Superconducting or Trapped Ion, They All Buy the Same Light: The Hidden Layer That Wires Quantum Computers Rack to Rack

$IONQ $RGTI $XNDU $GFS $TSEM | Quantum Optical Interconnect Stack

This piece started from a thought I posted on X.

The photonic approach uses light directly, but even platforms where light is not the qubit, superconducting (AWS), neutral atom (QuEra), trapped ion (IonQ), have to split into modules and wire them with light to grow the qubit count. A quantum signal differs from a classical one. Modern communication sends hundreds or thousands of photons at once, so losing 10 percent still lets you recover 1001010110 from the SNR, but quantum information rides on a single particle. Whether that one photon arrives becomes probability, and once loss crosses roughly half, the 1001010110 you sent can read out as 000... So the lowest loss optical network is not a choice but a requirement.

The same intuition shows up in the people. The AWS quantum director is Oskar Painter of Caltech, QuEra’s co-founder is Mikhail Lukin of Harvard who has published widely in photonics, and IonQ’s co-founder is Professor Jungsang Kim, who studied both trapped ions and optical systems. Regardless of qubit type, the people who built each camp came from photonics.

Qubits split into four families: superconducting, trapped ion, neutral atom, and photonic. But the moment you try to go past the limit of a single chip, a single fridge, or a single trap and wire rack to rack, all four platforms funnel toward the same exit. A telecom band photon (C-band 1550 nm or O-band), optical fiber, and a single photon detector. This piece looks past the qubit modality race at the optical interconnect layer underneath it. Over the past twelve months IonQ has bought optical interconnect companies including Lightsynq, ID Quantique, and Qubitekk, and acquired Oxford Ionics for $1.075B [1][2][3]. A trapped ion company vertically integrating an optics supply chain is the market admitting, ahead of everyone, that optical interconnect is the bottleneck regardless of modality. And as we will see, that signal is written not only into M&A but into the resumes of the scientists leading each camp. If picking the winning quantum pure-play is hard, the conclusion here is that you look first at the components and foundry layer that everything converges on through the telecom photon.

Table of Contents

Intro: Why IonQ Bought a Pile of Optical Interconnect Companies

Why It Has to Be Light: Superconducting, Trapped Ion, Neutral Atom, Photonic

Here Is the Real Question

Layer 1. Light Source: Every Species Has Its Own Wavelength

Layer 2. Conversion: Where the Difficulty Splits by Orders of Magnitude

Layer 3. Transport, Routing, and Who Actually Fabs the Chips

Layer 4. Detection: Catching Single Photons

The Convergence Is Not Only in Components, the People Converge Too

The Convergence Map: Four Platforms Buy the Same Parts

Investment Positioning: Where Listed Exposure Splits

Scenarios and Monitoring

Closing

Intro: Why IonQ Bought a Pile of Optical Interconnect Companies

Start with the facts.

Here is the list of companies IonQ (NYSE: IONQ) has acquired or taken a stake in over the past twelve months [1][2][4]. Lightsynq Technologies (a Harvard spinout team that built the first quantum repeater, with photonic interconnect and quantum memory IP), ID Quantique (a single photon detector and QKD company, majority stake), Qubitekk (entangled photon pair source), Capella Space, and Vector Atomic. On top of that, it acquired Oxford Ionics for $1.075B [3]. IonQ’s core business is trapped ion quantum computers. Yet half the acquisition list is photon, detector, and repeater companies.

