Everyone Saw a Laser Shortage. The Money Went to the Foundries First.

$TSM $GFS $UMC $TSEM $SOI $SLOIF $XFAB + TFLN/Packaging | SiPh Foundry Capacity & Pricing Power

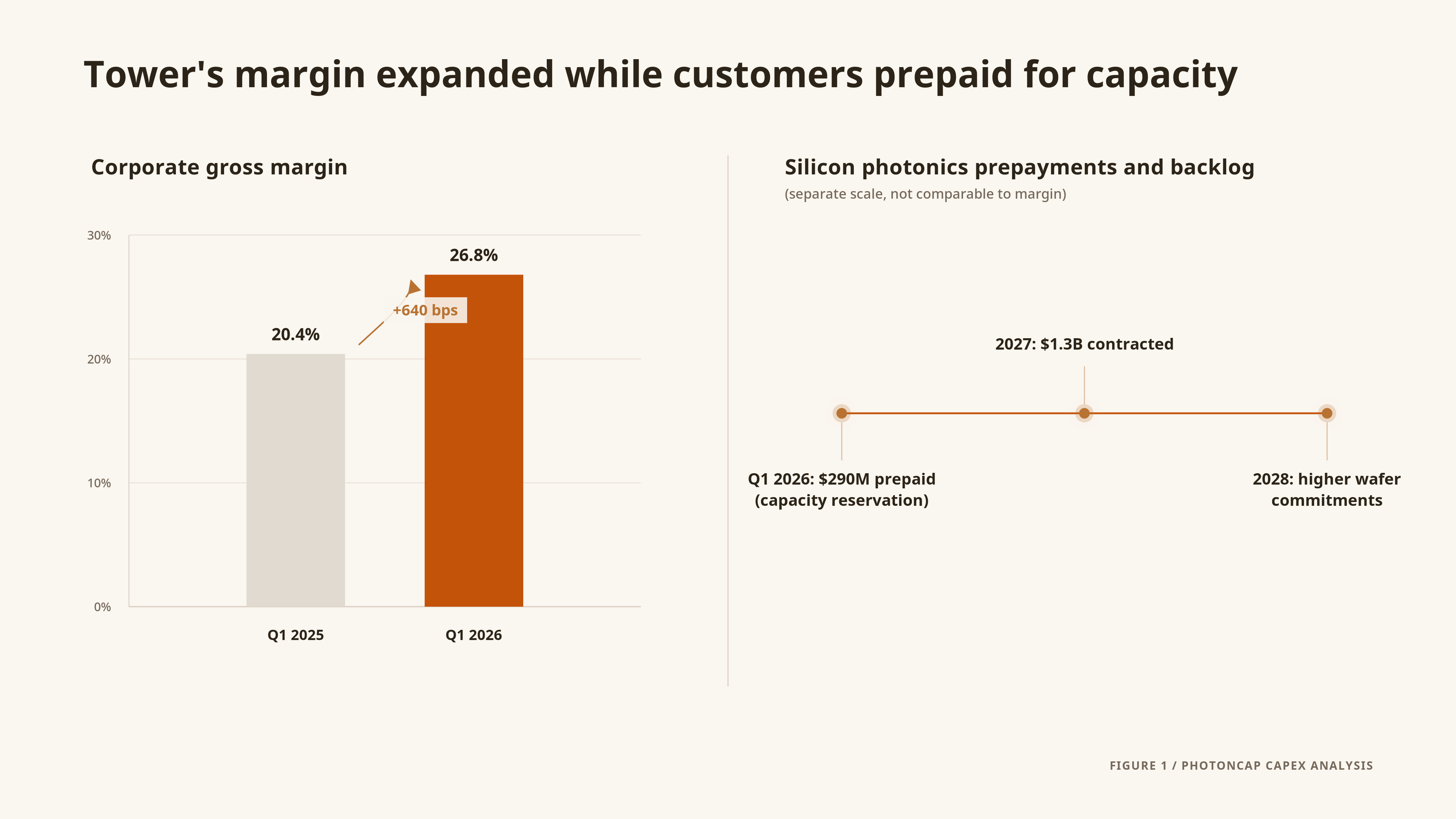

When AI data centers move from copper to light, the market looks at laser companies first. Lumentum, Coherent, the EML and CW laser shortage. That is the most intuitive story. But in this cycle, the money moved first not into lasers but into the SiPh foundry layer. Tower has locked in $1.3B of silicon photonics contracts on a 2027 revenue basis, and in the same quarter it took in $290M of customer prepayments, which Tower states are for capacity reservation.[1] Corporate gross margin rose from 20.4% in Q1 2025 to 26.8% in Q1 2026.[2] When capacity is scarce, customers pay up front for capacity that has not been built yet. The investment question is narrower: which layer can turn scarcity into margin. Foundry capacity, SOI wafers, InP materials, and CPO packaging are all tight, but they do not capture value the same way. The market watches the laser suppliers; this piece follows the capacity that fabricates, packages, and tests the optical engine. $TSM $GFS $UMC $TSEM $SLOIF $XFAB.

Tower Has Already Shipped 5 Million Coherent PICs

On June 18, 2026, Tower Semiconductor (TSEM), together with Marvell, announced it had shipped over five million coherent PICs cumulatively. A coherent PIC has to control not just the amplitude of light but its phase and polarization, which is a higher process bar than a direct-detect part. It is the most recent evidence that AI data center interconnect (DCI) is moving to light.[3]

The number itself is not the point. It matters because Tower is already producing at this scale, and that overlaps with another number from the same company.

A semiconductor foundry usually does not take money from customers up front. It builds the fab, installs the tools, ramps yield, then sells wafers to recover the cost. So a foundry’s biggest fear is an empty fab. Yet Tower booked $290M of silicon photonics customer prepayments into its Q1 2026 cash flow, and stated these were for capacity reservation. Its silicon photonics contracts stand at $1.3B on a 2027 revenue basis, the 2028 wafer commitment is larger still, and further prepayments arrive through January 2027.[2][1] Corporate gross margin rose from 20.4% in Q1 2025 to 26.8% in Q1 2026 ($111M gross profit divided by $414M revenue).[2]

