The microLED Light Source Was Just Avicena. A Quarter Later, Five Listed Tickers Piled In

Where NVIDIA’s Optical Interconnect Lead Went Next: The Quarter Listed Companies Crowded Into microLED Interconnect | Data Center microLED Interconnect Supply Chain Map

Dr. Ashkan Seyedi, who led co-packaged optics interconnect products at NVIDIA, has left NVIDIA to run the optical interconnect business line at ams OSRAM [1].

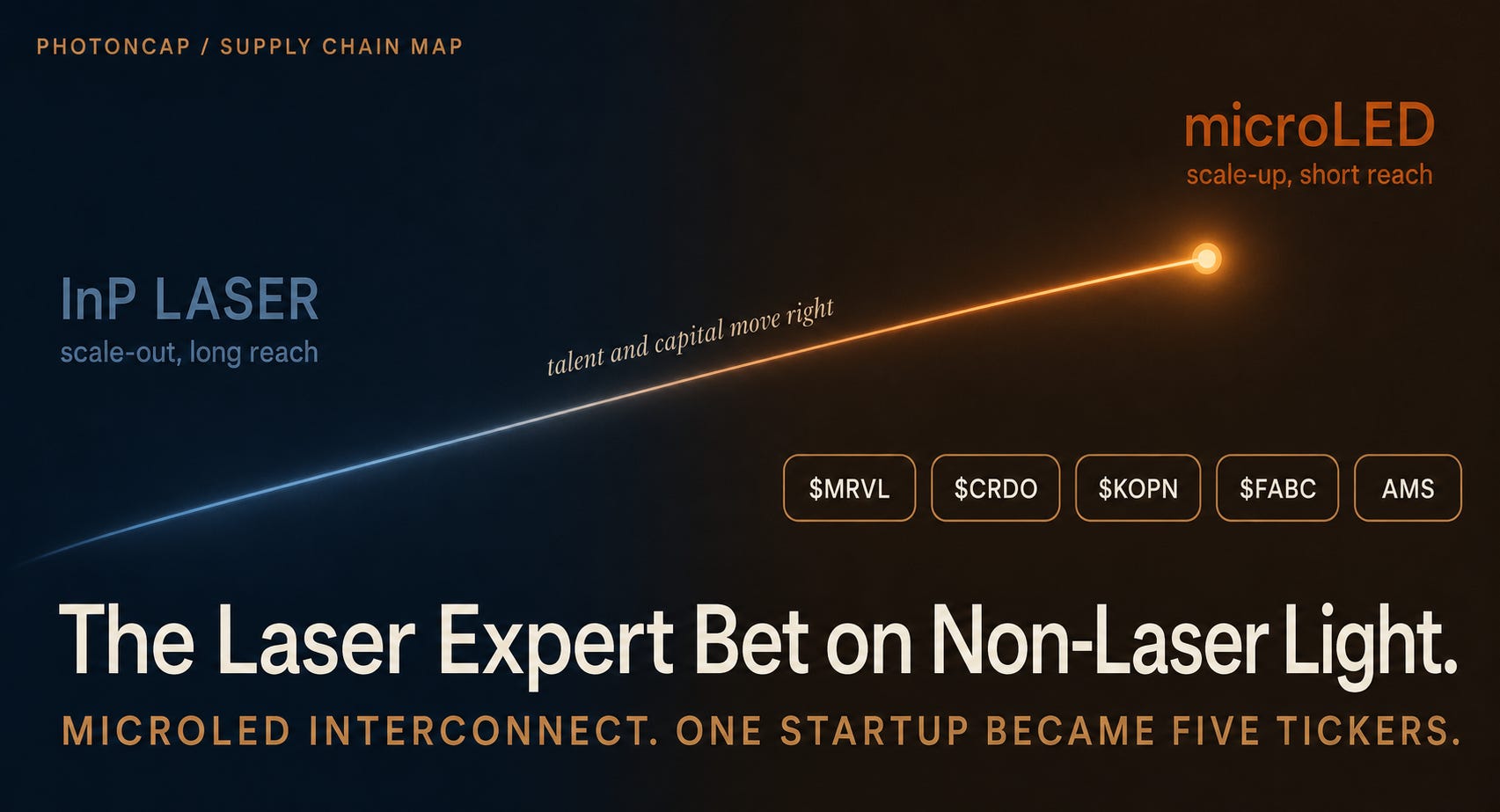

The place he chose is not a company that builds faster lasers. It is the lighting conglomerate that, after the February 2024 cancellation of a cornerstone project widely reported to be Apple, booked a non-cash impairment of EUR 600 to 900 million and stepped back from microLED displays [1][2]. This hire is not a one-off event. It is the clearest single frame of a wave over the past quarter in which listed names attached themselves to microLED-based optical interconnect through different routes. Three weeks ago I wrote that this seat was “effectively just Avicena,” and that sentence is now wrong. This piece maps the whole wave, then separates out the two-front fight in which Marvell and Credo hedge across microLED and silicon photonics, and the volume-manufacturing wildcard that is OSRAM. Related tickers: $MRVL, $CRDO, $KOPN, $FABC, ams OSRAM (SIX: AMS).

Contents

Intro: The Person Who Knows Lasers Best Walked Toward microLED

Why microLED Got Crowded in a Single Quarter

What Is Public and What Is Still Open

The Full microLED Datacom Map: Six Routes

The Real Fight: Marvell vs Credo, and the OSRAM Variable

Different Seats Inside the Same microLED

Valuation: How Do You Buy a Field With No Pure Play

Scenarios and Monitoring

PhotonCap’s View

References and Sources

1. Intro: The Person Who Knows Lasers Best Walked Toward microLED

There is a person who built the optical products that connect GPUs at NVIDIA. M. Ashkan Seyedi, who since 2021 led co-packaged optics and pluggable interconnect products [1]. From the center of demand, he watched the productization of laser-based optical communication more closely than almost anyone.