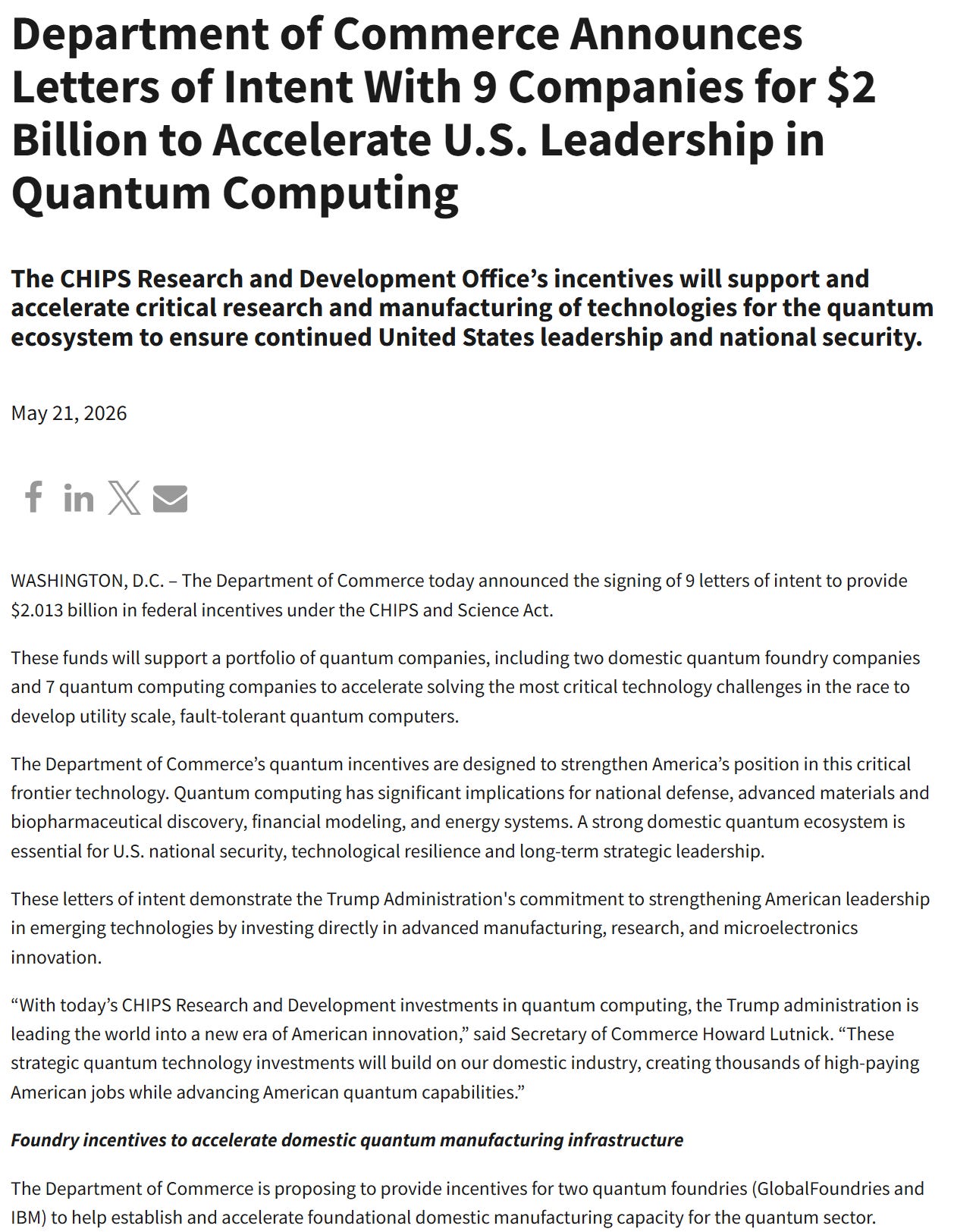

And this is not IonQ’s bet alone. In May 2026 the U.S. Department of Commerce issued letters of intent for more than $2B in CHIPS Act support to nine quantum companies, centered on the quantum foundries of GlobalFoundries ($375M) and IBM ($1B) [5]. The money went not to the qubit itself but to the manufacturing and connection layer that makes and wires qubits together. From an investor’s seat, that means billions are already flowing into the manufacturing and connection layer beneath a qubit race that has no clear winner yet. It is a signal that there is a place you can bet without waiting for the modality outcome. That layer is exactly what this piece follows to the end.

