The AI Light Source War Is Not a Speed Race: InP, VCSEL, and μLED Are Buying Different Distances

$AAOI $LITE $COHR $SIVE $ALMU $AVGO, plus PicoJool, Avicena | Data Center Light Source Map

When PicoJool unveiled its 200G VCSEL and 32x50G μVCSEL on June 15, 2026, a 30-year-old technology landed back on the table as an AI data center light source candidate [1][3]. Around the same window, Avicena, back in the spotlight before and after the PicoJool news, was pushing a non-laser GaN μLED link, driving Tx energy from 200fJ/bit in September 2025 down to 80fJ/bit in November 2025 [4][8]. Data center light sources are now splitting into three material systems and structures: InP edge-emitting laser, GaAs VCSEL, and GaN μLED. But the question the market asks, “who builds the faster laser,” is not the real one. The real axis is which light source the reach, lane count, and serialization cost actually call for. This piece lays out the physics of the three, then uses two axes, “fast and narrow” and “slow and wide,” to map which source takes which seat and which companies already sit there. Related tickers: $AAOI, $LITE, $COHR, $SIVEF, $ALMU, $AVGO.

Contents

Intro: Why a 30-Year-Old Light Came Back

Why the Light Source Is the Data Center’s First Gate

Three Light Sources: InP Edge-Emitting Laser, GaAs VCSEL, GaN μLED

The Quadrant: Fast and Narrow vs Slow and Wide

Supply Chain Map: Who Makes Which Light

PicoJool’s Bet and Avicena’s Bet

Scenarios and Monitoring

References & Sources

1. Intro: Why a 30-Year-Old Light Came Back

On June 15, 2026, a Silicon Valley startup called PicoJool unveiled its 200G VCSEL product family [1]. Bandwidth above 37GHz per channel, with quad 100G, quad 200G, and a 32x50G NRZ μVCSEL. Pat Gelsinger (former Intel CEO, now a partner at Playground Global) is on the investor list, and production runs at WIN Semiconductor, the foundry that has shipped more than a billion VCSELs for 3D sensing [1][2].

What makes this announcement matter is that VCSEL is not just a legacy part anymore. It came back as a scale-up optical I/O candidate. VCSEL has been the workhorse of short-reach data center optics since 1996 [3]. Through the AI cycle it sat on the bench under the verdict “cannot go far, speed is capped,” and now that 30-year-old light is back with an 800G, 1.6T, and 3.2T roadmap [1].

Around the same time, another light source rose from the opposite direction. Avicena’s GaN μLED. It is an LED rather than a laser, and it pushed Tx power from 200fJ/bit in September 2025 down to 80 femtojoules per bit in November [4][8]. The market asks “who builds the faster laser,” but the real answer is “which topology can absorb the serialization cost.” Scale-out has to travel far on few fibers, so the InP edge-emitting laser holds; scale-up runs short distances where power and latency matter more, so VCSEL and μLED open back up.

Takeaway: A data center light source is not one thing. InP laser, GaAs VCSEL, and GaN μLED chase different seats with different physics.

2. Why the Light Source Is the Data Center’s First Gate

Bandwidth between GPUs in an AI data center is climbing from 800G to 1.6T, 3.2T, and 6.4T, and copper cannot keep up on distance and power. So the connection is moving from electrical to optical.

The first place that bottlenecks in the move to light is the source itself. Silicon has an indirect bandgap, so it cannot generate light efficiently. You can build waveguides and modulators, and add germanium for detectors, but high-performance light sources are a different story. Research tracks like the silicon Raman laser and heterogeneous integration exist, but commercial data center light sources still depend mostly on III-V gain materials such as InP, GaAs, and GaN.

This matters for investors because the cost and supply bottleneck of an optical module concentrates at the source. A standard EML-based 800G module needs eight 100G EMLs, putting the laser cost alone in the $80 to $100 range per module (industry estimate), while putting a CW laser outside and modulating on the SiPh chip ends with only 2 to 4 sources, dropping to roughly $20 to $40 (industry estimate). That structural cost gap is what keeps lifting SiPh share. I covered this economics, and the $AAOI case that took it head on through vertical integration, in depth here: $AAOI, From $10 to $150.

