Down 40%, 40%, and 14% in Six Weeks: What the Ciena, Nokia, and Cisco Correction Priced In

$CIEN $NOK $CSCO | Scale-Across Incumbents Comparison

Abstract

Between June 2 and June 4, 2026, three stocks peaked within three days of one another. Ciena and Cisco closed at all-time highs, and Nokia printed a 52-week high. By July 17, Ciena had corrected 40.3% from its peak close, Nokia 39.9%, and Cisco 13.9%. All three are the classic incumbents of the scale-across coherent layer, the optics that link one datacenter to another. And the split is telling: the two companies with the highest optical exposure fell roughly 40% in lockstep, while Cisco, with the lowest exposure, gave back only 14%. This piece compares what each company actually holds, what the correction priced in, and when and where the numbers that will judge this correction arrive. The first gate is Nokia’s Q2 report on July 23. Tickers: $CIEN $NOK $CSCO.

Contents

Intro: the ones that rose most fell most

The layer these three stand on: a recap of the two optical fights

What each of the three incumbents holds

Nokia: four DSPs and two very different checks

Cisco: the dot-com relic whose coherent business just had a record quarter

Ciena: a correction at a supply-constrained company

Scenarios and three gates

1. Intro: The Ones That Rose Most Fell Most

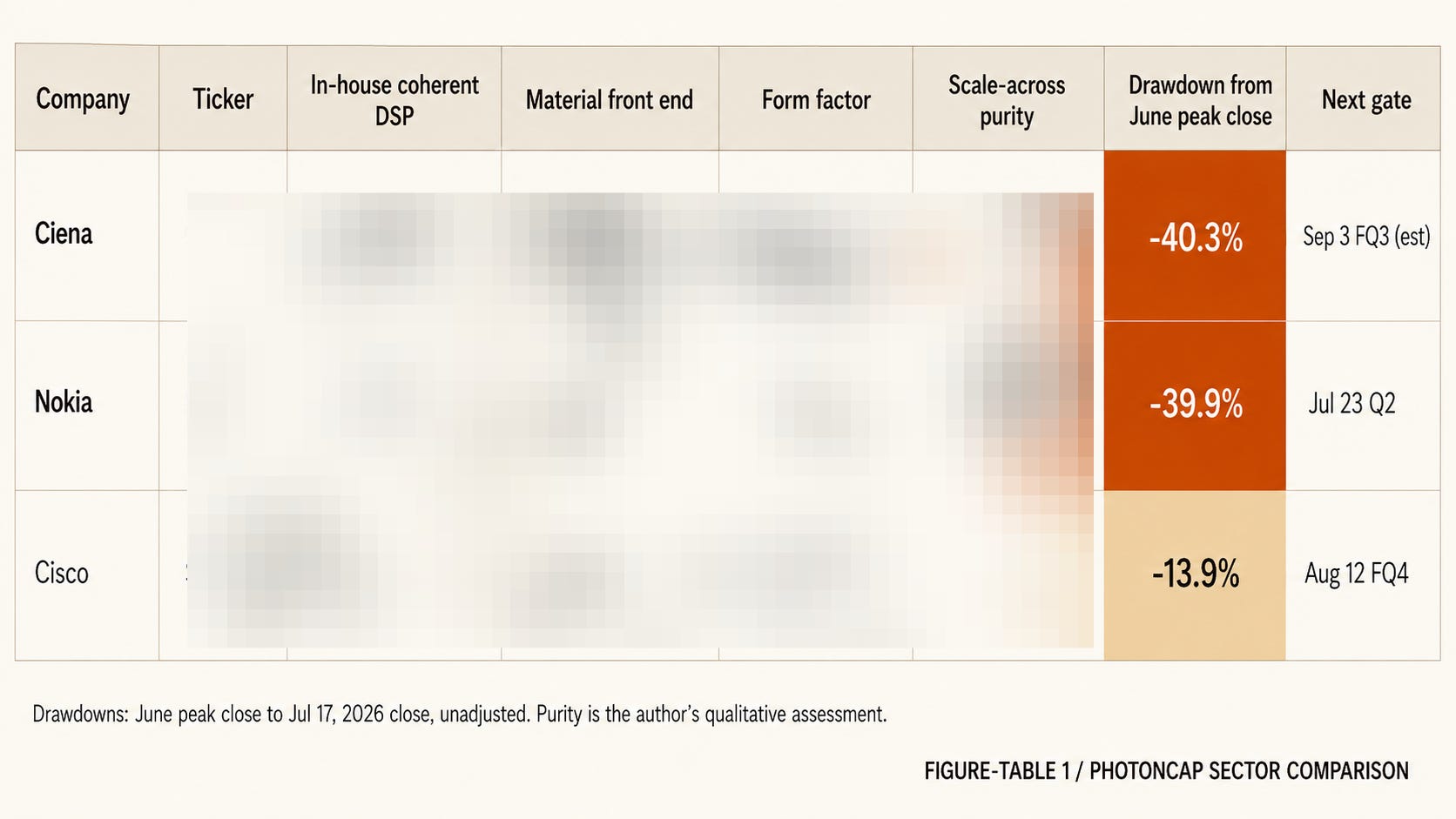

Here are the trailing 1-year returns (as of the 2026-07-15 close).

Ciena ($CIEN) +406.6%. Nokia ($NOK) +141.0%. Cisco ($CSCO) +68.1%.

