$AAOI, From $10 to $150: How a Cable TV Parts Company Became an AI Optics Stock

Abstract

Applied Optoelectronics ($AAOI) has surged 1,440% in one year. Starting from a $2 bottom in 2023, the stock broke through $150 in April 2026. This company originally made cable TV (CATV) equipment. This article analyzes the structural backdrop behind AAOI’s EML (Electro-absorption Modulated Laser) transceivers rapidly capturing 800G market share, and examines whether this position can hold against SiPh (Silicon Photonics) based solutions as the industry moves to 1.6T/3.2T. We compare AAOI’s valuation, technical positioning, and risks against competitors including Lumentum ($LITE) and Coherent ($COHR). Related tickers: $AAOI, $LITE, $COHR, $MRVL, $TSEM, $GFS.

Contents

Intro: Why AAOI, Why Now

What is AAOI: From CATV to AI

Anatomy of the Orders: $300M+ in Contracts

EML vs SiPh: 800G Works, But What About 1.6T?

Competitive Landscape: LITE, COHR, and Innolight

Valuation and Risks

Scenario Analysis & Monitoring Points

Closing

References & Sources

1. Intro: Why AAOI, Why Now

Today (April 10), Lumentum CEO Michael Hurlston told Bloomberg: “The capex numbers from the U.S. hyperscalers are enormous, and there seems to be no end in sight. We would be sold out through all of 2028 within two quarters.”[1] Orders filled through 2028. A month ago, he said “sold out through end of 2027.”[2] Visibility just extended by another year.

This is not just a Lumentum story. The entire optical component market has entered a structural supply shortage. And right in the middle of that shortage, an unexpected beneficiary has emerged.

Applied Optoelectronics, $AAOI.