The Real Quantum Race: NVIDIA, NQI, and China’s State Capital

As of April 2026, quantum computing has moved beyond the laboratory and into the arena of national strategic competition. NVIDIA announced its quantum AI model Ising on April 14, and the US Senate Commerce Committee advanced the NQI (National Quantum Initiative) Reauthorization Act on April 14. DARPA’s QBI (Quantum Benchmarking Initiative) has moved 11 companies to Stage B, and the White House is drafting a quantum executive order. On the other side, China has designated quantum technology in its 15th Five-Year Plan, and is targeting a 4-satellite QKD constellation for operational deployment in 2026 following the Micius satellite. This article reframes the US-China quantum competition through an investment lens.

Strange, isn’t it? Trapped ion works by holding ions in a vacuum chamber with lasers and running gates on them. The qubit itself is not a photon. So why buy up so many optical interconnect companies?

The point is connection after modularization. Trapped ion or superconducting, to gather enough qubits you eventually have to split into modules, and once you split into modules you have to wire them back together. The only physical medium that can do that wiring is, in practice, light.

It is not only qubit fidelity or error correction that bottlenecks. The moment scaling moves from one chip to modules, the optical interconnect that wires qubits across modules rises as the next bottleneck. And this bottleneck is not the problem of any one modality. It is common to all four platforms.

Why does this matter to an investor? Experts disagree on which qubit modality wins. But if every winner still needs the optical interconnect layer, then looking at the connection layer underneath becomes a sturdier question than betting on a modality. Rather than picking the winner of the qubit race, you look at which parts get sold no matter which qubit wins. IonQ buying optical interconnect companies that look far from its core business is exactly that logic.

IonQ’s acquisition pattern is a bet that, separate from “which qubit wins,” the optical interconnect layer on top is a must.

Why It Has to Be Light: Superconducting, Trapped Ion, Neutral Atom, Photonic

When people hear “optical interconnect,” they usually picture connecting two distant points. Long haul telecom across continents, satellite optical links (LEO), and the rack to rack optical interconnect inside a data center. All three are long distance links. But the same physics applies at a far smaller scale. Connecting module to module inside a quantum computer. Whether the distance is tens of km or tens of cm, the fact that light is the answer as a low loss medium for moving information does not change. Optical interconnect is not one application of the telecom infrastructure we know. It is the common layer that every form of computing reaches as it scales.

The ladder of scale makes it clear. Continent to continent (thousands of km) is subsea optical cable, city to city (tens to hundreds of km) is the metro optical network, inside a data center (tens to hundreds of m) is rack to rack optical interconnect, and going down to between boards and chips (a few cm) you reach today’s co-packaged optics. Even as the distance shrinks, the moment there is a lot of information to move and loss and heat to cut, light pushes copper out. Module to module connection in a quantum computer is a new rung added at the very bottom of this ladder. And in quantum there is one more reason to use light even at short distance. You have to move information at the single photon level without breaking it with noise.

Let us start from why you cannot cram qubits into one place forever. The reason differs by platform, but the conclusion is the same.

First, a quick pass over how qubits are built. There are roughly four families [6]. Superconducting controls superconducting circuits with microwaves at cryogenic temperatures, and IBM, Google, Rigetti, and AWS sit here. Trapped ion holds ions in a vacuum with lasers and uses them as qubits, with IonQ and Quantinuum as the standard bearers. Neutral atom arranges neutral atoms in a lattice with optical tweezers, and includes QuEra, Pasqal, and Infleqtion. Photonic uses particles of light themselves as qubits, with Xanadu and PsiQuantum out front. Other families such as silicon spin and topological are also studied, but this piece centers on the four above.

The 1% Loss Wall (Part 1): Where Xanadu ($XNDU) Really Stands, Through the Lens of Three Nature Papers

Xanadu Quantum Technologies (XNDU) is a Canadian company developing photonic quantum computers, listed on NASDAQ/TSX in March 2026 via SPAC merger. The deal was presented at approximately US$3.0B pre-money equity value and US$3.1B pro forma enterprise value, with roughly US$300M raised at close. In this article (Part 1), we analyze the three papers Xana…

So let us see why each platform cannot stay in one module.

