DSP, LPO, NPO, CPO: The Four Optical Architectures and the Light Source Beneath Them All

$LITE $COHR $AAOI $SIVE $POET | Optical Architecture Primer + Light Source Map

On June 9, an institutional-only SemiAnalysis note lit the fuse, and optics names dropped together. AAOI fell 14%, COHR 11%, LITE 8% [1][2]. The market’s logic was simple: “CPO volume slips to 2028 to 2029, so photonics is over.” Yet the very next day the same names bounced (AAOI +7%, LITE +5%, COHR +2%) [3], and in the same week NTT, SK, and Chunghwa Telecom launched a new $500M fund pointed at optical communications and light sources [4][5]. This piece lays out the four optical architectures, DSP, LPO, NPO, and CPO, in a way a non-specialist can absorb in one read, then maps where Lumentum, Coherent, AAOI, and Sivers actually sit on that ladder. The thesis is one sentence. Photonics is not CPO. CPO is one form factor among several, and the light source, substrate, and fiber sit inside every one of them.

Table of Contents

In the Same Week, Two Opposite Things Happened

Why “Photonics Equals CPO” Is the Wrong Equation

The Optical Architecture Ladder: DSP · LPO · NPO · CPO (Pluggable+DSP / LPO / NPO / CPO)

So Why Does This Matter for Investing

Form Factor by Form Factor: What Gets Removed, What Stays

The Copper-Light Boundary: Lane Speed Pushes the Line Inward

The Light Source Map: Lumentum · Coherent · AAOI · Sivers

Capital Votes on the Destination, Not the Quarter

Copper Runs Longer. That Is Not a Bear Case.

Scenarios and Monitoring

Closing: Look Far, Not at Tomorrow

The PhotonCap Series Behind This Piece

Coherent, Lumentum, Marvell, and Now Corning: NVIDIA’s 4 Photonics Bets · COHR, LITE, MRVL, GLW

NVIDIA’s $2B Marvell Bet and Celestial AI’s “25x” Claim · MRVL, interconnect

The Silicon Photonics Light Source War: Same Problem, Three Solutions · Sivers, QD Laser, Aeluma

Intro: In the Same Week, Two Opposite Things Happened

On June 9, optics stocks fell apart in a single session. AAOI led the way down 14%, with Coherent off 11%, Lumentum 8%, and Ciena 7% [1][2]. The trigger was an institutional-only note from SemiAnalysis. It reportedly said CPO (Co-Packaged Optics) volume timing is later than hoped, and outlets relayed summaries without confirming the original [1].

The story the market read was this: “CPO is late. CPO is photonics. So sell photonics.” The middle sentence is wrong, and the selling started from there.

That there is no such thing as a “CPO stock” is the argument I made in yesterday’s part 1. Today’s part 2 builds on it: draw the optical architecture once, and you can see why that middle sentence is wrong.

The same week ran the other way too. On June 10, the names that fell the day before simply bounced back. AAOI +7%, Lumentum +5%, Coherent +2% [3]. And that same day, at NTT headquarters in Tokyo, NTT, SK Telecom, Taiwan’s Chunghwa Telecom, and the Development Bank of Japan (DBJ) announced the IOWN AI Fund. Size $500M (about 760 billion won), with a management company, Catalight Capital, based in Silicon Valley and Tokyo. The stated investment scope names “Photonics Technologies,” “Light Source and Modulators,” and “optical communications” outright [4][5][6].

On one side, a “CPO is late, so sell the light” wave. On the other, telecom carriers and financial capital putting fresh money into “light.” Both in the same week. One of them is misreading the clock.

The June 9 selloff translated “CPO delay” into “sell photonics.” Whether that translation holds becomes a one-minute judgment once you know what the optical architecture actually looks like.

Why “Photonics Equals CPO” Is the Wrong Equation

Start with an analogy. There is a power plant, and there are lamps that run on its electricity. Lamps come in types: ceiling fluorescents, desk lamps, recessed wall fixtures. CPO is the “recessed wall fixture.” It is fiddly to install, and the work can run late.

