Veeco Q1 2026: Behind the MOCVD Thesis, Spector IBD Was the Real SiPh Lever

$VECO / Q1 2026 earnings call + $250M+ InP laser orders / A dot-com-era IBD franchise reactivates for the AI optical cycle

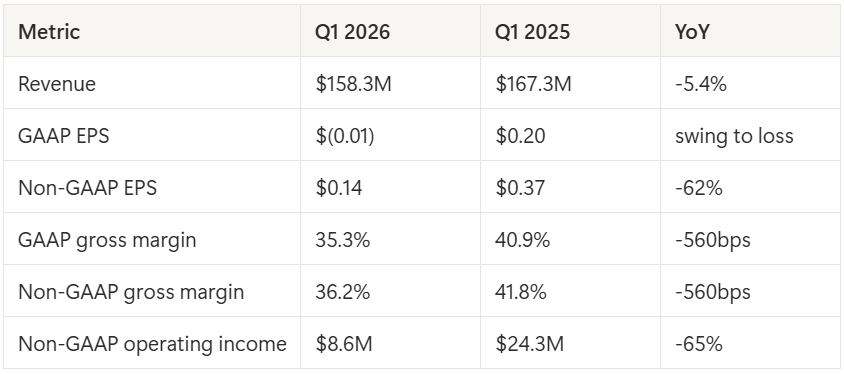

Veeco Q1 2026 revenue was $158.3M, down 5.4% YoY. Non-GAAP EPS of $0.14 landed at the low end of guidance, while non-GAAP gross margin of 36.2% came in below the guided range. The soft P&L was largely tied to one discrete event: BIS export-license requirements blocked shipment of one LSA system to a China customer, creating roughly an $8M revenue headwind. That was the most direct variable behind the gross-margin miss.