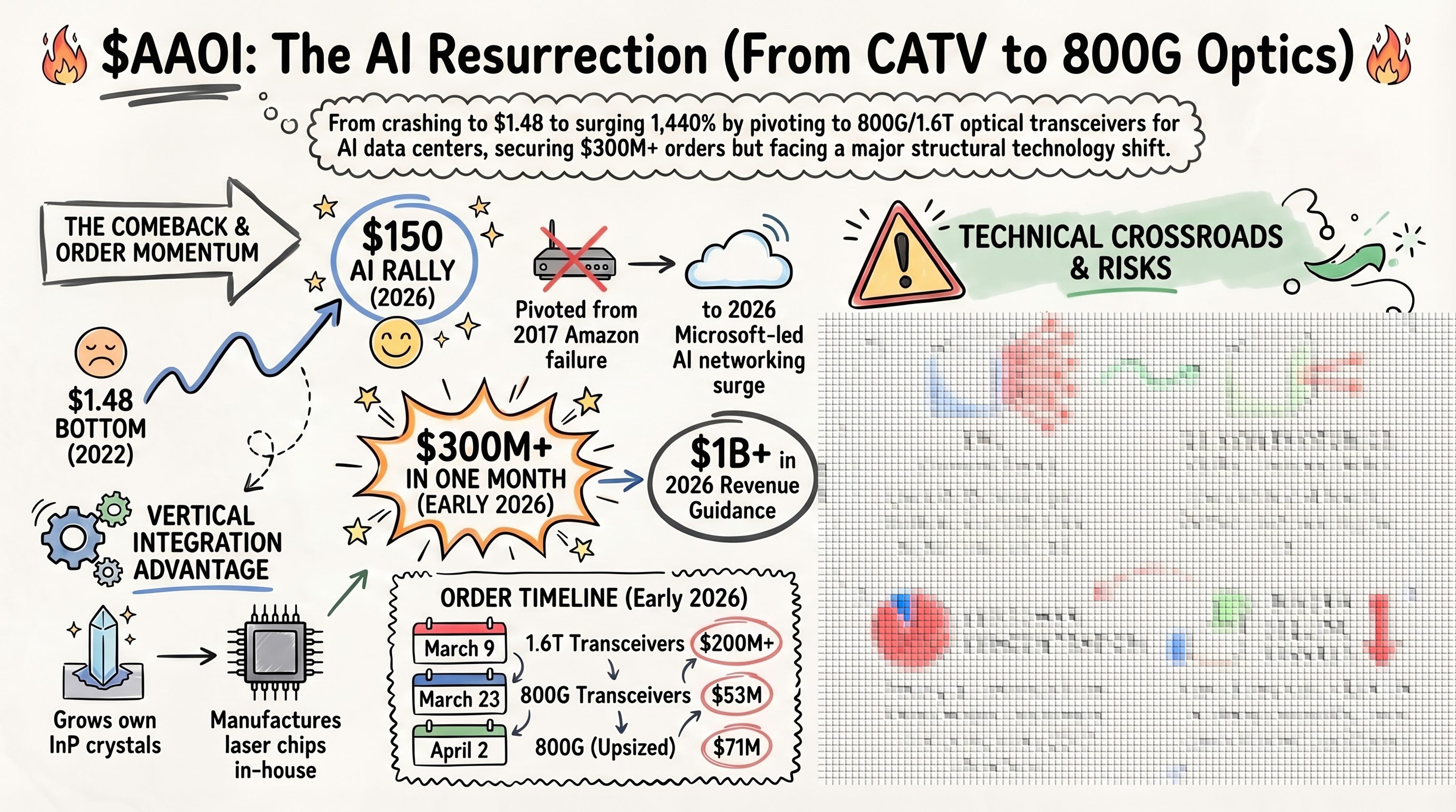

Stock price a year ago: $10. Now: $150. The rally has real substance behind it. The question is how long that substance lasts.

This article covers how AAOI pivoted from a CATV parts company to an AI optics stock, what the recent $300M+ order wave actually looks like, and whether its EML technology base can survive the SiPh transition. We compare against LITE, COHR, and others along the way.

2. What is AAOI: From CATV to AI

To understand AAOI, you need to start with its history. This is not the company’s first time in the spotlight.

The First Cycle: 2017 Glory and Collapse

Founded in 1997 by Dr. Thompson Lin, AAOI originally made optical transceivers, headend equipment, and lasers for CATV (cable TV) networks. HFC (Hybrid Fiber-Coaxial) network backbone equipment, basically the plumbing behind cable internet.