The combination is unusual. Tower has a production shipment record in coherent PICs, while customers are prepaying to reserve capacity that is not built yet. In Tower’s own wording, actual demand and shipment forecasts run higher than the contracted $1.3B.[1]

That is the inversion in this cycle. Investors framed the optical transition through lasers (LITE, COHR, the EML and CW shortage), but the first hard pricing signal appeared at the foundry layer.

Figure 1. Tower’s corporate gross margin expanded while SiPh customers prepaid for capacity reservation. Source: Tower Semiconductor Q1 2026 results and the $1.3B silicon photonics contract announcement.

This Is a Capacity Problem, Not a Technology Problem

As AI clusters grow, copper interconnect loses on power, reach, and equalization cost. So from 800G to 1.6T and then 3.2T, the optical share of the link can only rise. The market already prices some version of that transition.

The hard part is not deciding to use light. It is manufacturing the PICs that handle it. A SiPh PIC cannot be fabricated at a generic CMOS fab. The waveguide (the path the light travels), the modulator (electrons to light), the photodetector (light to electrons), Ge/Si integration, optical test, and packaging all have to line up together. Mainstream SiPh for high-performance AI datacom runs on 200mm and 300mm CMOS-compatible foundry processes, and the larger foundries are pushing toward 300mm. Production-scale supply is concentrated in a small group of qualified foundries.

So the AI optical cycle turns from a game of who designs it into a game of who holds the production capacity.

I covered who is technically ready in this field in our Samsung silicon photonics piece. This piece takes a different angle. Who holds the capacity, and how it shows up in price and margin.

Samsung's Silicon Photonics Bet: Too Late Against TSMC, GFS and Tower?

Samsung’s Silicon Photonics Bet: Too Late Against TSMC, GFS and Tower?