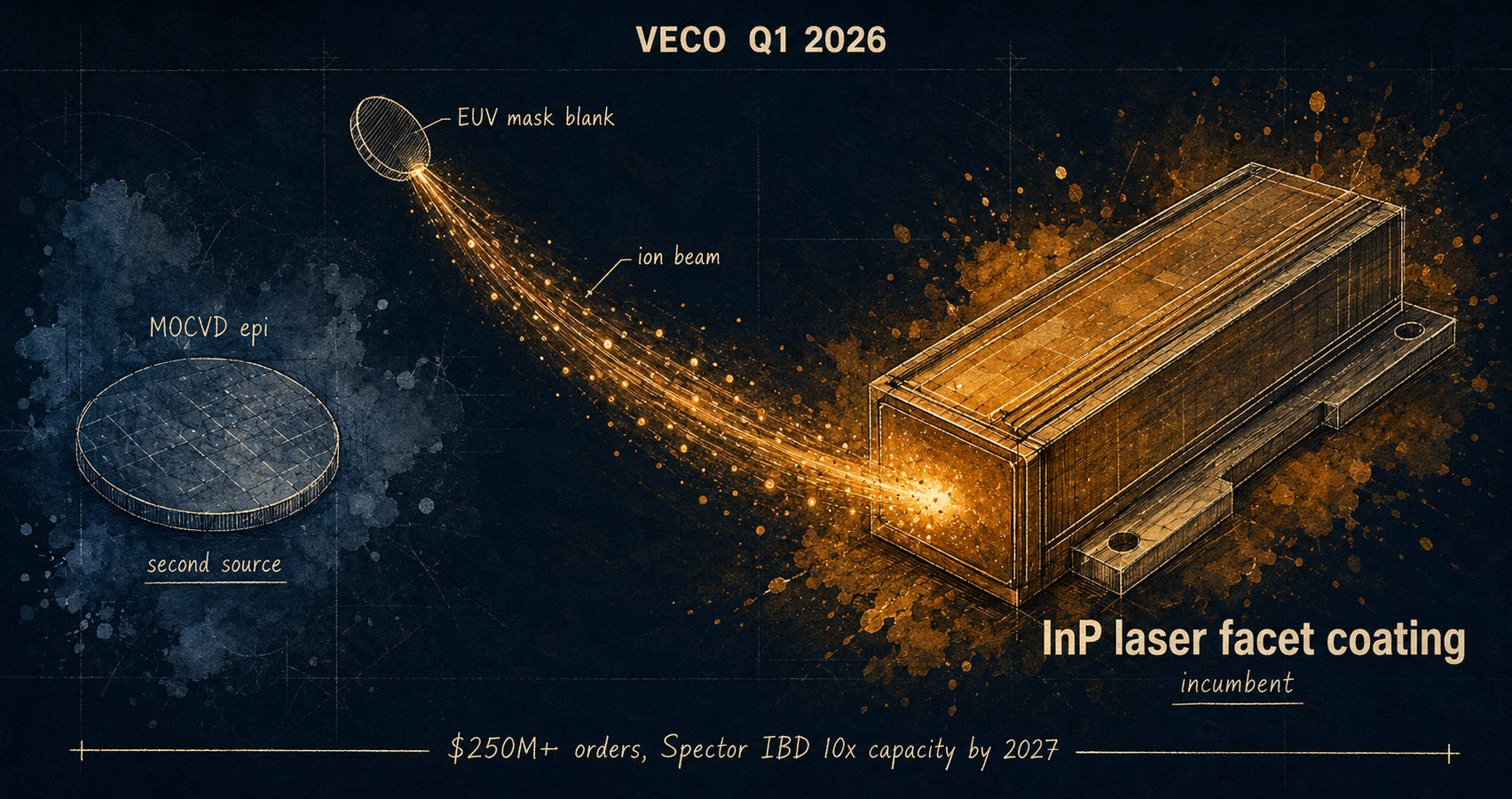

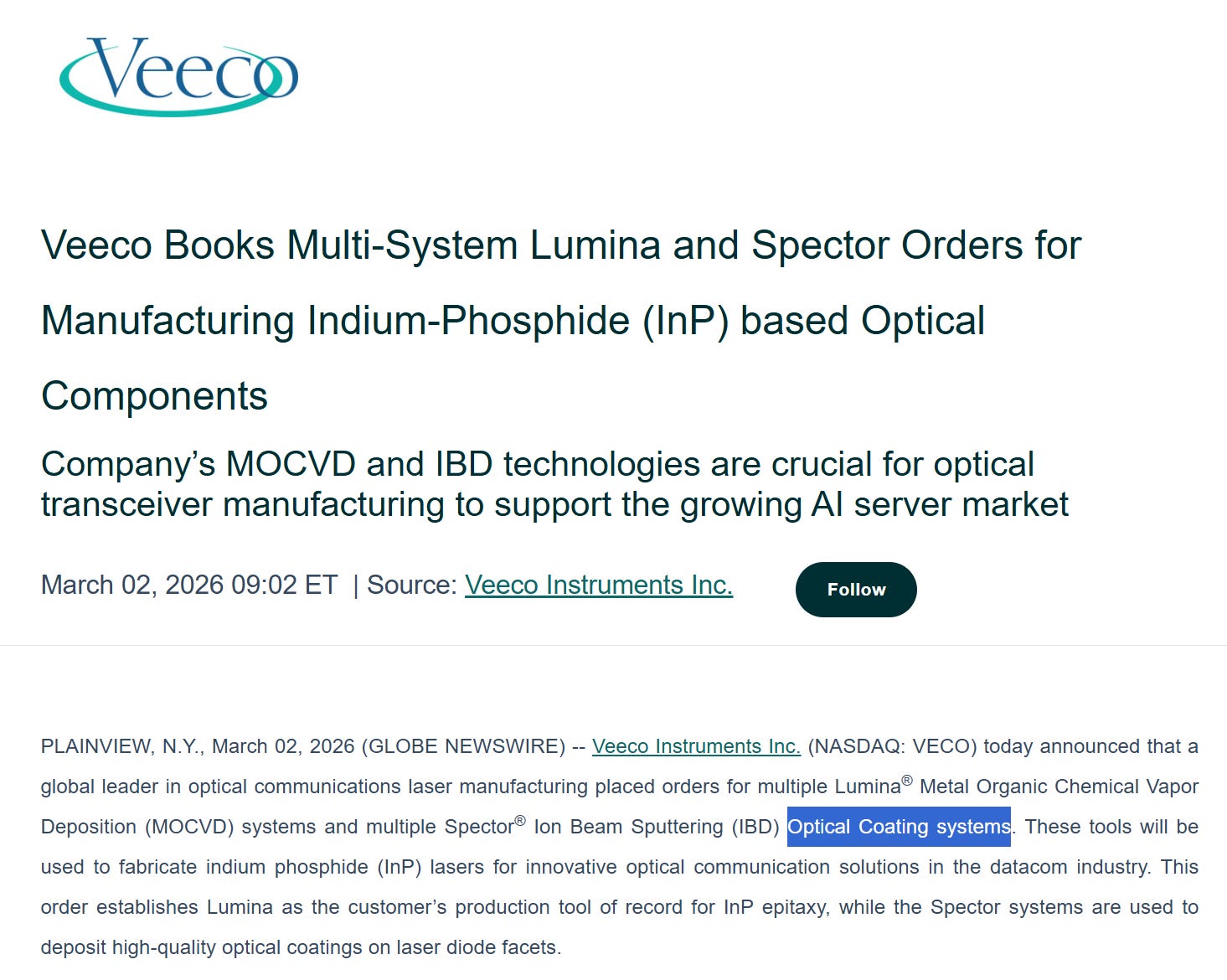

The real headline was elsewhere. On the same day, Veeco separately announced $250M+ in multi-product orders for InP laser manufacturing. In the company’s own wording, “a substantial portion of the orders are for the Spector® IBD” system, used for laser facet coating. The customers are leading manufacturers of 800G and 1.6T optical transceivers for hyperscale data centers.

This piece updates PhotonCap’s six-company piece, where Veeco’s SiPh exposure was framed mainly through MOCVD epitaxy. Q1 made the next layer clearer: the bigger surprise in the order book and the 2027 ramp was not MOCVD, but Spector IBD. The same ion beam technology is already the process tool of record across leading EUV mask-blank manufacturers, and that same asset is now extending into InP laser facet coating.

Ticker referenced: $VECO

Contents

Quarterly Headline

Quarterly data summary (results, segment mix, guidance, B/S, commentary)

The next question

PhotonCap reading: SiPh exposure 3-step + Spector IBD core lever + thesis update

Scenarios + monitoring + close

References & Sources

1. Quarterly Headline