Superconducting qubits operate inside a dilution refrigerator, near 10 mK. Each qubit needs microwave control lines and coaxial cable, and pushing into the fault-tolerant regime of 10,000 to 1,000,000 qubits, the volume of that wiring, the amplifiers, and the microwave components runs far past the space and heat budget of a modern fridge [7]. Coaxial cable carries not just signal but heat. Every metal line going into the fridge is a heat ingress path. So connecting fridge to fridge is regarded as a practically unavoidable step for a large scale fault-tolerant quantum computer [8].

This is not only superconducting’s problem. In trapped ion, the more ions you add to one trap the denser the motional modes get and the harder gate control becomes, and in neutral atom arrays the field of view of the optics and the laser power limit how many atoms one module can hold. Even the photonic platform hits a wall in single chip yield as the component count grows. The method differs, the conclusion is the same. Past a certain scale, wiring several modules together becomes the realistic path rather than growing one module further. And to wire modules you need a medium to travel between them.

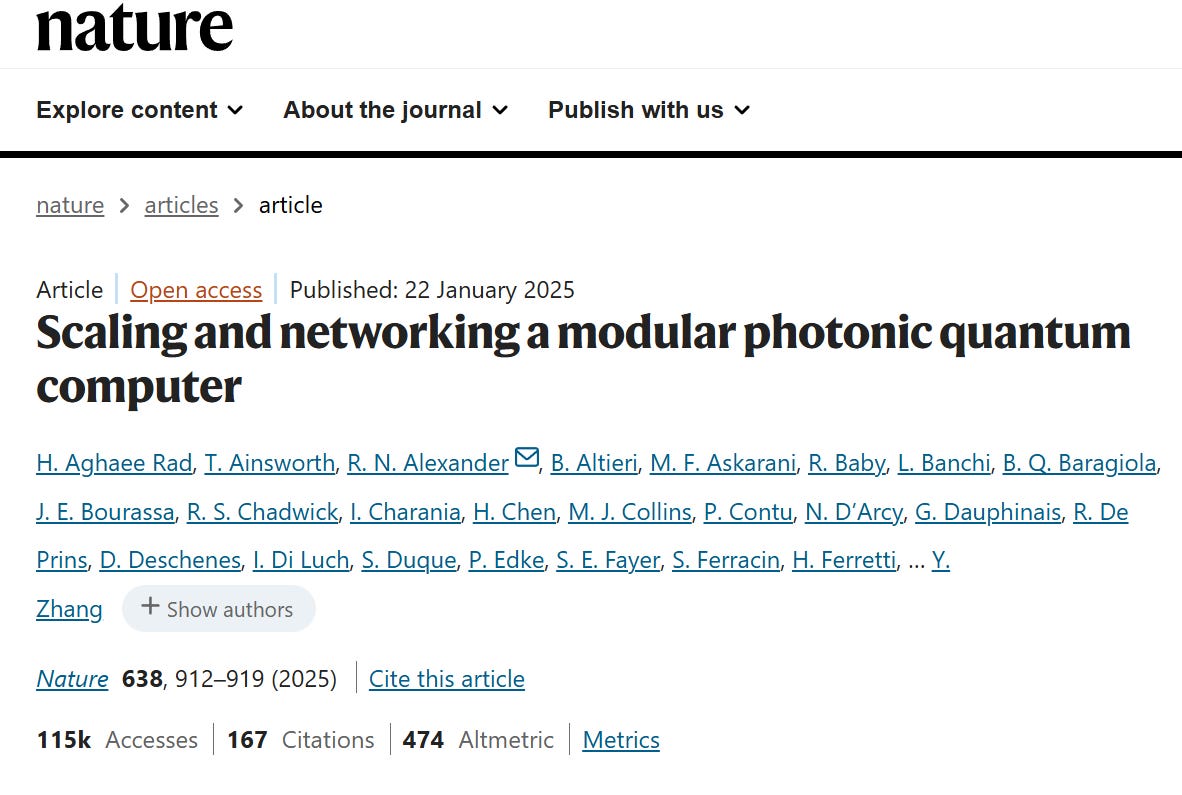

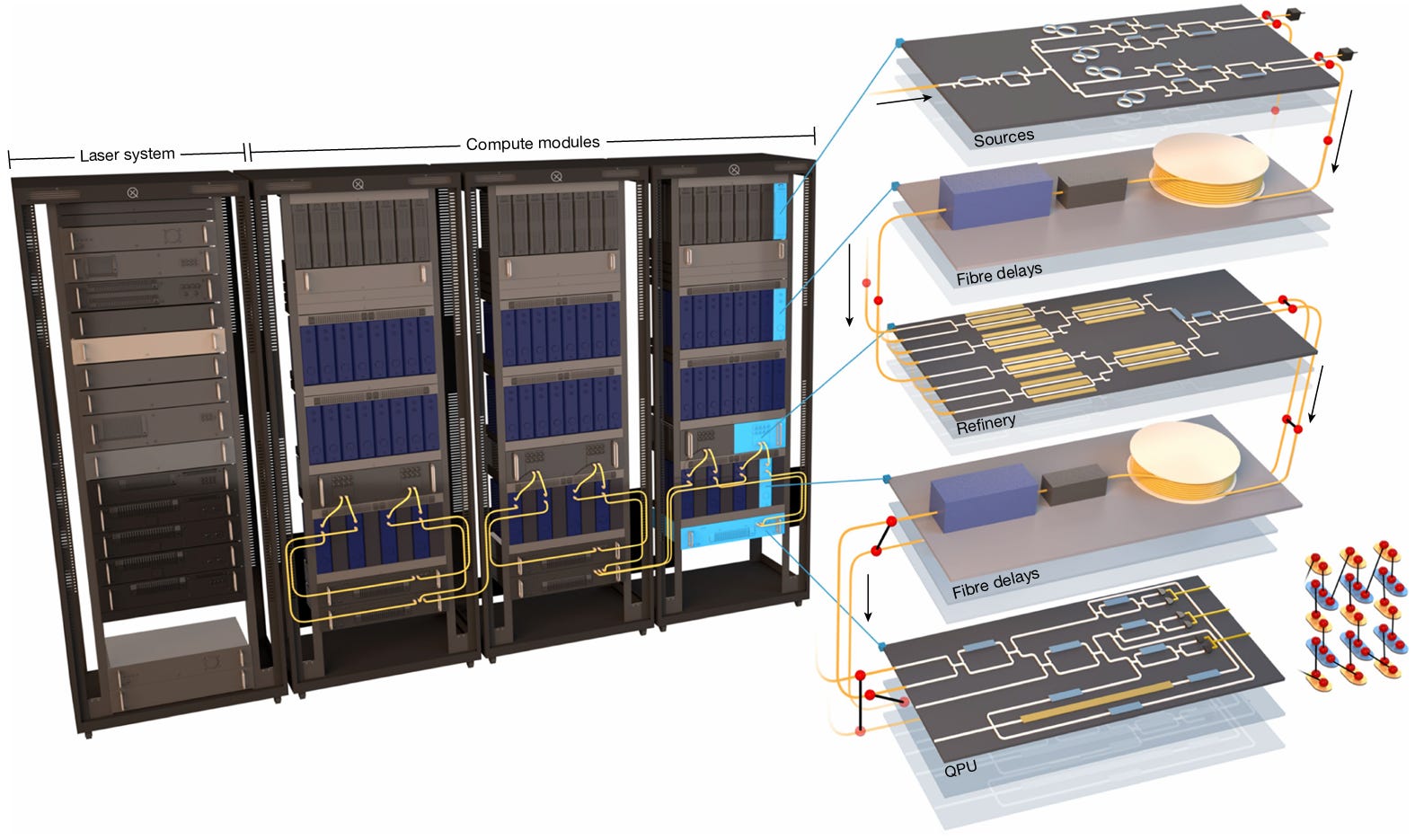

There is a familiar analogy. Classical computers also could not put transistors on one chip forever, so they split chips into many, chips into boards, boards into racks, and racks into data centers as they grew. The medium of that connection moved from copper to light as the distance grew. Just as connecting