3. Three Light Sources: InP Edge-Emitting Laser, GaAs VCSEL, GaN μLED

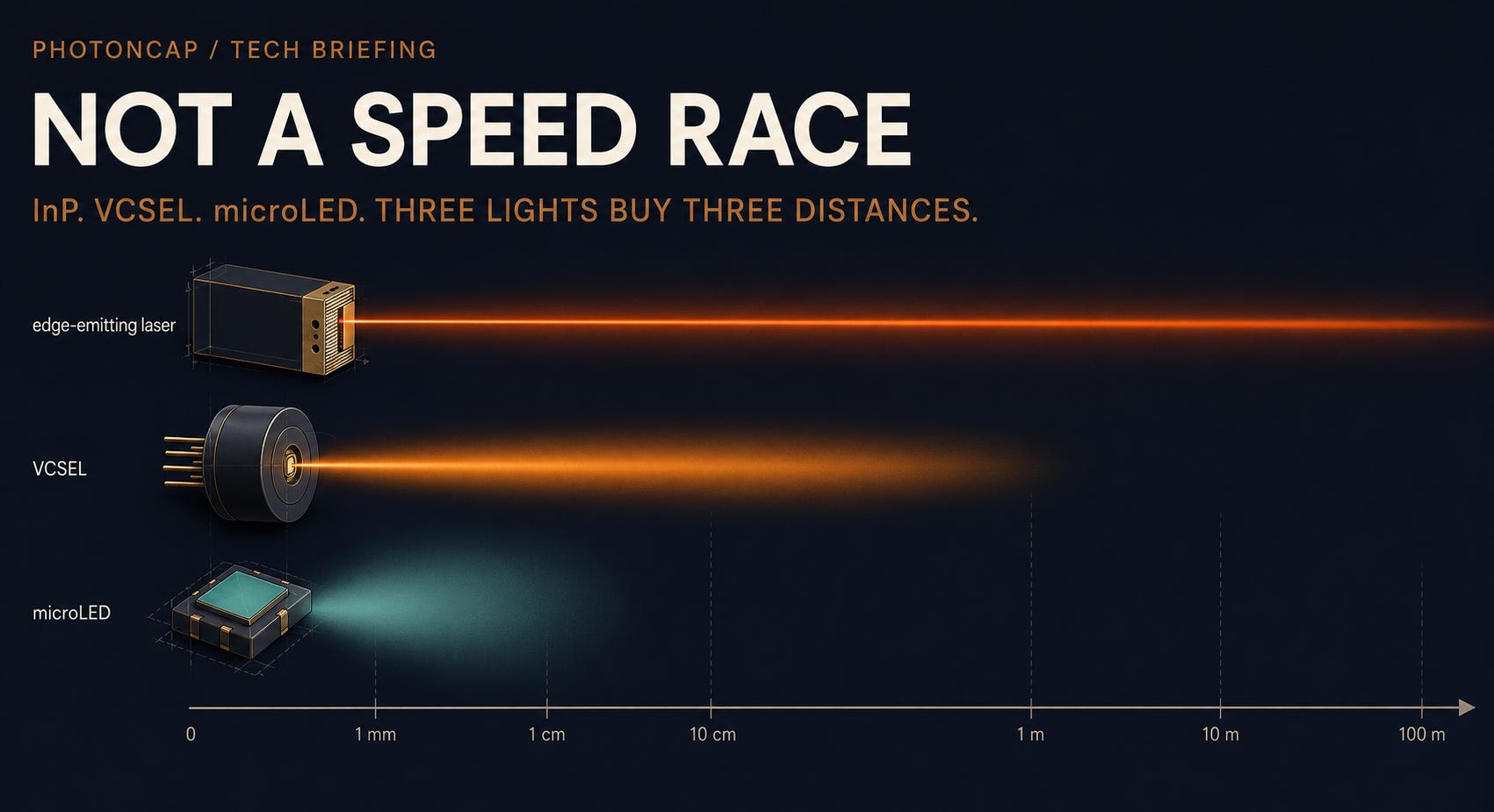

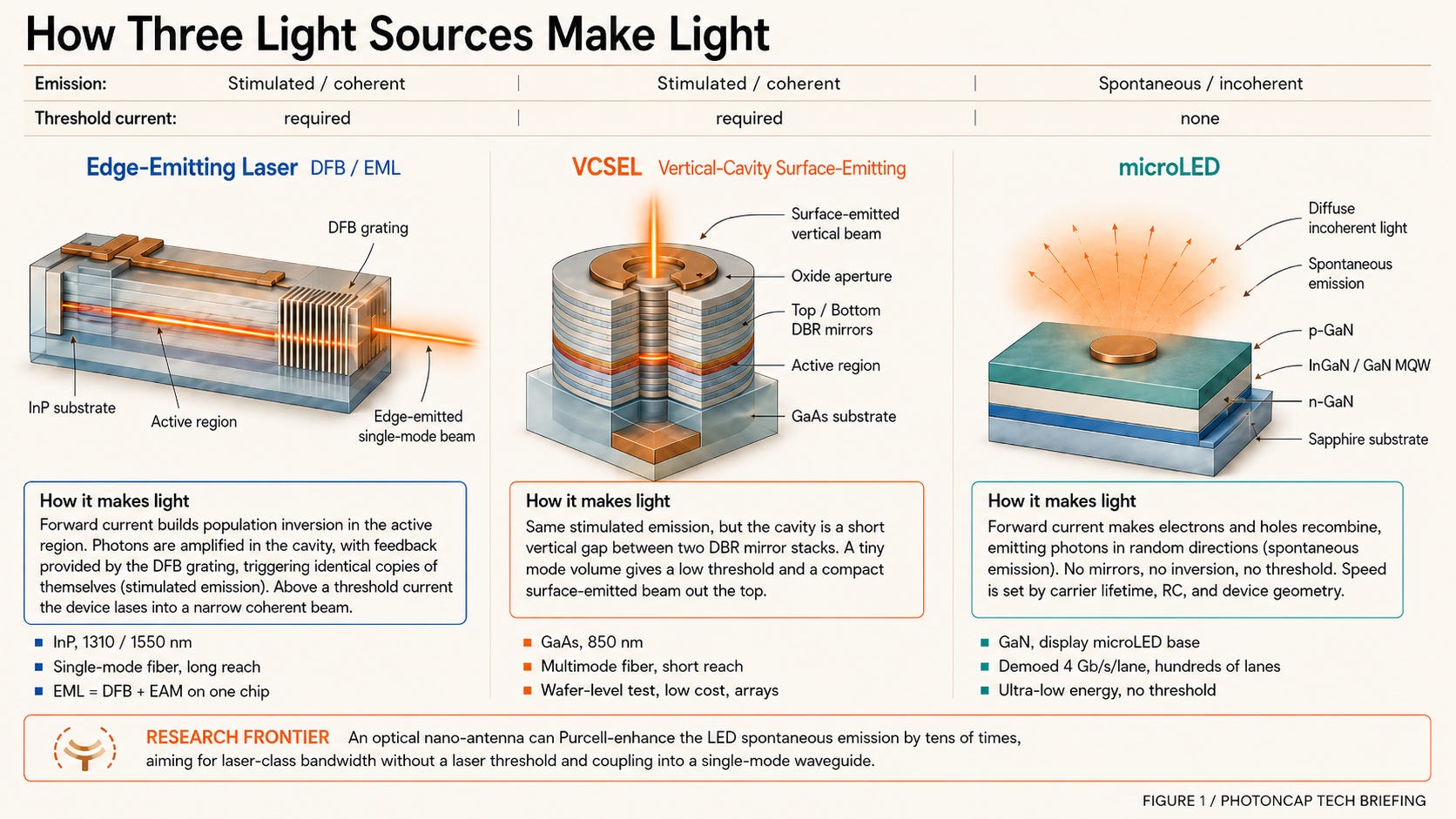

Start with one big split. Light sources divide by how they make light. A laser amplifies light through stimulated emission, so it has a narrow linewidth and strong coherence. An LED runs on spontaneous emission, so it has a broad spectrum and no coherence, an incoherent source. And a laser needs a threshold current to start lasing, while an LED has no threshold. These two things, the presence or absence of coherence and of a threshold current, are the root of how reach and power split. One thing to flag: VCSEL is also a laser. The edge-emitting laser and the VCSEL both run on stimulated emission; what differs is the structure (edge emission vs surface emission) and the material system (InP vs GaAs). Let us look at the three that actually get used in data centers, one at a time.

3-1. Edge-Emitting Laser (DFB / EML / CW)

This is an edge-emitting laser, where light leaves the side of the chip. It is the workhorse of today’s 800G and 1.6T modules. If it emits light and loads data at the same time it is an EML; if it just emits steady light and leaves modulation to the SiPh chip it is a CW laser. The way InP DFB, GaAs quantum dot, and monolithic approaches bet on different time horizons for this light source seat is laid out here: The Silicon Photonics Light Source War.

The Silicon Photonics Light Source War: Same Problem, Three Solutions (Small Cap)

Intro Sivers Semiconductors (OTCMKTS: SIVEF) surged +63.62% and QD Laser (TYO: 6613) jumped +33.39% over the past five days. What do these two microcaps have in common? They’re both light source suppliers for silicon photonics (SiPho).