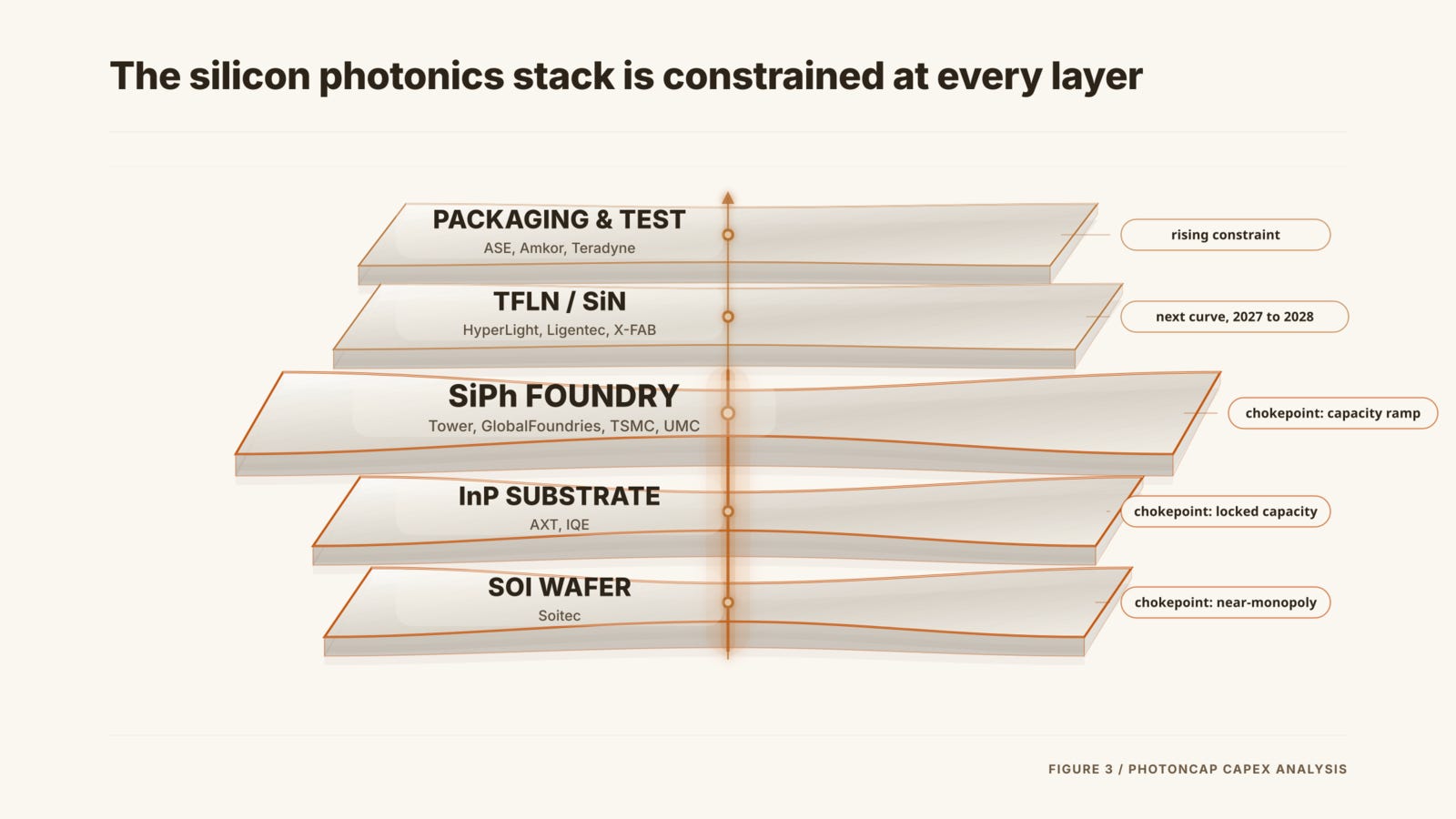

This bottleneck does not end at the foundry layer. To fabricate a SiPh PIC you need photonics-grade SOI wafers underneath, and one company supplies the overwhelming share of those wafers. I looked at it in our Soitec piece. To make the lasers you need InP (indium phosphide) substrates, and as flagged in our AXT deep dive, NVIDIA locking up capacity has stretched lead times out past 2027.