rack to rack inside a data center is ultimately optical communication. The quantum computer now stands at that wall of moving from chip to module, and the moment the distance grows, light is the answer just the same. In fact, in 2025 Xanadu presented a modular photonic quantum computer that ties four server racks together with optical fiber in Nature. It is a demonstration that a quantum computer can be built as fiber connected racks, like a data center. That said, the Nature paper itself is explicit that this is a sub-performant scale model, not a fault-tolerant machine [9].

Put differently, a quantum computer’s scaling roadmap becomes, past a certain point, necessarily an optical interconnect roadmap. The problem of making more qubits turns into the problem of sending the light those qubits emit far away without loss. So behind the qubit count headlines, how each company solves light source, conversion, and detection effectively sets the true speed of scaling. The place an investor should look is right behind that.

So the alternative is to swap coaxial cable for optical fiber. Optical fiber has a far smaller cross section and brings far less heat into the fridge than metal coaxial cable [7]. On top of that, its loss is dramatically lower. At the 1550 nm telecom C-band, fiber loss is about 0.18 dB/km, and at the O-band (1310 nm) about 0.32 dB/km [10]. Ultraviolet or visible light climbs to tens of dB per km in the same fiber and cannot travel more than tens of meters. To move a signal far, and cold, it has to be light, and specifically telecom band light.

