There Is No Such Thing as a 'CPO Stock': How the Market Misread SemiAnalysis

$LITE $COHR $MRVL $AVGO $POET | CPO Delay Selloff, Reader Mailbag Edition

On June 9, an institutional-only SemiAnalysis note read as a “CPO rollout delay” and optical networking stocks broke in a single session. AAOI down 14%, COHR down 11%, LITE down 8%, CIEN down 7% [1][2]. But were the names the market sold really “CPO delay casualties”?

One reader asked about selling Lumentum, Soitec, and Sivers to rotate into Broadcom and Marvell. The instinct was right. The sense that you buy the fundamental layer, not the form factor, is right. The problem was that the execution pointed the opposite way.

This piece looks at three things the market missed in the CPO delay selloff: how CPO and 800VDC got bundled into one AI infrastructure delay trade, production versus volume, and the false category of a “CPO stock.” (Relevant tickers: $LITE $COHR $MRVL $AVGO, plus Soitec, Sivers, $POET.)

Contents

Intro: a reader’s trade

An institutional-only note, and a summary of a summary

The real order of the selloff: price first, explanation later

“Production has started,” but production is not volume

Many form factors, one set of toll-gates

Form-factor exposure matrix (LITE, COHR, Sivers, Soitec, POET)

The “safe haven” paradox

NVIDIA’s capital map

Buy the dip? Scenarios, downside, monitoring

References and sources

Intro: A Reader’s Trade, June 9

On June 9, intraday, more than ten DMs came in about this across X, Substack, and elsewhere. Here is one of the more specific ones, anonymized and close to verbatim.

“Photon Cap, SemiAnalysis just reported that CPO for NVIDIA Rubin Ultra is now delayed to 2028. I’m thinking about selling Soitec, Sivers and Lumentum tomorrow and shifting the money into AVGO and Marvell. What’s your opinion?”

The timing is perfect. Midday June 9, AAOI fell 14% and dragged the whole optical networking complex down with it [1]. COHR down 11%, LITE down 8%, CIEN down 7% [2]. The trigger was a note SemiAnalysis sent to institutional clients only, and the gist was that the CPO rollout slips later than the market expects [1].

The reader’s instinct gets one thing right. The feel of “don’t get pinned to a single form factor, buy the fundamental layer.” But the execution points the wrong way. In two places.

First, the premise got compressed. “CPO for Rubin Ultra in 2028” does not appear in any primary source, nor in any credible secondary one. What the note covered was two separate timelines. (a) NVIDIA’s large-scale adoption of native 800VDC lands around 2028, and (b) CPO shipment volume comes in below expectations in 2027 with full mass production slipping toward 2028 to 2029 [3]. The market bundled the two into a single “AI infrastructure buildout is slipping” trade and sold them together, and in the process the two timelines collapsed into one number, “Rubin Ultra CPO 2028.” 800VDC is a power architecture. CPO is an optical interconnect. Different layers, traded as one basket. Not because anyone mistook one for the other, but because they got de-risked together as one correlated theme.

Second, there is a category error. Lumentum, Soitec, and Sivers get bundled as “CPO plays,” so the logic runs: CPO is late, they die, therefore AVGO and Marvell are the safe zone. But once you see where AVGO and Marvell stand, the trade is tangled against its own premise. More on that below.

An Institutional-Only Note, and a Summary of a Summary

Sourcing first.

The June 9 note is not in any public newsletter or general paid tier. It is institutional-only [1]. One community write-up even concedes that the figures it quotes (800VDC 2028 / CPO 2027 shortfall / mass production 2028 to 2029) are based on “third-party summaries” [3].

One key word here. “Delayed” is not “dead” [3]. A timing debate and a demand denial are completely different stories. And this is not a claim that SemiAnalysis is wrong. What they made is a timing-and-magnitude call on the CPO volume ramp. What this piece makes is a mechanism call on which layer is pinned to which form factor. Different kinds of claims, and not in conflict. If anything, the Downside scenario PhotonCap wrote on June 4 sits close to their base case. More on that later.

Taiwan GTC (Computex 2026): CPO Just Entered Production, So Why Are Coherent and Lumentum, the Companies It Was Supposed to Kill, Still on the Supplier List?

On May 31, 2026 (US press release date, Taiwan GTC Taipei keynote), NVIDIA called Spectrum-X Ethernet Photonics “now in production.” It is the world’s first co-packaged optics (CPO) Ethernet switch built on 200G SerDes, with CoreWeave, Lambda, and Oracle Cloud Infrastructure among the first adopters. One caveat up front: “now in production” marks the start of a manufacturing ramp, while broad availability is guided to the second half of 2026, so the two should be read separately. CPO pulls optical I/O right next to the switch silicon, so the market’s first reaction was pluggable transceiver cannibalization. Yet on the 11-partner supply chain list NVIDIA disclosed back in 2025, the very companies that build pluggables (Coherent, Lumentum) show up again as CPO suppliers. This piece looks at who actually builds what behind that one-line “production” claim, and how cannibalization and upside can happen inside the same company at once.