But you do not sell the power plant because the recessed fixtures are behind schedule. Fluorescents, desk lamps, and recessed fixtures all draw from the same plant. In CPO terms, the “power plant” is the light source, the substrate, and the fiber. Whatever form factor you choose, light has to be generated somewhere, modulated or routed through something, and carried somewhere.

Many of the names sold off on June 9 are closer to “power plant companies” than “fixture companies.” Lumentum and Coherent make lasers, transceivers, and materials, a layer that pluggable, LPO, and CPO all need. The plant stock fell on news that the recessed fixtures are running late.

This either-or, “CPO or copper,” is not new. Back in March, when Broadcom’s Hock Tan said on the earnings call that copper could carry the within-rack job and that CPO would arrive in time, not in 2026 or 2027, the market read it the same way, as a fight between a copper camp and an optics camp. As I laid out in NVIDIA’s $4 billion optics bet, Broadcom and NVIDIA were not in conflict but looking at different axes of time and distance. Inside the rack at 0 to 2 meters, copper is right for 2026 to 2027. Across clusters at 10 to 100 meters, optics is right for 2028 to 2030. This CPO delay panic is just the June version of that same frame.

So how do you tell “plant” from “fixture”? You learn the optical architecture ladder.

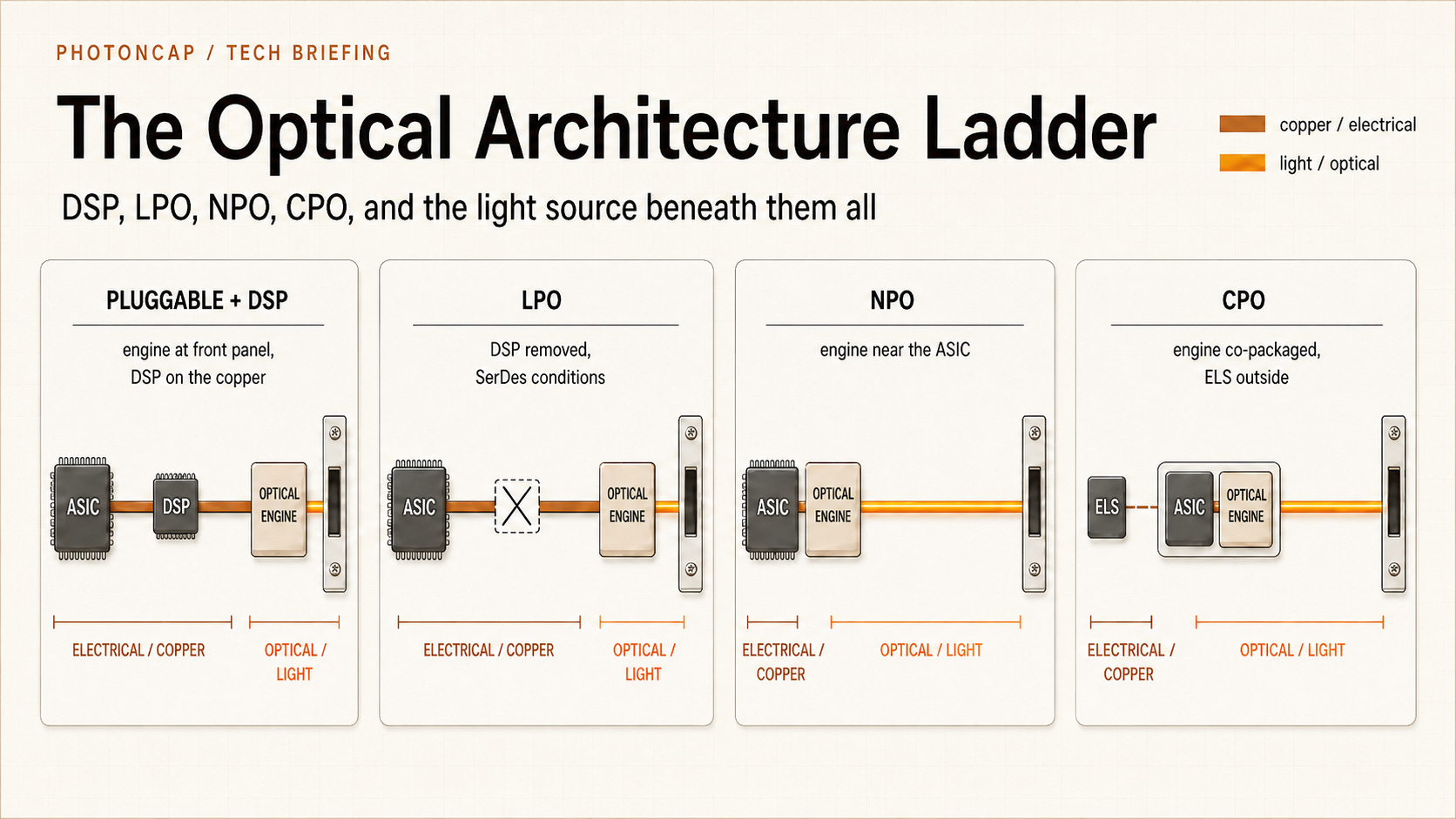

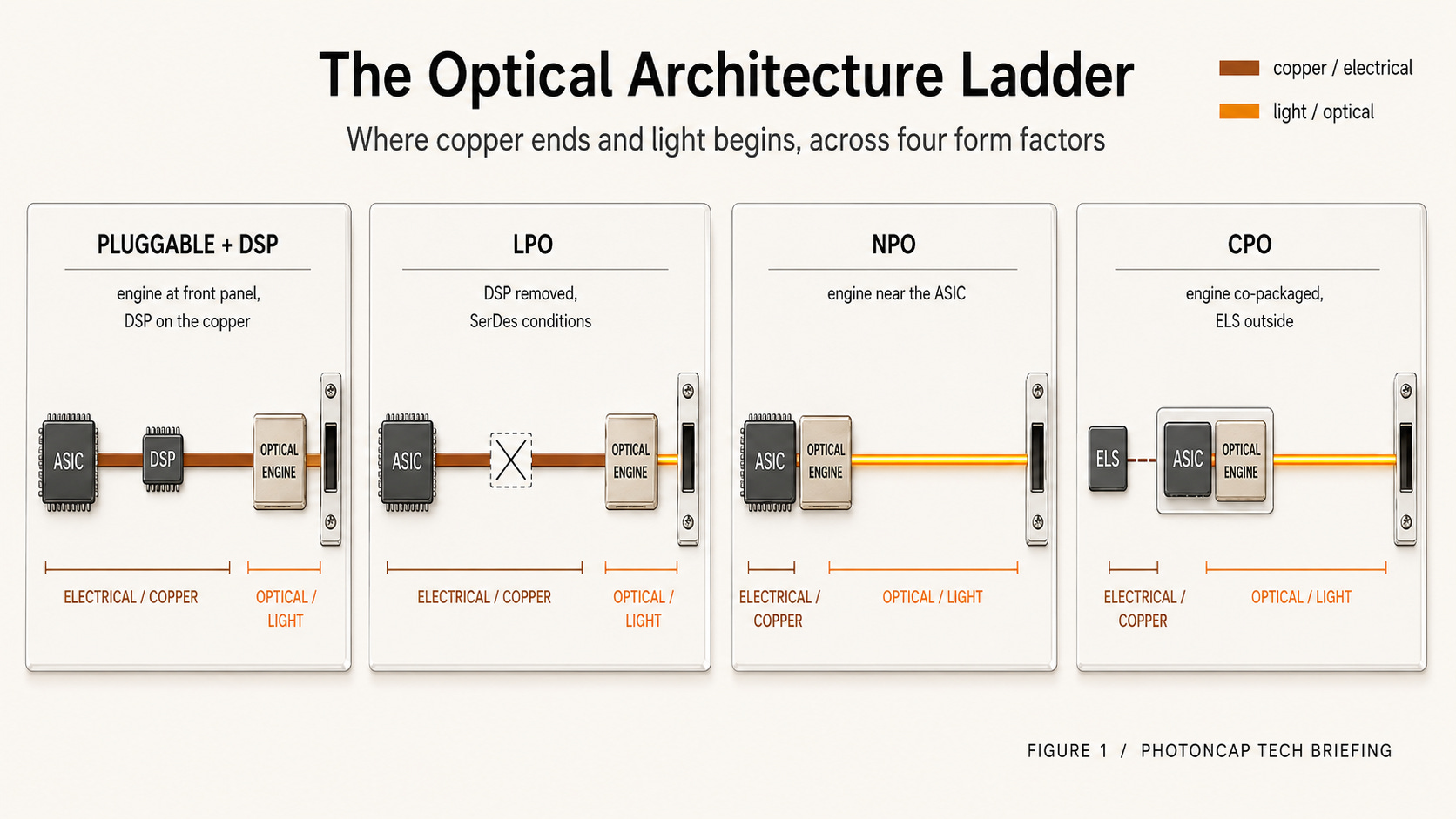

The Optical Architecture Ladder: DSP, LPO, NPO, CPO in One Pass