The Wafer That Used to Roll Around My Lab Is Now an AI Data Center Bottleneck: Soitec and the Investment Case for the Photonics-SOI Monopoly

As AI data centers accelerate the transition from electrical to optical interconnects, demand for SOI (Silicon-on-Insulator) wafers, the critical substrate for silicon photonics (SiPh), is growing rapidly. This article analyzes Soitec’s (EPA: SOI) technological moat (3,500+ Smart Cut patents, no competitor with meaningful Photonics-SOI volume identified from public sources), financial profile (FY2025 revenue of €891M, Photonics-SOI approaching €100M scale), and the reality behind the SiN platform threat narrative. Soitec’s stock rallied from its December 2025 low of €23 to €78 as of April 15, 2026, a YTD gain of +213%, as the market began pricing in its SiPh/CPO positioning. But the actual Photonics-SOI revenue scale-up is still in its early innings. The real test comes over the next 2 to 3 years as 1.6T/CPO ramps accelerate. Related tickers: $SOI (EPA), $SLOIF (OTC), $GFS, $TSEM

AXT Inc. (AXTI) Deep Dive: The Hidden Bottleneck in AI Optical Interconnects

1. The Hook: Why Pay Attention to Indium Phosphide (InP) and AXT Inc. Now?

Both upstream bottlenecks have already shown up in the share prices. As of June 20, 2026, Soitec (Euronext Paris: SOI, US OTC: SLOIF) was up roughly +54% from our April 15 coverage and AXT (AXTI) roughly +96% from our March 3 coverage (price basis). The moves cannot be attributed to a single catalyst, but they show the market has started to price upstream materials scarcity. AXTI in particular has been volatile on recent InP-related news.

Figure 2. SLOIF and AXTI re-rated after PhotonCap coverage. Source: Euronext Paris and Nasdaq pricing, indexed to 100 at each coverage date. As of June 20, 2026.

SOI wafers, InP substrates, foundry fabs, and packaging. Nearly every layer of the stack is tight at the same time.

Everyone Is Adding Capacity, But Demand Is Faster

By company, the field breaks down like this.

Tower is expanding its global multi-fab SiPho capacity substantially. The company calls it a substantial capacity ramp, and it is the foundation of its 2028 $2.8B revenue model.[1] The 2027 $1.3B of contracted revenue and the prepayments above are the demand base under it.

GlobalFoundries acquired AMF, the Singapore-based SiPh foundry, in November 2025, becoming the largest pure-play SiPh foundry by revenue.[4] AMF adds over $75M in 2026 revenue, and GFS pulled its target for crossing $1B in SiPh revenue forward from 2030 to 2028.[5][6]

TSMC moves with COUPE, but its role is a bit different. It fabricates the chip while also being the packaging backbone (CoWoS, SoIC).[7][8]

UMC entered in December 2025 by licensing imec’s iSiPP300, targeting risk production in 2026 to 2027[9], and it is taking TFLN (HyperLight/Wavetek) at the same time.

Samsung has also entered, but it has no public production track record or design win yet.

Meanwhile, LightCounting calls 2026 “the year of silicon photonics,” expecting more than half of all optical transceiver revenue in 2026 to come from SiPh modulator-based products. That was 10% in 2018 and 33% in 2024.[10] The demand curve is steeper than the capacity build.

Figure 3. The silicon photonics supply stack is constrained at every layer. SOI wafer to InP substrate to foundry to TFLN/SiN to packaging and test. The materials and foundry layers are the current chokepoints.

The free takeaway is straightforward. SiPh capacity is short.

