Taiwan GTC (Computex 2026): CPO Just Entered Production, So Why Are Coherent and Lumentum, the Companies It Was Supposed to Kill, Still on the Supplier List?

$NVDA $COHR $LITE $GLW $FN $TSM | Spectrum-X Photonics Goes Production: The CPO Supply Chain

On May 31, 2026 (US press release date, Taiwan GTC Taipei keynote), NVIDIA called Spectrum-X Ethernet Photonics “now in production.” It is the world’s first co-packaged optics (CPO) Ethernet switch built on 200G SerDes, with CoreWeave, Lambda, and Oracle Cloud Infrastructure among the first adopters. One caveat up front: “now in production” marks the start of a manufacturing ramp, while broad availability is guided to the second half of 2026, so the two should be read separately. CPO pulls optical I/O right next to the switch silicon, so the market’s first reaction was pluggable transceiver cannibalization. Yet on the 11-partner supply chain list NVIDIA disclosed back in 2025, the very companies that build pluggables (Coherent, Lumentum) show up again as CPO suppliers. This piece looks at who actually builds what behind that one-line “production” claim, and how cannibalization and upside can happen inside the same company at once.

Contents

Intro: NVIDIA Put Money Into the Companies It Was Supposed to Kill

Where CPO Actually Landed: Scale-Out, Not Scale-Up

The Three Physics Problems That Blocked Production

The Question to Ask After “Production”

Splitting the 11 Suppliers by Role

Cannibalization vs Content, Inside One Company

Fiber: The Second Set of Numbers CPO Creates

Where the Real Chokepoint Is

Scenarios, Monitoring Points, Close

References & Sources

1. Intro: NVIDIA Put Money Into the Companies It Was Supposed to Kill

The market read CPO as the death of the pluggable transceiver. NVIDIA, instead, put money into the suppliers that were supposedly dying. In 2026 it invested $2B each into Coherent and Lumentum on March 2 [9], $2B into Marvell at the end of March [10], and tied Corning in directly in May [6]. The stranger part: on the Spectrum-X Ethernet Photonics supply chain list NVIDIA disclosed back in 2025, Coherent and Lumentum are already there. The supposed casualties are also suppliers to the new platform.

That contradiction is where this piece starts. CPO removes the pluggable form factor, not the optical content. It unbundles the economics that used to sit inside one transceiver module into three layers: the laser that makes the light, the fiber and connectors that move it, and the packaging that bonds the electronic and photonic chips. So the question for an investor is not “how much pluggable does CPO kill,” but where the dollars from the shrinking transceiver socket get captured again. I broke down which layer each of the four investments targeted in a prior piece, “Coherent, Lumentum, Marvell, and Now Corning”.

Now the event itself. On May 31, 2026 (US press release date), at the Taiwan GTC Taipei keynote, NVIDIA said the Vera Rubin platform had entered full production, and inside that was one line. Spectrum-X Ethernet Photonics is “now in production,” into its manufacturing ramp, with CoreWeave, Lambda, and Oracle Cloud Infrastructure among the first adopters [1][2]. The Ethernet version that was “expected in 2026” at GTC in March 2025 [3] has flipped to “in production.”

Takeaway: what changed is one word (”expected” to “in production”), but while the market asks “who dies,” NVIDIA had already lined up “who gets paid again in a different layer.”