The most direct variable behind Q1’s gross-margin miss was one LSA system blocked from shipment to a China customer ($8M, BIS export license). The real headline was elsewhere: Veeco received $250M+ in multi-product orders for InP laser manufacturing, with a substantial portion in Spector IBD for laser facet coating.

The PhotonCap six-company piece framed Veeco’s SiPh exposure mainly through MOCVD (epitaxy). Q1 data makes the next layer clearer: the bigger surprise in the order book and the 2027 ramp was Spector IBD, one process step downstream from epi. The same ion-beam tooling platform that is already the process tool of record across leading EUV mask-blank manufacturers is now extending into InP laser facet coating.

Scope: $VECO Q1 2026 earnings + the separate $250M+ orders PR + call transcript Q&A + six-company piece thesis update.

2. Quarterly data summary

2.1 Q1 results [1][4]

Non-GAAP EPS $0.14 lands at the low end of guidance. Non-GAAP gross margin 36.2% sits below the guidance range.

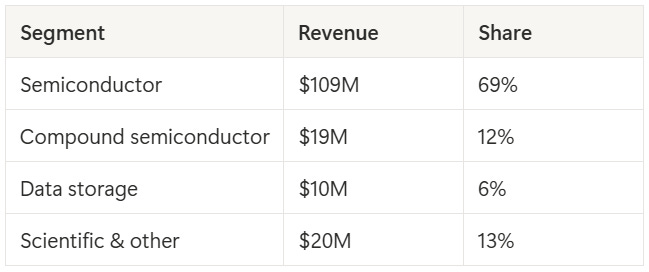

Segment mix (Q1 2026) [4]:

Compound semi at 12% maps directly onto the six-company piece‘s “photonics ~11%” framing. That bucket includes SiPh InP laser, GaN power, microLED, AR/VR, and LEO satellite solar cells.