What retail saw was not the original. It was a summary of a summary. Closing that gap is where this piece begins.

The Real Order of the Selloff: Price First, Explanation Later

One question remains. If retail cannot see the report, how did the selloff hit intraday? Reverse the order and the answer appears.

Institutions read it first. A SemiAnalysis institutional-only note reaches institutional clients, hedge funds, long-short and pod-shop desks, and tech-specialist funds before anyone else [1]. Optical was already a crowded trade, with AAOI, LITE, COHR, GLW, and MRVL bid up on the CPO and NVIDIA photonics narrative. In a seat like that, one line saying “2027 volume is too rich” is enough to trigger de-risking. Institutions read the original and trim, retail has not seen it yet, and this is not the first time a big technical claim made the market sell first and do the work later. Price moves first, and the explanation gets attached afterward [4].

Then Seeking Alpha and Tae Kim report “why it fell,” and the public learns the event. Tae Kim, on the same day, read NVIDIA executive comments as refuting the SemiAnalysis narrative rather than confirming it [5]. Last, KuCoin, Futu, and coin-news feeds recompress the summary into something louder. “800VDC delayed,” “CPO delayed,” and “mass production 2028 to 2029” collapse into one line, and the reader’s “Rubin Ultra CPO 2028” is born right here [6].

Unfold the timeline and you can see where this “delay” narrative was assembled. The January CPO Book already noted that CPO deployment, economics, and serviceability are not simple [7], and the March “Inference Kingdom Expands” said Rubin’s in-rack scale-up stays copper-centric while CPO goes rack-to-rack and into larger world-size links [8]. The May 26 “Inside the 800VDC Revolution, Part 1” framed 800VDC as a four-phase gradual shift, with the facility-level move landing in 2028 to 2029 [9]. None of these described “Rubin internals all CPO by 2028.” The picture got synthesized when the market laid one line from the June 9 note on top of all this.

The selloff did not happen because retail read the report. It happened because institutions read it first, trimmed first, and the public learned the headline only after the price had already moved. That order is the gap PhotonCap exists to close.

“Production Has Started.” But Production Is Not Volume

The same week, the data on the other side.

NVIDIA’s own blog states Spectrum-X Ethernet Photonics is “now in full production,” with CPO-based next-generation Spectrum-X switching going into scale-out and scale-across deployments on the Vera Rubin platform. It named CoreWeave, Lambda, and Oracle Cloud Infrastructure as the first adopters, and broke the silicon-to-system pipeline into layers: TSMC (silicon photonics fab), SPIL (chip-scale packaging and test), TFC (laser die modules), and Foxconn (system assembly) [10].

At GTC Taipei, networking SVP Gilad Shainer said the CPO switch developed with TSMC had begun shipping to select partners, at up to 400 Tb/s, with production capacity expanding in 2H26 [11][12]. These remarks predate the June 9 note. They were made on the GTC Taipei floor on June 3 and 4, and were re-summoned after the selloff as NVIDIA-side counter-evidence. The point that holds is no delays, mass production and customer deliveries beginning in 2H26, and a distinction: small-scale commercial validation and large-scale deployment are different stages [13].

That is the whole thing. “Production” and “broad availability” are not the same word. Between the first switch reaching a select partner and the standard form factor going into clusters of tens of thousands of GPUs sits a packaging-capacity ramp. What SemiAnalysis pointed at was most likely the speed of that ramp. That is not “CPO dies.” That is “the volume ceiling opens slower than expected.”