He left NVIDIA. And the place he staked his career on was neither an InP EML laser house nor the CW laser camp. It was a lighting company, ams OSRAM, that in February 2024 was told by a cornerstone customer widely reported to be Apple that the project was cancelled, booked a non-cash impairment of EUR 600 to 900 million, and then stepped away from microLED displays [1][2]. The seat he took runs a business line chasing short-reach scale-up with GaN microLED and VCSEL.

The person who understands lasers best walked toward a light that is not a laser. (To be precise, ams OSRAM holds both microLED and VCSEL, and a VCSEL is a laser. But what makes this hire a signal is the non-laser source, the microLED.)

Let me first lay out why this carries weight. The market reads a move like this as an expensive signal. More honestly than any single paper or demo number, where talent flows across material systems tells you where the roadmap is heading. When someone who was drawing co-packaged optics roadmaps at the center of demand moves toward microLED, it means that seat has become a serious candidate [1].

Here I need to correct one sentence from my last piece. Three weeks ago I described the microLED light-source camp as “effectively just Avicena, no listed pure play” (Data Center Light Source Map). That sentence is wrong as of today. More precisely, it was already wrong at the time I wrote it. Seyedi’s hire only exposed the gap. He was not alone.

The AI Light Source War Is Not a Speed Race: InP, VCSEL, and μLED Are Buying Different Distances

When PicoJool unveiled its 200G VCSEL and 32x50G μVCSEL on June 15, 2026, a 30-year-old technology landed back on the table as an AI data center light source candidate [1][3]. Around the same window, Avicena, back in the spotlight before and after the PicoJool news, was pushing a non-laser GaN μLED link, driving Tx energy from 200fJ/bit in September 2025 down to 80fJ/bit in November 2025 [4][8]. Data center light sources are now splitting into three material systems and structures: InP edge-emitting laser, GaAs VCSEL, and GaN μLED. But the question the market asks, “who builds the faster laser,” is not the real one. The real axis is which light source the reach, lane count, and serialization cost actually call for. This piece lays out the physics of the three, then uses two axes, “fast and narrow” and “slow and wide,” to map which source takes which seat and which companies already sit there. Related tickers: $AAOI, $LITE, $COHR, $SIVEF, $ALMU, $AVGO.