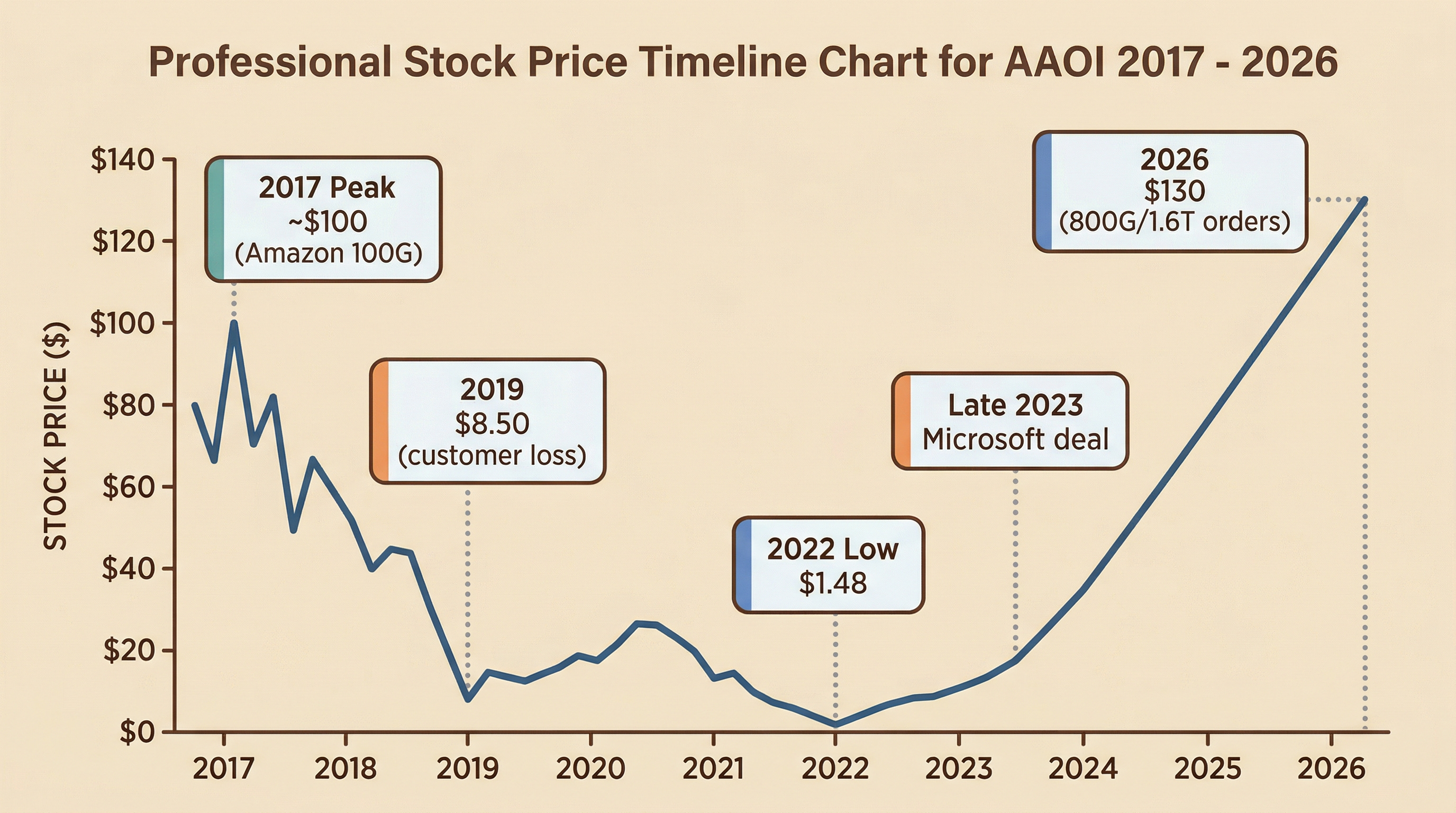

Then 2017 hit. During the early cloud buildout, demand for 40G/100G transceivers (modules that convert data into optical signals and send them over fiber) surged, and AAOI’s stock shot to $100. The main customer at the time was Amazon.[3]

What followed was the problem. Larger competitors moved in, and AAOI’s revenue structure, heavily dependent on Amazon, collapsed along with the customer relationship. The stock fell 91% from $100 to $8.50 (August 2019).[4] That was not the bottom. After a brief post-COVID bounce, it hit an all-time low of $1.48 in July 2022.[4]

The Pivot: CATV Cash Cow + Data Center Transition

AAOI in 2022-2023 was essentially a CATV company. As of Q3 2025, CATV still accounted for 66% of total revenue.[5] Data center was at 24%. In September 2022, the company even agreed to sell its Chinese factories to Yuhan Optoelectronic for $150M, planning to double down on CATV (the deal was terminated in September 2023 due to CFIUS issues).[34]

The turning point came in late 2023. A strategic supply agreement with Microsoft kicked off a serious pivot toward 400G/800G data center transceivers.[3]

This is where AAOI’s core strength showed up. The company is vertically integrated. It handles everything from InP (indium phosphide) semiconductor crystal growth to EML laser chip fabrication to final transceiver module assembly, all in-house.[3] Most transceiver companies buy their laser chips externally. AAOI makes its own.

Current State: FY2025 Results

Full-year 2025 revenue was $455.7M, up 82.8% year-over-year.[6] Annual revenue mix:

CATV: 53.8% (Digicomm at 53.1% of annual revenue)

Data Center: 42.9% (Microsoft at 31% of annual revenue)

Telecom/FTTH: the remainder[7]

The quarterly picture tells a different story, though. In Q4 2025, data center grew rapidly, shifting the composition. Q4 top 3 customers: CATV customer at 39%, data center customer at 31%, another DC customer at 21%, totaling 91%.[15] On a full-year basis, Digicomm was at 53%, but as data center surged in Q4, CATV’s relative share dropped. This ratio will flip further in 2026.

Q4 2025 revenue hit $134.3M, a quarterly record, with near break-even on a non-GAAP basis (EPS -$0.01).[6] We will revisit the customer concentration numbers in the risk section.

Key takeaway: AAOI hit $100 in 2017 and crashed to $1.48. Now it is in its second cycle, with a CATV cash cow funding a data center pivot. Vertically integrated EML laser manufacturing is the core asset.