This ladder is best read along two axes. One is how close to the ASIC you put the optical engine. The other is where you restore the degraded electrical signal. LPO is a move along the second axis: it removes the module DSP and leans more on the host ASIC’s SerDes. NPO and CPO are moves along the first axis: they pull the optical engine toward the ASIC. The optical engine (the cluster of optics that makes and receives light) and who restores the signal, those two together are what name every form factor.

Why does that matter? Because the electrical signal coming out of the AI chip (ASIC) travels over copper wiring. The faster the signal goes (these days over 200G per lane in PAM4), the faster it degrades on copper. There are only two ways to deal with that. One is to attach a chip (DSP) that restores the degraded signal. The other is to pull the optical engine closer to the ASIC and cut the copper distance outright. The ladder is the process of shrinking the copper electrical run by reducing the DSP, pulling the optical engine toward the ASIC, or combining the two. Let us climb it.

Rung 1. Pluggable + DSP (today’s standard)

The optical engine sits inside a swappable module that plugs into the switch front panel. The 800G and 1.6T transceivers you usually hear about are this. Electrical signals from the switch ASIC travel across copper PCB to the front panel, and the longer that run, the more the signal degrades, so a DSP (Digital Signal Processor) inside the module restores it. It is the most mature and most proven approach.

Definition: optical engine inside a pluggable front-panel module. Today’s 800G/1.6T standard.

How it works: ASIC to copper PCB to front-panel module. The long run degrades the signal, so the module’s DSP restores it.

Upside: standardized, hot-swappable (swap just the module on failure), long reach, the most mature ecosystem.

Tradeoff: the DSP is power hungry, and each module has a power and thermal ceiling, so rising bandwidth hits a wall.

Rung 2. LPO (Linear Pluggable Optics)

Same pluggable form factor, but with the module’s DSP removed. The switch ASIC’s SerDes handles signal conditioning instead, and the module’s amplifier (TIA) and driver simply pass the signal through in linear mode. The DSP was the most power-hungry part, so removing it brings power and cost down together [7].

Definition: same pluggable form factor, with only the module DSP removed, the “linear” version.

How it works: signal restoration moves from the module to the switch ASIC’s SerDes. The module only passes through.

Upside: power, cost, and latency drop with the DSP gone. Reuses existing pluggable infrastructure.

Tradeoff: performance can vary by host platform, so interoperability is tricky. A practical bridge before CPO.

Rung 3. NPO (Near-Packaged Optics)

The optical engine moves off the front panel to sit next to the switch ASIC on the main board. The electrical run shortens, so loss and power drop. It is a midpoint before full CPO, a compromise that captures some of the benefit at lower packaging difficulty than CPO.