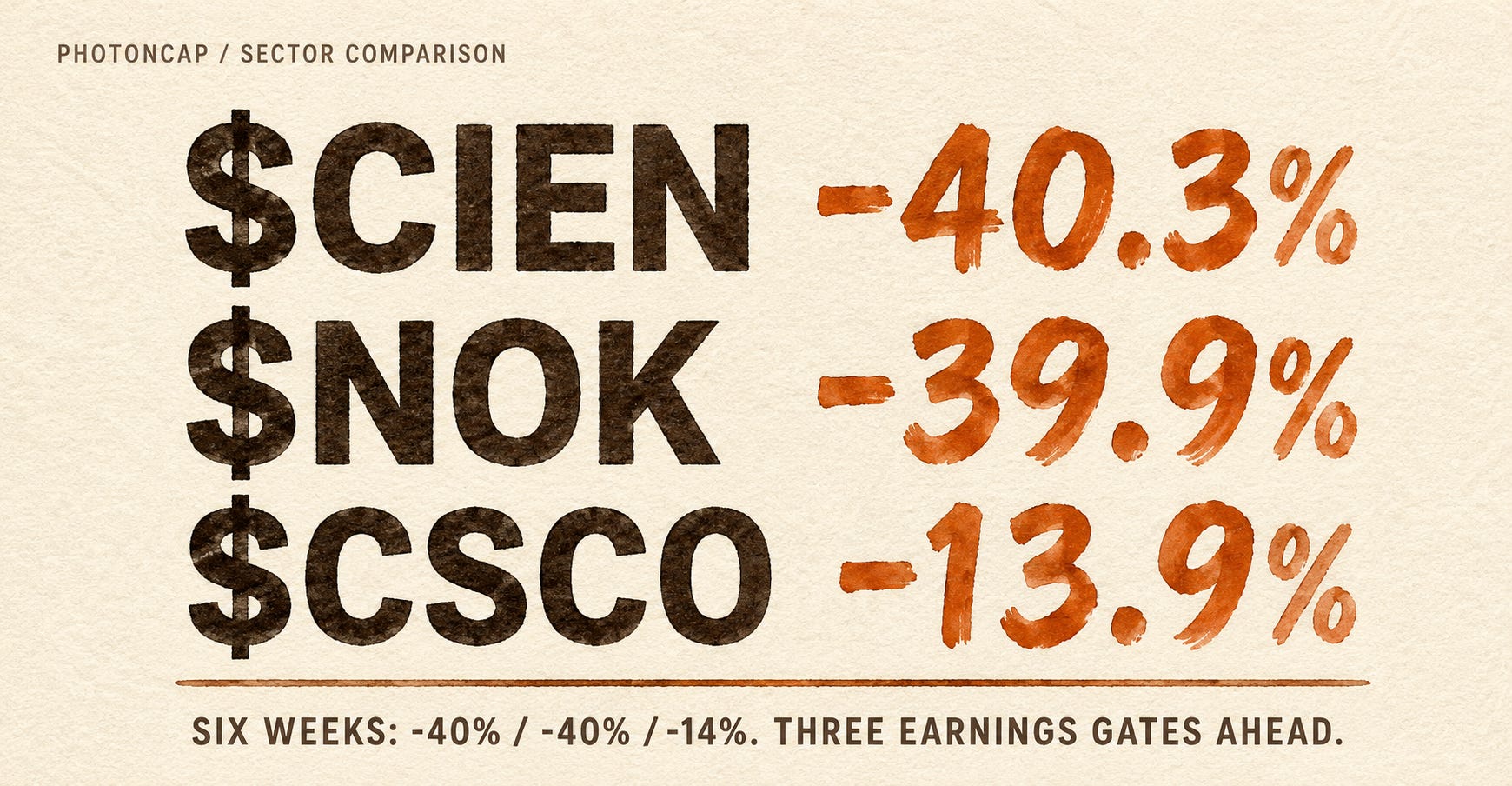

And here are the drawdowns from each June peak close to the July 17 close (unadjusted closing prices).

Ciena -40.3% ($627.00 → $374.41). Nokia -39.9% ($16.85 → $10.12). Cisco -13.9% ($130.00 → $111.94).

Start with the peak dates. On a closing basis, Ciena and Nokia topped on June 2 and Cisco on June 4, while Nokia’s intraday 52-week high of $17.45 printed on June 3. Three stocks peaked within three days of one another, and over the following six weeks they split into two groups. Ciena and Nokia, the two names with the heaviest optical exposure, fell roughly 40% by almost identical amounts. Cisco, where optics is one business among several, gave back only 14%. It looks like coincidence. It is not. There is a reason for this split, and that reason is the subject of this piece.

One scene captures what kind of correction this was. On June 4, Ciena reported quarterly revenue up 40%, adjusted EPS nearly quadrupled, and a raised full-year guide. The print beat consensus. There was no guidance cut and no ugly headline. The stock still fell 13.7% that day ($620.37 → $535.63), then dropped another 8.9% the next day, for a two-day cumulative decline of more than 21%. The results were not the problem. Even a raised guide could not fill the price and the expectations that had been stacked in front of it. And the July leg down that followed was not a Ciena-specific event; it came with a repricing across the entire AI optics complex.

So the question becomes this. Did the correction break the scale-across demand thesis, or had the price simply run ahead of the thesis? To answer that, we first need to pin down exactly which layer these three companies stand on.

Summary: three peaks within three days in early June, then a six-week correction. High-optical-exposure Ciena and Nokia both fell about 40%, while low-exposure Cisco fell only 14%. The trigger was not deteriorating results.