Now that we know what the company looks like, let’s look at what actually moved the stock. The orders that poured in starting March.

3. Anatomy of the Orders: $300M+ in Contracts

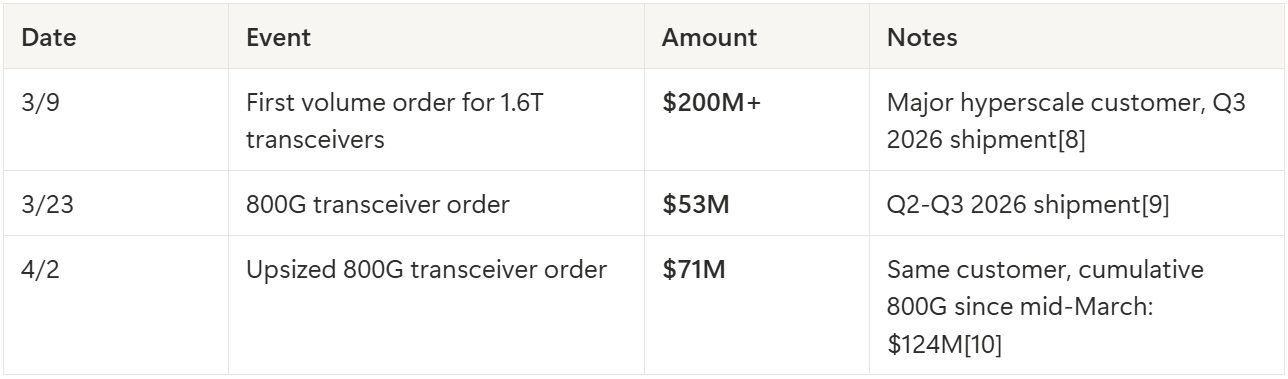

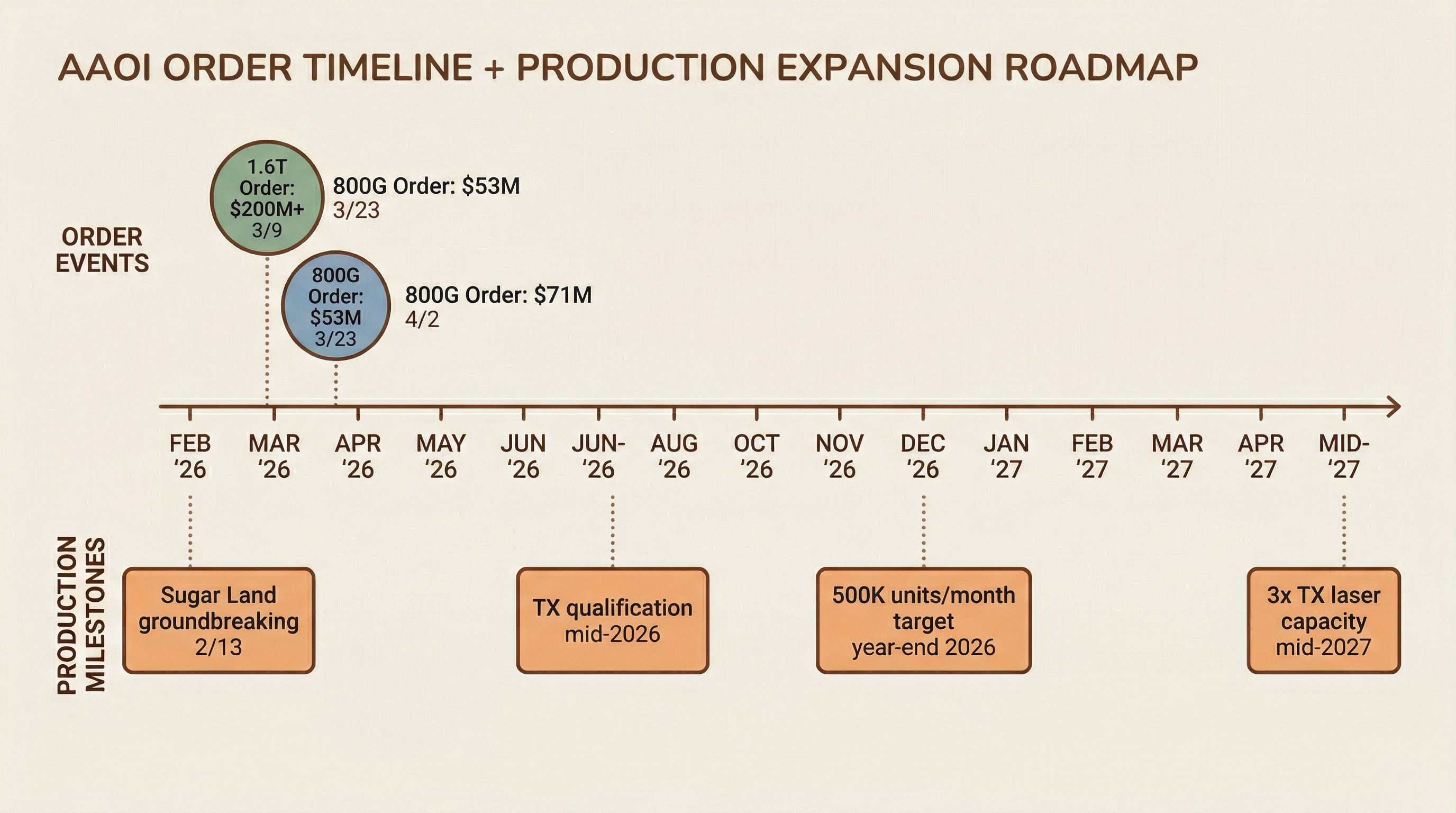

Here is what happened to AAOI in the span of one month starting March 2026:

Over $300M in orders landed in one month. For context, AAOI’s full-year 2025 revenue was $455.7M. More than double the existing backlog stacked up in a single month.

CFO’s Direct Quote

From the Q4 2025 earnings call, CFO Stefan Murry:

“This revenue level is limited by our production capacity and supply chain, not market demand, which we believe is much larger.”[11]

Revenue is capped by production, not demand. They can sell everything they make.

2026 Guidance

Based on these orders, management guidance for 2026:

Annual revenue exceeding $1B (119% growth from $455.7M in 2025)[6]

Non-GAAP operating profit above $120M[6]

Non-GAAP profitability starting Q2 2026[6]

Q1 2026 guidance: revenue $150-165M, non-GAAP net loss $0.3-7M[12]

Longer-term targets are even more aggressive. Year-end target of 500,000 units/month across 800G and 1.6T. Mid-2027 monthly transceiver revenue potential estimated at roughly $378M (100G/400G ~$90M, 800G ~$217M, 1.6T ~$71M).[13]

Who is Buying?

Officially, the announcements only say “major hyperscale customer.” The market believes it is Oracle and Microsoft.[14] The 10-K explicitly names Microsoft as the key data center customer for 2025[7], and the 1.6T order is widely attributed to Oracle.[14]