Takeaway: microLED optical interconnect is not the story of a single startup. In one quarter, several listed names attached themselves to the field. Seyedi’s move is the face of that field, not the whole of it.

2. Why microLED Got Crowded in a Single Quarter

To understand the crowding, look at the seat itself. As GPU-to-GPU bandwidth in AI data centers climbs from 800G to 1.6T and 3.2T, the connection is moving from electrical to optical. But that “light” is not one thing. Scale-out has to travel far on few fibers, so the InP laser holds; scale-up runs short distances where power and latency matter more, so VCSEL and microLED open up. In my last piece I split this along two axes, “fast and narrow” and “slow and wide.”

The reason microLED holds a weapon in slow-and-wide comes down to one line of physics. Unlike a laser, an LED has no threshold current. It can switch on and off even at very small currents, and it can send the slow on-chip signal (a few Gb/s) straight out across hundreds of parallel lanes without high-speed serialization. That removes a large share of the power burned by high-speed serialization and compensation circuitry, which opens room for energy per bit to flip at short reach. Of course driver, TIA, packaging, and redundancy overhead remain. The point is not that a laser cannot do this. It is that in this narrow seat, threshold-free light has the edge.

The problem is that as soon as this seat opened, companies that know how to make threshold-free light walked in all at once through different back doors. A company that did display microLED, a company that did automotive-lighting microLED, and a company that sold connectivity silicon all began chasing the same seat.

ams OSRAM is the most dramatic of these. OSRAM is not a company doing microLED for the first time. The opposite is true. It was one of the West’s leading microLED makers, having built a large 8-inch microLED epiwafer fab in Kulim, Malaysia, to supply a cornerstone customer widely reported to be for the Apple Watch [2]. That customer cancelled the project in February 2024 (the company never officially confirmed the customer’s name; Apple comes from industry reporting and analysis), and OSRAM booked a non-cash impairment of EUR 600 to 900 million, retreated from microLED displays, and narrowed its microLED work to an automotive forward-lighting (EVIYOS) base [2]. What is happening now is not “starting microLED.” It is that part of the microLED manufacturing experience and assets OSRAM accumulated is being reinterpreted toward data center interconnect. In its Q1 2026 results, OSRAM disclosed a development agreement with a leading AI data center infrastructure partner to commercialize a “slow and wide” micro-emitter-array optical interconnect, and it has not yet named that partner [3].

One precise point. Display microLED and a datacom emitter are different devices, even on the same GaN. A display pixel is static, while a datacom emitter switches on and off at a few Gb/s. The manufacturing base carries over, but the high-speed datacom device design skill is an area that has to be filled fresh, which is why seating Seyedi, who understands co-packaged optics, reads as the natural move [1].

Takeaway: The seat opened because of physics (the low power of threshold-free light), and it got crowded because several companies already held the manufacturing base to build that physics.

3. What Is Public and What Is Still Open

This is as far as public sources take us. Where Seyedi went, what OSRAM wrote down and what it is reinterpreting [1][2], that Marvell co-develops microLED interconnect as Mojo Vision’s largest investor [4], that Credo acquired Hyperlume to build a microLED light-source cable [6], and that Kopin and Fabric.AI are chasing GPU-to-GPU links with programmable microLED [8]. The names and the deals are all on the record.

What is not public is three things. First, who is OSRAM’s unnamed AI partner. The market names NVIDIA first because of Seyedi’s connections, but that agreement was signed before he joined, and the company has not disclosed the name [3]. Even across trade media, the names floated do not converge on one, and none of them, NVIDIA included, is company-confirmed. Second, which of these six routes actually takes the socket. Even inside the same microLED, reach and form factor split, so this is not a field where everyone wins or everyone loses. Third, given all that, where do you stand if you want to hold this wave through listed equity. A large cap that only carries exposure and a name that gains beta as the field grows are not the same thing.

The answers to these three questions, the full map of the six players, the reach sub-map, the structure of the Marvell versus Credo proxy fight, and the valuation by listed route, are worked out below. One thing I will say up front. The real contest here is not “six microLED companies.” It is a two-front fight in which two connectivity challengers hedge across microLED and silicon photonics. Who those two companies are and why they collide over the same seat is the center of this piece.