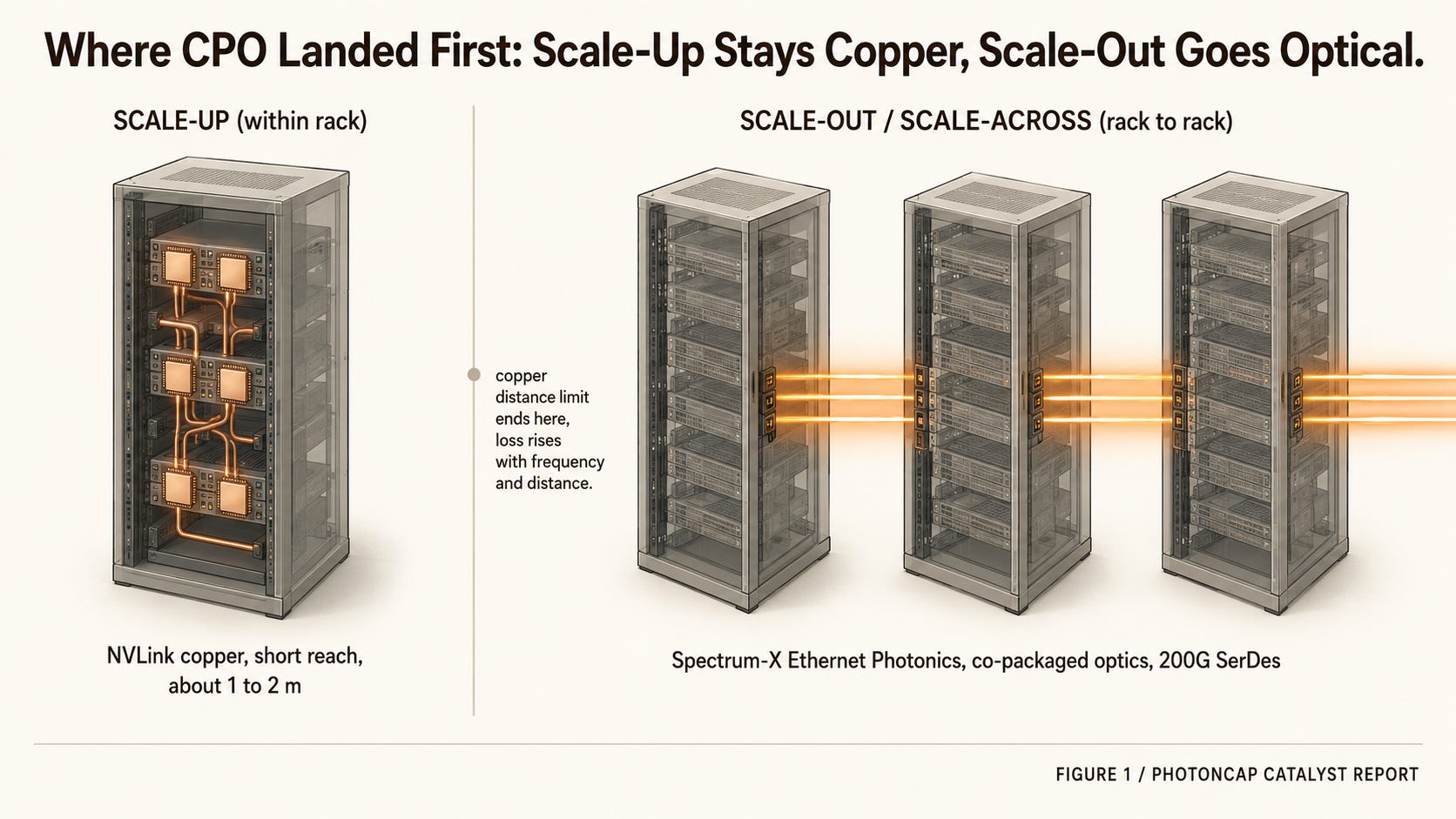

2. Where CPO Actually Landed: Scale-Out, Not Scale-Up

Read CPO as nothing more than “swap all copper for optics” and the market’s read-through goes wrong. The first thing to pin down is exactly which links this product replaced.

Connections inside an AI rack come in two kinds: scale-up, which binds GPUs together inside a rack, and scale-out plus scale-across, which link rack to rack and site to site. In the Vera Rubin NVL72, scale-up runs on the sixth-generation NVLink Switch and stays copper [2], while the Spectrum-X Ethernet Photonics that just entered production handles the scale-out and scale-across Ethernet fabric alongside the ConnectX-9 SuperNIC [2]. CPO did not strip copper out of the rack interior. It went into the fabric leaving the rack first.

Why can scale-up stay copper while scale-out has to go optical? It comes down to distance and frequency. Copper loss climbs steeply as signal frequency rises. As lane rates climb toward 200G SerDes, the distance over which copper can still recover the signal shrinks. Inside a rack, GPU to GPU (scale-up) is typically within 1 to 2 meters, so copper still closes the link at these rates, and it beats optics on power, latency, and cost. But rack to rack and site to site (scale-out and scale-across) stretch from several meters to tens or hundreds of meters, and at those distances copper falls into a loss regime that equalization cannot rescue. Fiber, by contrast, is a medium whose loss is measured per kilometer, so it carries long distances at low loss. That is why scale-out is forced optical. And as lane rates rise, the distance copper can hold shrinks, pushing optics closer to the chip. CPO is where that push lands.