Gross-margin miss explained [4]: Per CFO John Kiernan, BIS notified Veeco that one LSA system shipment to a specific China customer fab required an export license. That event cost about $8M in top line and was the most direct variable behind the gross-margin miss. Q2 gross margin is guided to 38 to 40%, with recovery expected.

2.2 Guidance [1][4]

Q2 2026: Revenue $170 to $190M, gross margin 38 to 40%, Non-GAAP EPS $0.20 to $0.32. FY 2026 (unchanged): Revenue $740 to $800M, Non-GAAP EPS $1.50 to $1.85.

The CFO and CEO directly named 2026 segment growth on the call: semiconductor mid-teens YoY, compound semi roughly 50% YoY, data storage 2x YoY [4].

Q1 actual plus the Q2 guidance midpoint gives 1H ≈ $338M. Subtract from the FY midpoint of $770M and 2H ≈ $432M, +28% versus 1H. Revenue recognition is weighted heavily into H2.

2.3 Balance sheet shifts (Dec 31, 2025 to Mar 31, 2026) [1][4]

Accounts receivable rose from $111M to $151M (+$40M), and customer deposits within contract liabilities grew $19M to $69M. Inventories ticked from $275M to $282M (+$7M), while cash plus short-term investments was roughly flat at $390M moving to $383M.

AR growth shows the timing of collection on revenue already shipped or recognized. Customer deposits show prepayments not yet recognized. Combined with the $250M+ orders and the H2 weighting embedded in full-year guidance, the picture leans toward revenue recognition concentrated in H2 and into 2027.

2.4 CEO commentary + Q&A core points

SiPh entered the highlight paragraph of the PR, with “particularly strong momentum in silicon photonics” [1].