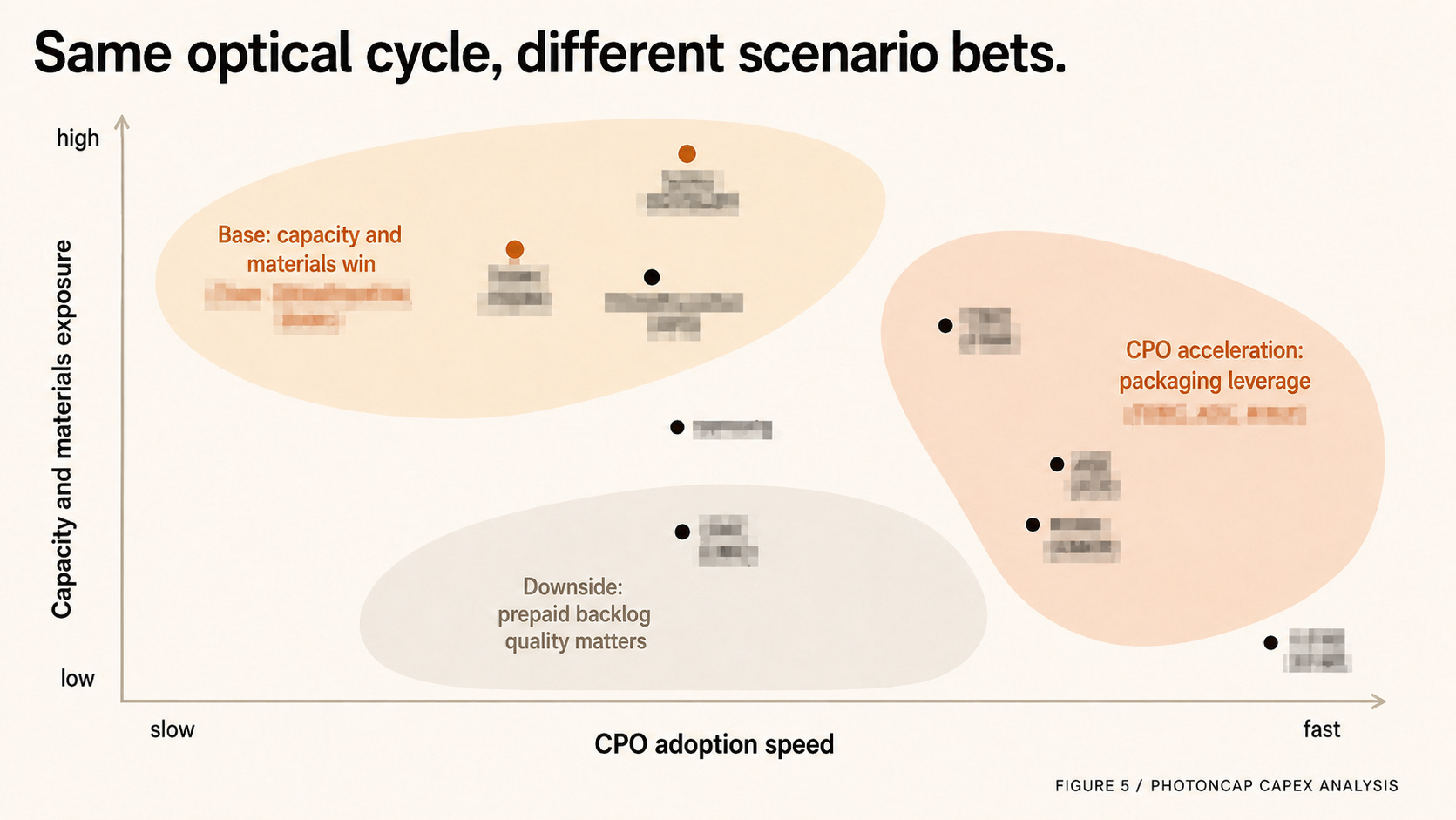

The investment question is where that shortage converts into margin. Tower and GFS both point to prepayments, but the quality of those signals may differ. Soitec may be the cleaner upstream bottleneck. And if CPO accelerates, value capture may move toward TSMC and OSAT packaging instead. Below, we split the supply chain into foundry, SOI, InP, TFLN, SiN, and packaging and test, and look at which layer is most defensive.