiPh (Marvell, 5/27). All three companies raised their forward demand visibility for AI optical interconnects, and all three secured $2B strategic commitments from the same counterparty: NVIDIA. Marvell posted Q1 FY27 revenue of $2.418B (+28% YoY), raised its interconnect growth outlook from +50% to +70%, and lifted FY28 revenue guidance to $16.5B, a $1.5B increase. This article analyzes the Marvell earnings while mapping why all three earnings paint the same picture, and where each company and layer sits within that picture.

The question all three answered was who makes the parts and chips for this layer. Today’s SemiAnalysis piece on Meta fills the other side: who actually deploys it at gigawatt scale. Supply and demand met at the same coordinates.

Which leaves one question. Who takes the revenue in this 2,000 km segment as pluggable coherent replaces standalone transport, and who is vertically integrated from laser to module? And is this a bet on Meta alone, or is it structural? That is where the piece turns.