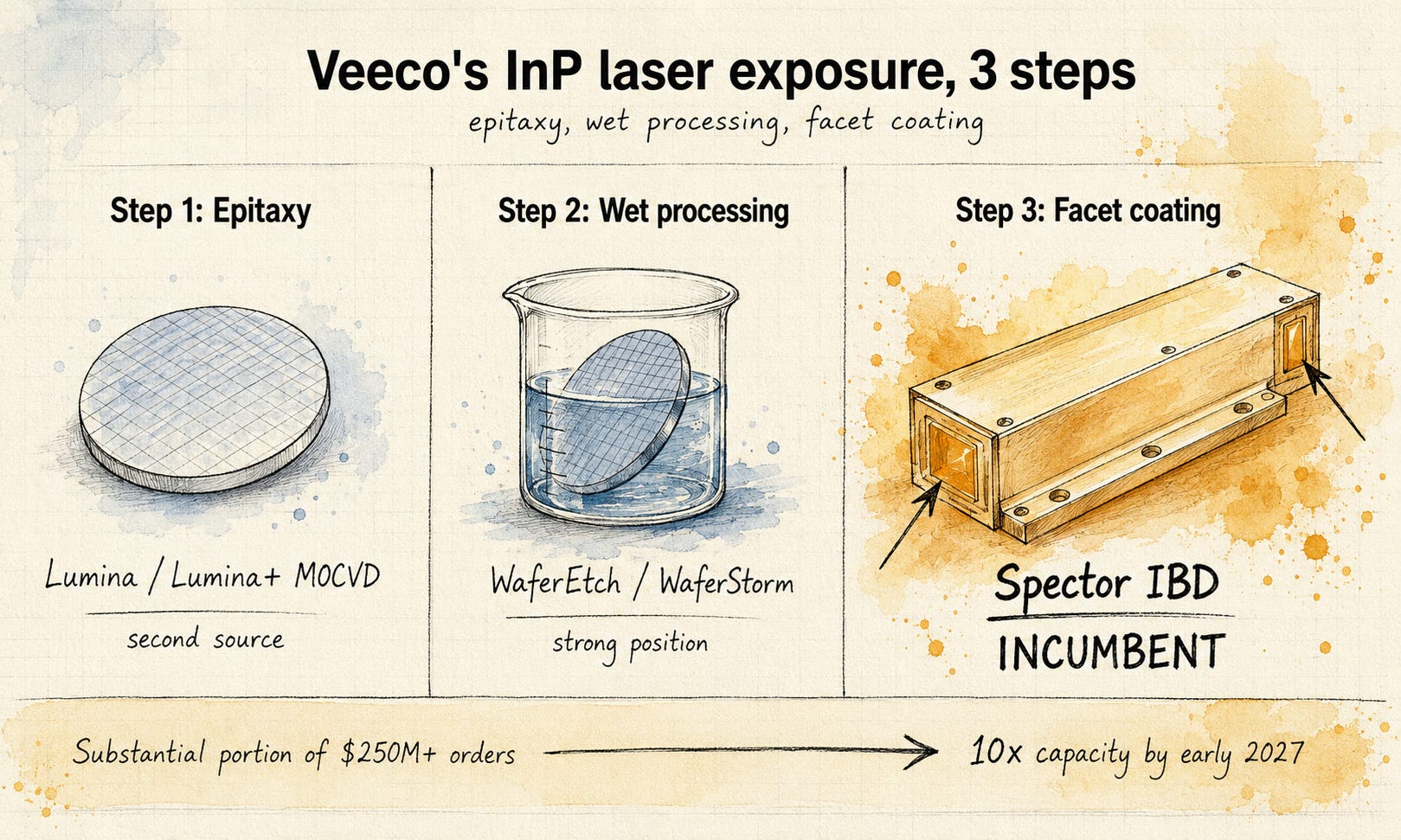

On the same day, Veeco issued a separate PR announcing $250M+ in multi-product orders for InP laser manufacturing [2]. The product mix spans Spector IBD, Lumina MOCVD, and WaferEtch, and per the company’s own wording, “a substantial portion of the orders are for the Spector® IBD”. Customers are leading manufacturers of 800G and 1.6T optical transceivers for hyperscale data centers. Deliveries begin in 2026 and significantly accelerate in 2027 [2]. Per the Q&A, shipments start in Q3 2026 and ramp in Q1 2027 [4].

In the Q&A, Bill Miller explicitly committed to a 10x Spector IBD capacity expansion by early 2027, with potential for another 2x beyond that [4].