Material: InP. Mostly the 1310 / 1550nm bands

Emission: stimulated. Light bounces between two end mirrors and amplifies, giving a narrow linewidth and strong coherence

Fiber: single-mode (SMF). Long reach (km class)

Modulation: EML combines a DFB and an EAM on one InP chip. CW does no modulation; the SiPh MZM/MRM handles it

Weak spot: a threshold current means a high power floor, and per-chip cost is high

Seat: 800G/1.6T pluggables, CPO external light source (ELS)

3-2. VCSEL (Vertical-Cavity Surface-Emitting Laser)

As the name says, this is a surface-emitting laser with a vertical cavity. Light comes straight up out of the top of the chip. A short cavity sits between stacked DBR mirrors above and below, and an oxide-narrowed aperture shapes the output. It has been the workhorse of short-reach data center optics since 1996 [3], and it is the light PicoJool pulled back out at 200G [1].

Material: GaAs. Mostly 850nm

Structure: top and bottom DBR mirrors and an oxide aperture. Surface emission

Fiber: multimode (MMF). Short reach (tens of meters)

Strength: you can test it on-wafer and print it in arrays, so it is dramatically cheap

Weak spot: being multimode caps the reach and speed of a single lane

Workaround: pivoting to many slow lanes in parallel (32x50G μVCSEL, slow and wide) [1]

Seat: short-reach scale-up, NPO

3-3. μLED (micro-LED)

From here it is not a laser anymore. It is an LED with no cavity, that is, spontaneous emission. So it is an incoherent source with light that spreads and a broad spectrum, but having no threshold current becomes a decisive weapon at short reach. It turns on and off fast even at very small currents. Avicena closing a 4Gb/s link at around 100µA drive and getting down to 80 femtojoules per bit comes straight out of this physics [8].

Material: GaN. Built on display μLED process foundations

Emission: spontaneous (LED). No cavity, so incoherent with a broad spectrum

Threshold current: none. So ultra-low power. From 200fJ/bit in September 2025 down to 80fJ/bit in November [4][8]

Speed/reach: the link runs about 4Gb/s per lane, with reach above 10m. On-chip data (around 2Gb/s class) goes straight out as light with no serialization [8]

Receive: silicon PD array. TSMC builds the visible-light PDs on its image-sensor (CIS) process [9]

Seat: ultra-short-reach chip-to-chip, memory interconnect [5]

3-4. Research Frontier: nanoLED and the Optical Antenna (and How It Differs from μLED)

If μLED is “many slow LEDs in parallel,” there is research going the exact opposite way. Making a single LED as fast as a laser. That is the optical antenna-LED pushed by Eli Yablonovitch and Ming Wu’s group at Berkeley. An LED is slow because spontaneous emission itself is slow, but attaching a nanometer-scale optical antenna to the emitter can raise the spontaneous emission rate by tens of times through the Purcell effect. With a strong enough antenna, spontaneous emission can even become faster than stimulated emission. The group has shown coupling an antenna-LED’s light into a single-mode waveguide at high efficiency (around 70% in an InP-waveguide demo) [6], and has gone as far as analyzing how to bundle such nanoLEDs over WDM [7]. The core is one line. Use an optical antenna to speed up spontaneous emission and lift the LED’s modulation bandwidth.

Here is the μLED vs nanoLED difference in short.

μLED: micron scale. Borrows the display GaN ecosystem. The spontaneous emission rate is unchanged, so each lane is slow, and total bandwidth is filled by hundreds of parallel lanes. Close to commercial (Avicena).

nanoLED: nanometer scale with an optical antenna attached. Purcell speeds up spontaneous emission to make a single LED fast. It aims at single-mode waveguide coupling without a threshold. Still at the paper and demo stage [6][7].

So μLED solves it “wide” and nanoLED solves it “fast,” two different routes to the same advantage, the threshold-free LED. Both start from the same place: dodging the laser’s threshold current.

[Figure 1: Three-panel structural cutaway. (1) Edge-emitting laser: InP, edge emission, a single-mode beam exits sideways between two cavity mirrors. (2) VCSEL: GaAs, top and bottom DBR mirrors and an oxide aperture, a vertical beam exits the top. (3) μLED: GaN, diffuse light with no cavity spreads upward. Five key bullets beside each panel. Top band contrasts “Stimulated emission / coherent” vs “Spontaneous emission / incoherent” and “Threshold current: needed / needed / none”.]