Why this distinction matters: “CPO kills NVLink copper” and “CPO replaces part of the scale-out Ethernet pluggable market” are claims of completely different size. What happened now is the latter. The former has not.

On the spec sheet, each port is 1.6 Tb/s, and depending on configuration the switch spans 102.4 Tb/s (128 ports of 800G) to 409.6 Tb/s (SN6800, 512 ports of 800G or 2,048 ports of 200G) [5][7]. (NVIDIA’s 2025 press release rounded these to 100/400 [3].) The efficiency figures use different baselines across announcements. The 2025 platform launch cited, versus traditional designs, 3.5x energy savings, 63x signal integrity, 4x fewer lasers, 10x resiliency, and 1.3x deployment [3], while the Spectrum-X Ethernet Photonics technical material cites, versus pluggables, 5x power per port, 5x AI uptime, and 10x resiliency [7]. Both are company figures with different baselines, and neither is independently verified.

[Figure 1: Where CPO landed. Scale-up (copper NVLink) vs scale-out/across (CPO Ethernet) diagram]

Takeaway: CPO did not “rip all copper out of the rack.” It “went into the fabric leaving the rack first.” That difference sets the boundary of cannibalization.

3. The Three Physics Problems That Blocked Production

CPO sat at “maybe” for years not because the idea was hard, but because three physics problems blocked production. That these three reached a level where they integrate within a production configuration is what “now in production” actually means. Yield, per-customer qualification, and long-term reliability are separate items to keep watching.

First, where to make the light. Silicon passes light well but cannot generate it, so the laser source sits outside the package (External Laser Source, ELS) and its light is fed into the silicon photonics engine. Put the laser right next to the chip and heat destroys it. Assembling, optically aligning, and testing this ELS is the first hard problem [4].

Second, how to couple that light in without loss. Light from the external laser has to be coupled into the silicon photonics engine while preserving polarization, and the processed signal has to exit through front-panel fiber. This is a precision problem for optical connectors and fiber assemblies [4].

Third, how to stack the electronic and photonic chips in one package. Long electrical paths cost efficiency, so the electronic IC (EIC) has to sit directly on top of the photonic IC (PIC) in 3D. That is what TSMC’s COUPE process does [4][5].

None of the three is the kind one company solves alone. The laser maker, the fiber-coupling specialist, and the 3D-stacking foundry are each different. That the layers have different owners is the starting point for the investment view.

Takeaway: CPO production = external laser (ELS) + fiber coupling + 3D packaging, with all three layers meshing together in a production configuration. Different owners per layer is where the investment view begins.

4. The Question to Ask After “Production”

Up to here is the range anyone can see by following the press release and the technical blog. What the public release tells you is that the switch exists. The investable part is next: splitting the 11 disclosed suppliers by role.

The question narrows to this. Among these 11, who gains new content and who gives up a socket? Do Coherent and Lumentum gain more from ELS lasers than they lose from pluggables, or less? Why does Corning have its own separate arithmetic? And which single spot, if it falls out, stops the line?

Production is a start signal, not a destination. Between the announcement, volume shipment, and a meaningful attach rate sit more gates of yield and qualification, and at each gate a different layer books revenue first. Below: the 11-supplier split, the net of cannibalization and upside, the chokepoint, and scenarios.

Pricing update — effective June 3, 2026 (end soon!!)

PhotonCap started with a simple bet: that there’s demand for silicon photonics research that goes deeper than press releases and earnings recaps.

That bet has paid off.

PhotonCap has grown to well over a thousand paid subscribers and ranks #23 on the Substack Top Bestseller list. I’m grateful that this publication is now trusted not only by individual investors, but by institutional investors, hedge funds, and sell-side analysts — as well as fellow research publications including Citrini Research, FundaAI, ChipStrat, Vik’s Newsletter, and Jason’s Chip, who subscribe as paid members.

New pricing — effective June 3:

Monthly: $50/month (currently $30)

Annual: $500/year (currently $300)

Already a paid subscriber? Your rate is locked in permanently. Nothing changes for you.

If you’ve been considering subscribing, now is the time. Lock in the current rate before June 3.

Content offerings, format, and frequency may evolve over time as PhotonCap grows.

— PhotonCap