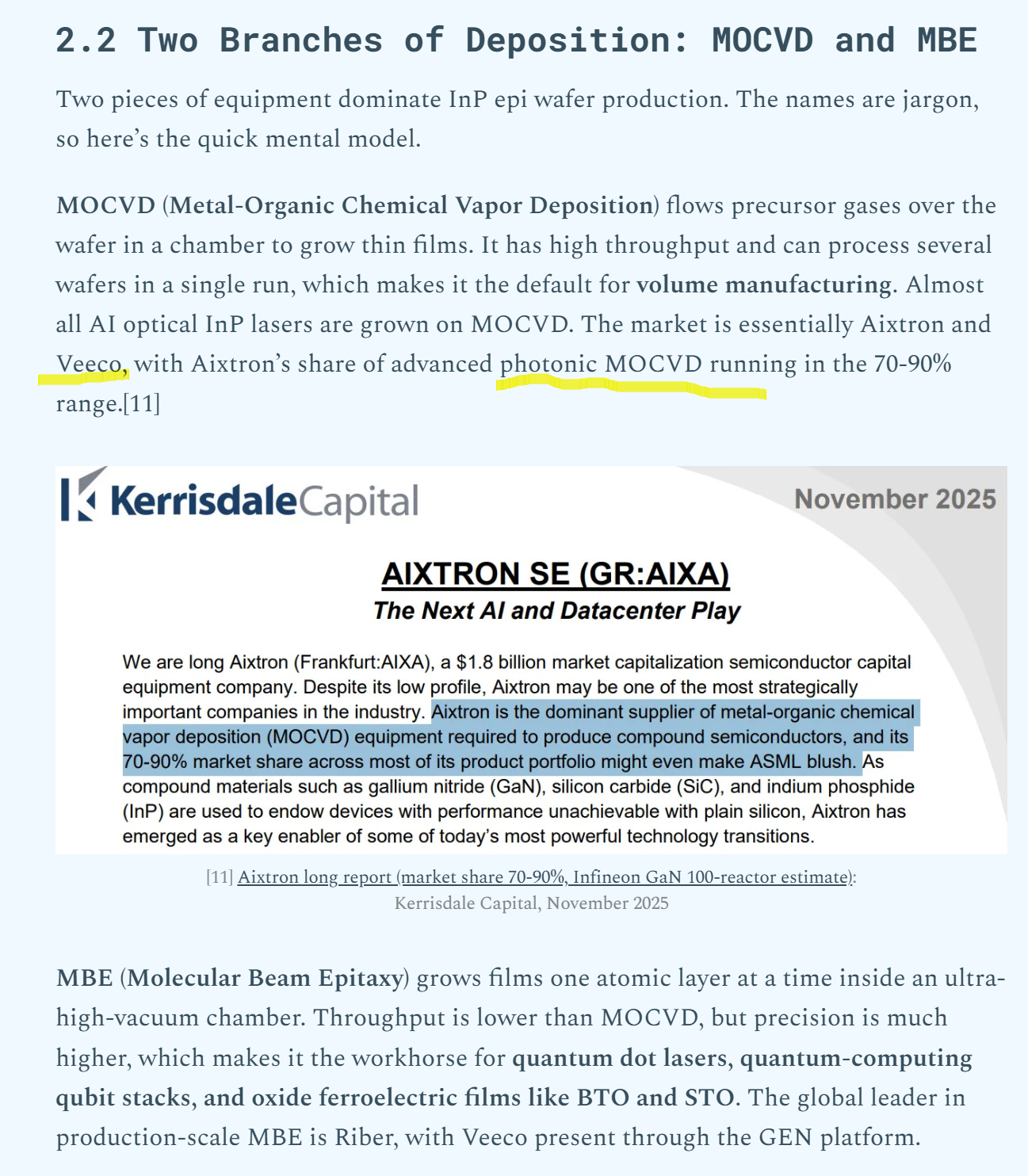

Veeco’s InP laser exposure splits into three process steps. At epitaxy (MOCVD), Aixtron is the incumbent and Veeco runs as a second source. At wet processing (etch / clean), Veeco holds a strong position with multiple leader customers. At laser facet coating, Spector IBD is the incumbent, and that is where the core lever sits [4].

[Figure 1: Veeco’s InP laser 3-step exposure (epi / wet / facet coating)]

Section 2 in one line: the most direct variable behind the Q1 miss is a single event. The actual headline is $250M+ in InP laser orders, with Spector IBD as the substantial portion.

3. The next question

That is what the PR plus call transcript can tell you about the quarter.

The real difference starts here.

The six-company piece framed Veeco’s SiPh exposure through MOCVD epitaxy. Q1 data suggests the larger lever was one process step downstream: InP laser facet coating via Spector IBD, on the same ion-beam tooling platform that is already the process tool of record across leading EUV mask-blank manufacturers.

Behind the paywall, four threads. The semi view covers the Q1 gross-margin miss as a single event and the three streams’ H2 ramp. The photonics view breaks Veeco’s SiPh exposure into 3 process steps, explains why Spector IBD is the core lever, and traces how the previously dormant DWDM-era IBD line reactivates into the AI cycle. The six-company thesis update splits the MOCVD epitaxy line and the IBD facet-coating line, then adds a new thesis line on a single ion-beam tooling platform spanning two AI-cycle markets. The piece closes with Spector IBD ramp scenarios A/B/C and monitoring points.