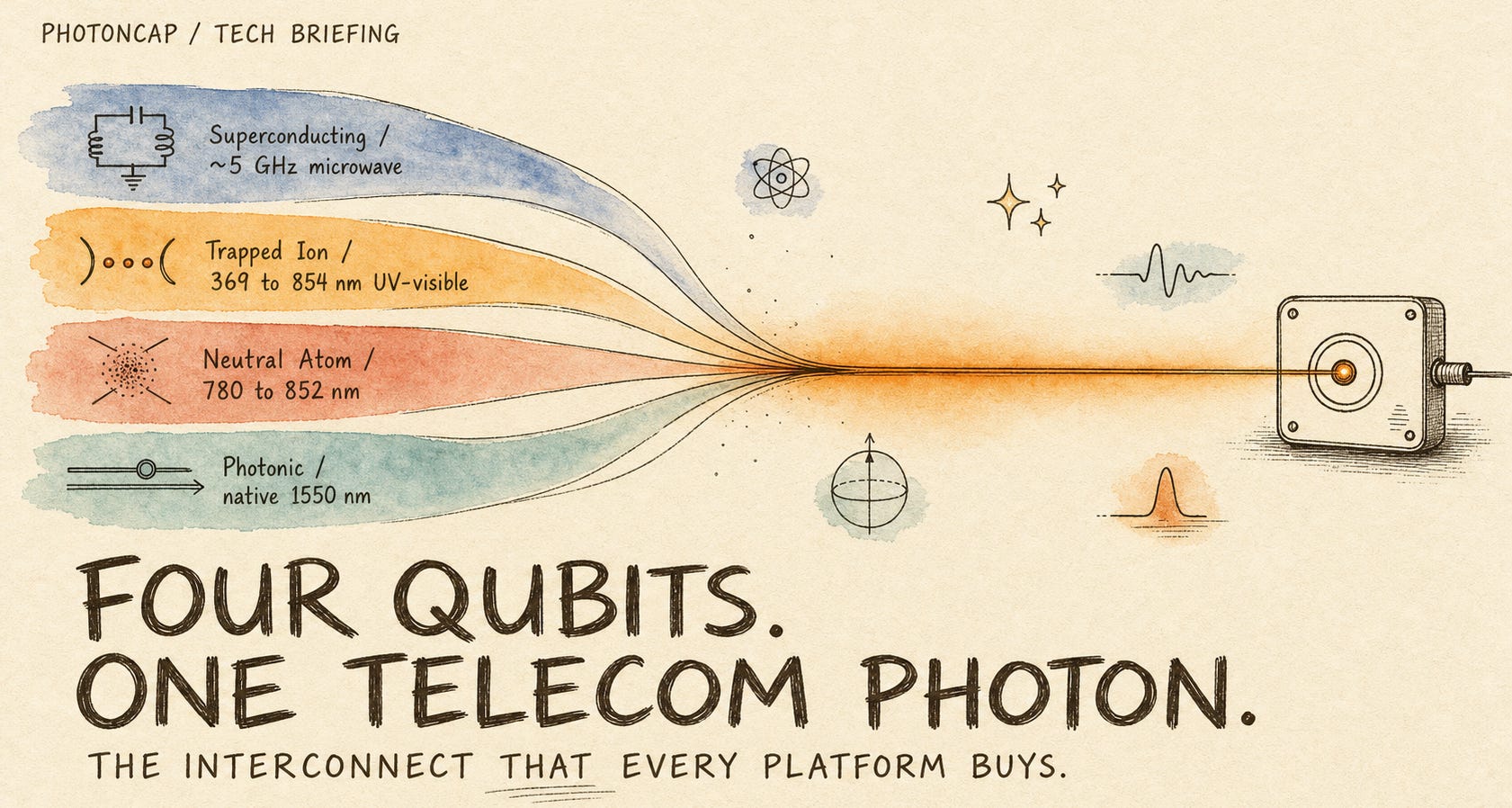

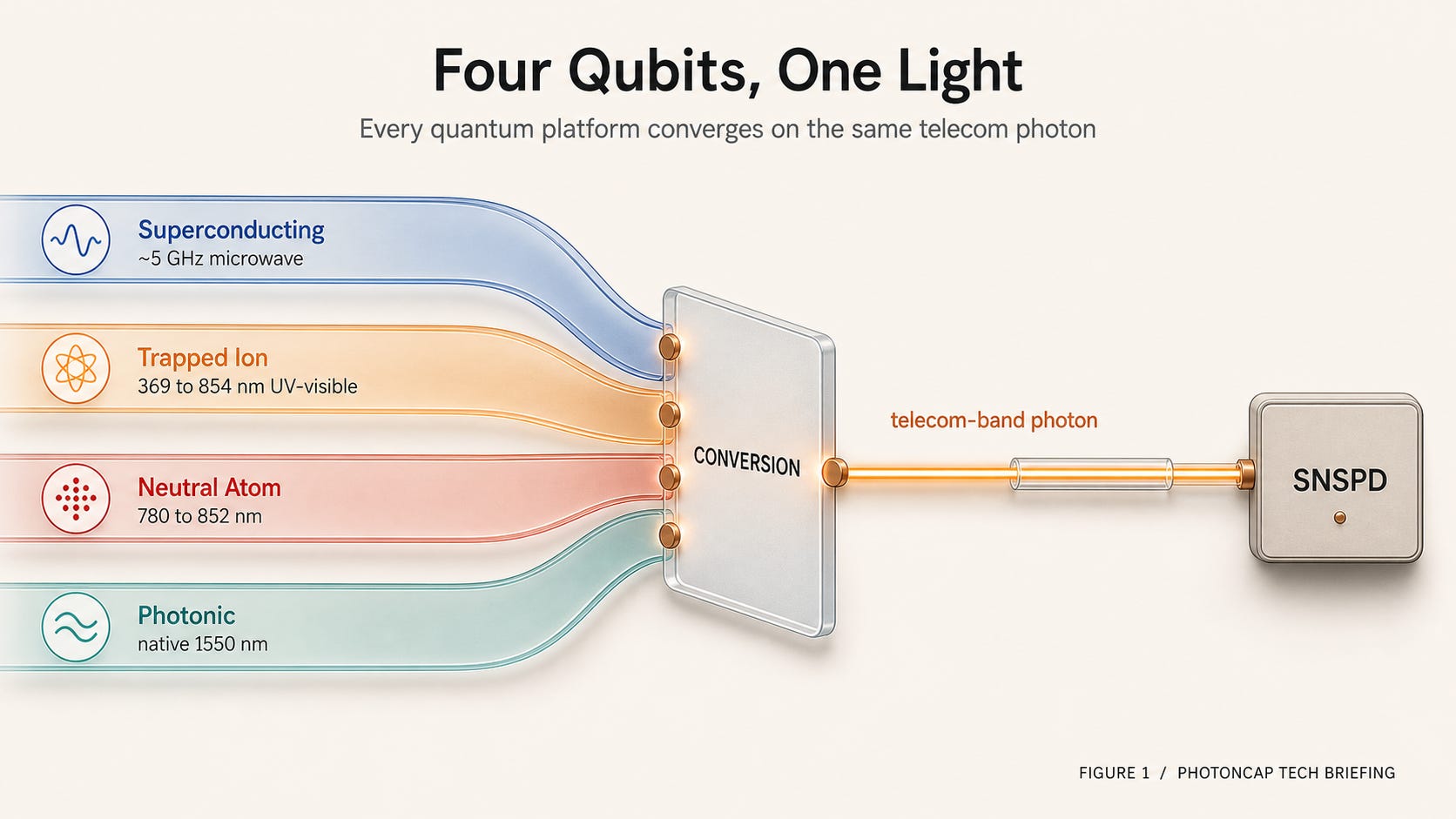

Here is where the crux splits. The light (or signal) a qubit emits is not in the telecom band. Ions emit ultraviolet and visible light, and a superconducting qubit emits not light at all but microwaves. So every platform needs a step that translates its own signal into a telecom photon. This is the heart of the optical interconnect stack.

[Figure 1: Funnel diagram showing the signals from all four platforms converging on a telecom photon]

To summarize, the optical interconnect stack is four layers. The light source (laser) that makes light, the conversion that turns the qubit signal into a telecom photon, fiber transport and routing, and the detection that catches the single photon on arrival. All four platforms have to pass through these four layers.

Qubits come in four families, but the signal leaving the rack converges on a telecom band photon in the end. The difference is whether it reaches C-band 1550 nm or stops at O-band or near-telecom, and how much that conversion costs.

Here Is the Real Question