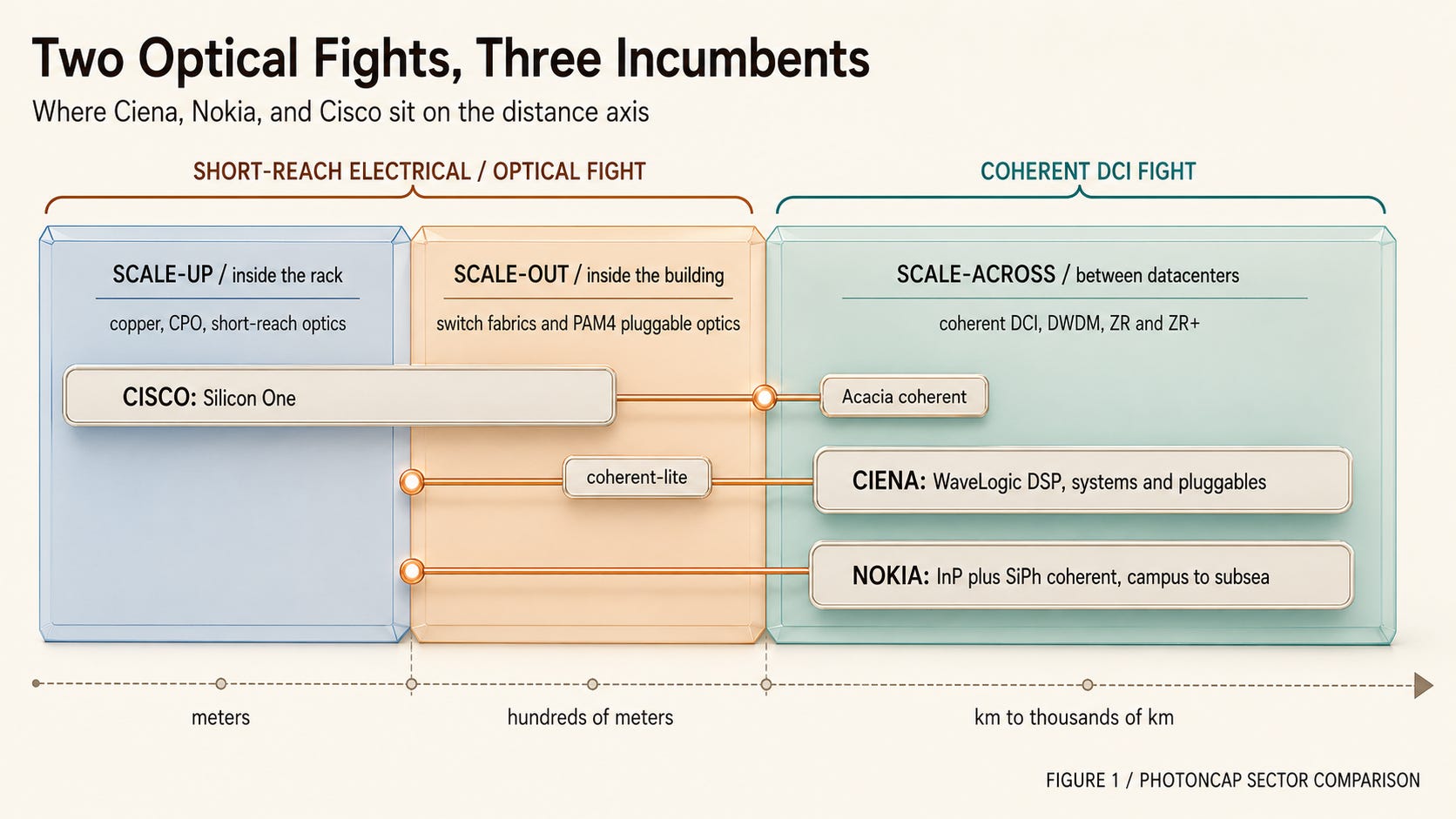

2. The Layer These Three Stand On: A Recap of the Two Optical Fights

In our last piece, we laid out why there is not one optical fight inside an AI datacenter but two. Inside the rack (scale-up) it is a CPO fight; between datacenters (scale-across) it is a coherent DCI fight. The distance-based layer split itself was first drawn in our April NVIDIA-Marvell piece, and if terms like CPO, LPO, and NPO are new to you, the optical architecture primer is a good place to start. Meta’s blueprint linking campuses at distances up to 2,000 km (a SemiAnalysis model estimate) was the first concrete evidence that demand for the second fight is opening at gigawatt scale.

DSP, LPO, NPO, CPO: The Four Optical Architectures and the Light Source Beneath Them All

On June 9, an institutional-only SemiAnalysis note lit the fuse, and optics names dropped together. AAOI fell 14%, COHR 11%, LITE 8% [1][2]. The market’s logic was simple: “CPO volume slips to 2028 to 2029, so photonics is over.” Yet the very next day the same names bounced (AAOI +7%, LITE +5%, COHR +2%) [3], and in the same week NTT, SK, and Chunghwa Telecom launched a new $500M fund pointed at optical communications and light sources [4][5]. This piece lays out the four optical architectures, DSP, LPO, NPO, and CPO, in a way a non-specialist can absorb in one read, then maps where Lumentum, Coherent, AAOI, and Sivers actually sit on that ladder. The thesis is one sentence.

The hardware market that receives that demand is shifting in ways the numbers confirm. Per Cignal AI, standalone coherent WDM pluggable revenue grew 37% to reach $1.8B in 2025 (Cignal AI rounds this to a $2B market in its headline), a category that has compounded at 71% annually since 2021. WDM pluggables are projected to exceed $5B by 2029 at a 30% CAGR, the single largest growth driver in optical hardware, and the near-term catalyst is the volume deployment of 800ZRx modules into AI-driven scale-across networks.[1] (In this piece, 800ZRx is used as the market-research umbrella covering the OIF-standard 800ZR and vendor-specific 800ZR+ families.) Scale-across architectures demand 5x to 20x the bandwidth of legacy DCI, and North America posted record optical revenue in 2025, growing more than 30% and overtaking China by a wide margin as the largest optical market.[1]

In the last piece we noted that Marvell and Coherent had adopted scale-across as their own official language. That language has now spread to one more company. In its May earnings materials, Cisco classified its new design wins using the phrase “P200 scale-across” directly on its official IR slides.[2] This is no longer an analyst’s frame. It has become the suppliers’ own product taxonomy.