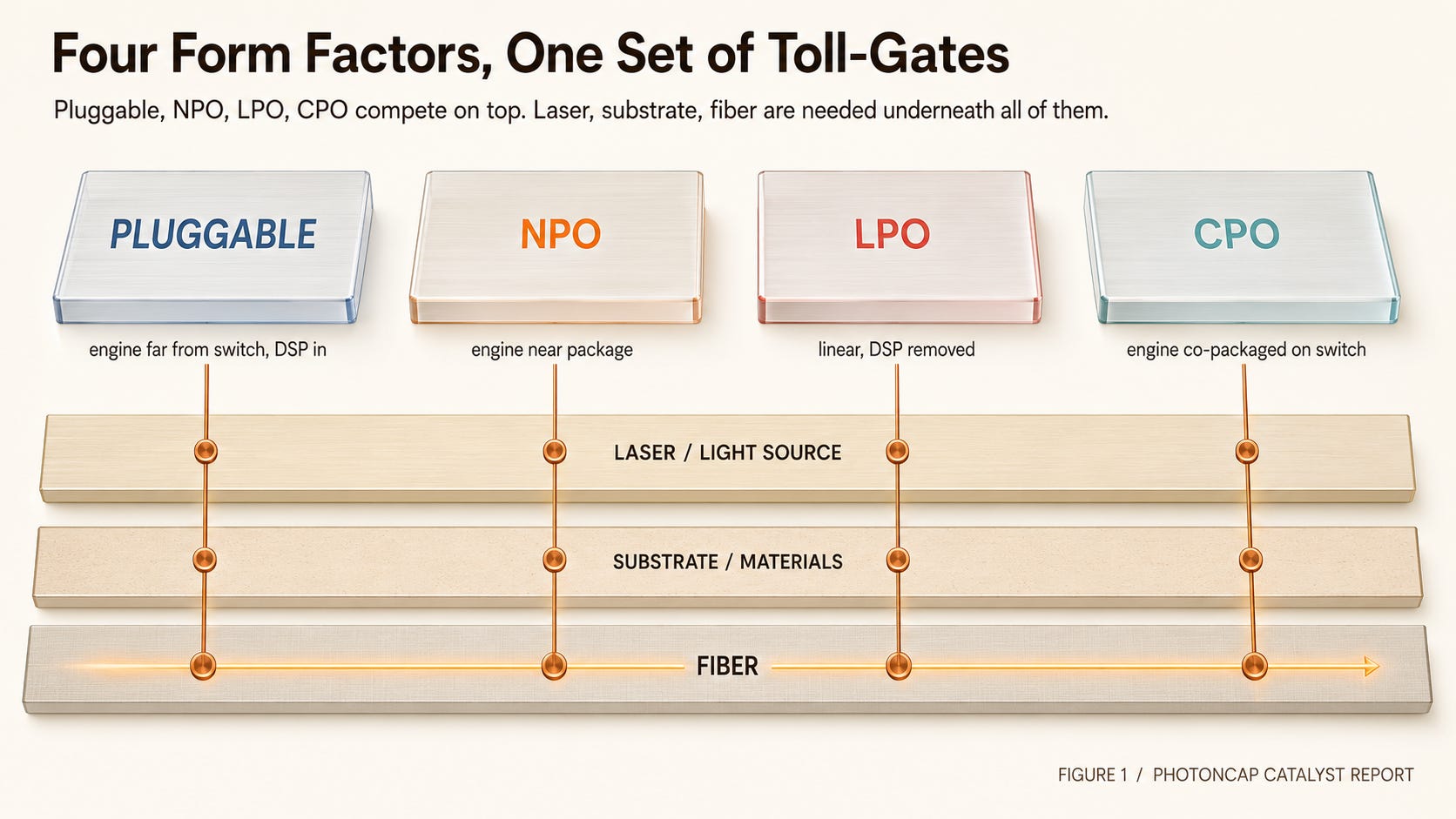

Many Form Factors, One Set of Toll-Gates

The optical interconnect in an AI data center is not one shape. Four broadly compete. Pluggable transceivers (today’s workhorse), NPO (near-package optics), LPO (linear pluggable optics), and CPO (co-packaged optics). They split on how far from the switch chip the optical engine sits, and on whether a DSP is in or out.

Here is what investors miss. Whichever of the four wins, there is always a laser inside, a substrate inside, and fiber inside. The light source that makes the photons, the fiber that carries them, the substrate and materials that bind chip and optics into one package. These do not sit on top of form factor. They sit underneath it, as shared toll-gates.

[Figure 1: Four form factors, one set of toll-gates. The pluggable / NPO / LPO / CPO spectrum and the common laser, substrate, and fiber layers underneath]

So “if CPO is late, optical stocks die” is a fear that lumps distinct layers together. A CPO delay does not push every optical layer the same direction. Some layers take the hit, and some buy time as pluggable runs longer. The problem is that the market put both in the same basket and sold them together.

That is the range anyone can reconstruct from public material. The real question is separate.

What if the names being sold are not pinned to CPO, and the names being bought are the actual CPO principals? Isn’t this trade pointed the wrong way?

Who holds which toll-gate, why AVGO and Marvell are not a clean hedge, and why NVIDIA’s own capital is the strongest counter-evidence of all. That part is for paying subscribers.

[Paid section: a breakdown of which layers the market mispriced, and which names a CPO delay buys time for. LITE, COHR, Sivers, Soitec, POET, AVGO, and MRVL on one table, “why it was sold” against “actual exposure.”]