The CFO directly stated on the earnings call that of the projected $1B in 2026 revenue, subtracting ~$300M in CATV leaves ~$700M in data center, and the majority of that will come from two large hyperscalers, with roughly equal weight by year-end.[15]

Capacity Expansion

To fulfill these orders, AAOI is running three parallel tracks:

Sugar Land, TX new facility: Groundbreaking February 2026, targeting mid-to-late 2026 operations. Texas laser capacity to triple by mid-2027[13]

Taiwan facility expansion: Existing transceiver assembly line expansion

Automated production lines: Expanding U.S. production share (over 90% of 800G/1.6T component value is already non-China sourced)[13]

Funding is coming via a $250M ATM (At-The-Market) offering set up on February 26, expanded to $500M on March 12.[16] Approximately 2.48 million shares were already sold for $250M in proceeds.[16]

Key takeaway: $300M+ in orders arrived within a single month, and management is guiding for $1B+ in 2026 revenue. Most of that revenue will be concentrated in two hyperscalers.

That covers “what is happening at AAOI right now.” The orders are real. Capacity expansion is underway.

But here is a question worth pausing on. AAOI’s transceivers are EML-based. With the industry moving toward SiPh, can this technology base survive into the 1.6T and 3.2T generations? And where does AAOI stand relative to Lumentum and Coherent, both backed by $2B from NVIDIA?

The analysis continues below.