So far this is a picture you can draw from public material alone. There are four platforms, all need optical interconnect, and the light gathers around telecom. That far.

But what an investor really wants to know is what comes next. The way the four platforms convert to light is not the same. For some the conversion is nearly free, and some carry a problem hard by orders of magnitude, with conversion efficiency still stuck at tens of percent. Different conversion difficulty means a difference in which layer makes the money and who holds that layer.

On top of that, this convergence does not happen only in components. As we will see, the people leading the non-photonic platforms are themselves photonics people, and they are gathering toward optical interconnect as if by agreement. This may be a deeper signal than the market’s M&A.

Beyond that, we also pin down who actually fabs these photonic chips. The manufacturing layer is already the territory of listed companies, and a place that national money has flowed into.

Below we walk through the four layers of light source, conversion, transport, and detection in turn, laying out what materials and equipment each layer uses, which companies stand at the chokepoint, and how both components and people gather toward the same place.

Pricing update — effective June 3, 2026

PhotonCap started with a simple bet: that there’s demand for silicon photonics research that goes deeper than press releases and earnings recaps.

That bet has paid off.

PhotonCap has grown to well over a thousand paid subscribers and ranks #23 on the Substack Top Bestseller list. I’m grateful that this publication is now trusted not only by individual investors, but by institutional investors, hedge funds, and sell-side analysts — as well as fellow research publications including Citrini Research, FundaAI, ChipStrat, Vik’s Newsletter, and Jason’s Chip, who subscribe as paid members.

New pricing — effective June 3:

Monthly: $50/month (currently $30)

Annual: $500/year (currently $300)

Already a paid subscriber? Your rate is locked in permanently. Nothing changes for you.

If you’ve been considering subscribing, now is the time. Lock in the current rate before June 3.

Content offerings, format, and frequency may evolve over time as PhotonCap grows.

— PhotonCap