Definition: optical engine pulled off the front panel to sit beside the ASIC on the board.

How it works: shortens the electrical path to board level, cutting loss and power.

Upside: some of CPO’s benefit at lower packaging difficulty. Easier to use the existing supply chain.

Tradeoff: less efficient than full CPO, and a board-level electrical path still remains.

Rung 4. CPO (Co-Packaged Optics)

The optical engine is co-packaged on the same package as the switch or GPU ASIC, right beside it. The electrical signal barely moves, so power efficiency is best. The catch: lasers are heat sensitive and hard to place beside a hot ASIC, so the laser is pulled out into a separate module outside the package. That is the External Light Source (ELS). It is the most efficient, but packaging and yield are the hardest, so volume comes latest.

Definition: optical engine co-packaged with the ASIC, the final rung.

How it works: minimizes the electrical path. The heat-sensitive laser is split out into an external ELS.

Upside: best power efficiency and bandwidth density. The copper electrical wiring nearly vanishes.

Tradeoff: highest packaging, yield, and test difficulty, so volume comes last. This is exactly the rung SemiAnalysis called late.

The Whole Ladder in One Line

We climbed all four rungs, but the point is not the ladder itself. It is the shared foundation under all four rungs. Whether rung 1 pluggable or rung 4 CPO, light is made in a laser (the source), modulated on a substrate, and carried on fiber. Silicon is not an efficient light-emitting material in the first place (I covered this in detail in the earlier light source piece), so most commercial silicon photonics links bring in a III-V light source separately, as an ELS or through hybrid integration. So whether DSP is removed (LPO) or the engine relocates (NPO, CPO), those three layers, light source, substrate, and fiber, do not drop out of any form factor.

One more thing. This ladder is also a story about where light begins. Short distances (inside one rack) still favor copper, and from longer distances (rack to rack) light takes over. Which way that boundary moves over time is what actually sets the pace of the whole ladder. I unpack this in detail later, as copper demand versus light demand.

[Figure 1: The optical architecture ladder. Four form factors from pluggable+DSP to CPO, with the copper (electrical) line and the optical (light) line color-distinguished, the copper segment shrinking and the optical engine moving toward the ASIC up the rungs]

To restate it, what SemiAnalysis called late is rung 4, CPO. And not “CPO will not happen” but “large-scale volume timing slips,” a speed claim. Rungs 1, 2, and 3 keep selling in the meantime, and all four draw on the light source and fiber beneath them. So selling the entire optical layer on the single sentence “CPO delay” is a trade that fails to separate the form factor from the shared component layer.

So Why Does This Matter for Investing

That is the picture I can lay out for free. The architecture is a ladder, CPO is the top rung, and the foundation beneath is shared.

The real question starts here. Among the names that fell together on June 9, who is CPO-dependent and who is not? Who is the plant and who is the fixture? Was Lumentum’s drop justified, or was it a power plant swept up in fixture news? Where does the EML that AAOI makes hang on the ladder? Does a pure light-source company like Sivers fall with CPO if it slips, or is it actually safer?

And the direction of capital. Was it a coincidence that NTT and SK put $500M into optical communications in the same week, or are they looking at the destination of the whole ladder?

One preview before the paywall. That AAOI fell hardest on June 9 (down 14%) and bounced hardest the next day (up 7%) is no accident. It is because of the rung AAOI stands on in the ladder. Where that rung is, and by the same logic why Lumentum is a “power plant” and why Sivers is actually safer, I work through one by one just below.

Below, I lay out the form-factor comparison quantitatively, map the four light-source companies onto the ladder, and itemize the capital that actually flowed into photonics in the second week of June. AAOI is a pluggable overshoot, Lumentum is laser capacity, Coherent is a composite materials-and-transceiver exposure, Sivers is the purest light-source option. Same selloff, but not the same bet.