Which brings us to the cast of this piece. Coherent technology is the craft that carrier-backbone equipment makers spent decades refining. Ciena and Nokia (including the Infinera lineage) are direct descendants of that craft, and Cisco joined it in 2021 by acquiring Acacia, a company of that lineage. The three incumbents in the networking sense, Ciena, Nokia, and Cisco, are the cast of this piece.

Summary: scale-across coherent pluggables are a market growing from $1.8B in 2025 to $5B+ by 2029, and the frame has become the suppliers’ own official product taxonomy.

3. What Each of the Three Incumbents Holds

Standing on the same layer does not make them the same company. Each arrived here by a completely different path.

Ciena is the one whose revenue is most directly exposed to the optical network investment cycle. It owns its coherent DSP line, WaveLogic, and fields a lineup that spans both line systems and pluggables: WL6e-based 1.6Tb/s coherent solutions, WaveLogic 5 Nano 400G and WaveLogic 6 Nano 800G coherent pluggables for metro DCI, and 1.6T coherent-lite aimed at campus and inside the datacenter.[3]

Nokia completed the vertical structure of this layer by acquisition. It closed the Infinera deal on February 28, 2025, scaling up its optical networks business, and the company itself framed the acquisition as accelerating growth into datacenters, North America, and webscale customers.[4] What Infinera brought was InP (indium phosphide) PIC technology and fabs, and combined with Nokia’s existing silicon photonics, the result is an optical front-end structure with a foot on both material platforms.

Cisco is defined by the combination of in-house switching and routing silicon alongside coherent DSP and optics under one roof. Silicon One sits in the fights inside the rack and the building (scale-up, scale-out), while Acacia, acquired in 2021, sits in scale-across with its coherent DSP and silicon photonics. So the fact that Cisco’s drawdown is the shallowest of the three is better read not as superior defense, but as scale-across simply being the smallest share of the whole company.

Which brings us back to the observation from the intro. Ranked by purity of scale-across exposure, the order is Ciena, Nokia, Cisco (this purity is the author’s qualitative assessment based on disclosed revenue segments, product mix, and order disclosures, not an accounting measure). Optics is the center of Ciena’s business, one part of Nokia’s group, and one of several businesses at Cisco. And in this correction, the two high-purity names fell roughly 40% side by side while low-purity Cisco stopped at 14%. What the market discounted was not any individual company’s results but scale-across exposure itself. Of course, the attribution is not that simple. Nokia’s +141% in particular carries a meaningful contribution from the AI-RAN and NVIDIA narrative, so part of its -39.9% may be that narrative unwinding rather than optics. Why that distinction matters is something we sort out in the Nokia chapter of the paid section, where we split the two checks apart.

One question deserves a preemptive answer. Why is Marvell ($MRVL), the other headliner of this layer, not in this comparison? Marvell is not a classic equipment maker; it entered this market as the merchant-DSP-and-pluggable insurgent, and PhotonCap has covered it separately several times, including in the last piece. In this article Marvell appears not as a fourth card but as the yardstick against which the three incumbents are measured. Where exactly it becomes the yardstick is confirmed with numbers in the paid section.

Figure 1: Distance-based three-layer map (scale-up / scale-out / scale-across) with the three companies’ product positions overlaid

Everything up to here, though, is a map anyone familiar with the public record could draw. The real question is not the map but the clock. Even with exposure pointing the same way, the numbers each company must prove in this correction are completely different. Nokia has to bridge the gap between a product roadmap that reaches GA in 2027 and its optical growth rate right now. Cisco has to show its coherent business is genuinely growing at triple digits. Ciena has to show how fast a record backlog converts into revenue. And all three already have dates on the calendar for those numbers. The first one lands days after this piece is published.

What is written on each company’s card, and what to check on which date. That is where the real body of this piece begins.