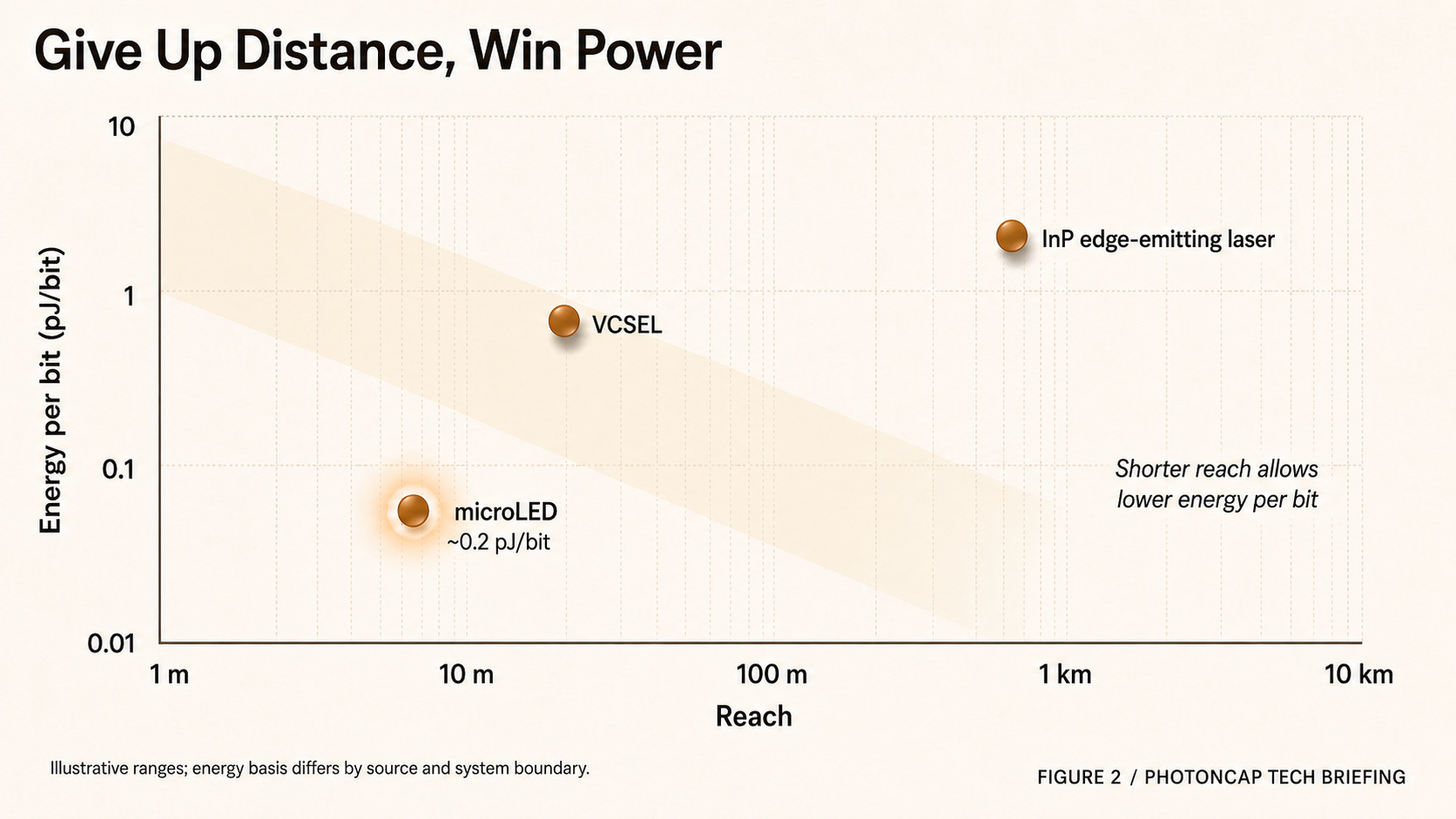

Wrap the three sources in one line: InP laser goes far, fast, and expensive. VCSEL goes near, cheap, and parallel. μLED goes nearer, with less power, and wider.

[Figure 2: Reach (x axis, log) vs energy per bit (y axis). InP laser / VCSEL / μLED plotted as points to visualize the “give up distance, power drops” tradeoff.]

Takeaway: The root of the split is physics. Whether there is coherence and whether there is a threshold current decide reach and power.

That covers the public physics and industry structure. The investment question here is not the physics explainer, it is socket allocation. Put the three sources on the “fast and narrow” and “slow and wide” axes and which quadrant takes which application, and which company already sits there? The company-level detail is in the two pieces linked above, and the full map with VCSEL and μLED added is completed below.