The Real Quantum Race: NVIDIA, NQI, and China’s State Capital

US $200M, China $140B. The asymmetric position that Ising creates in between.

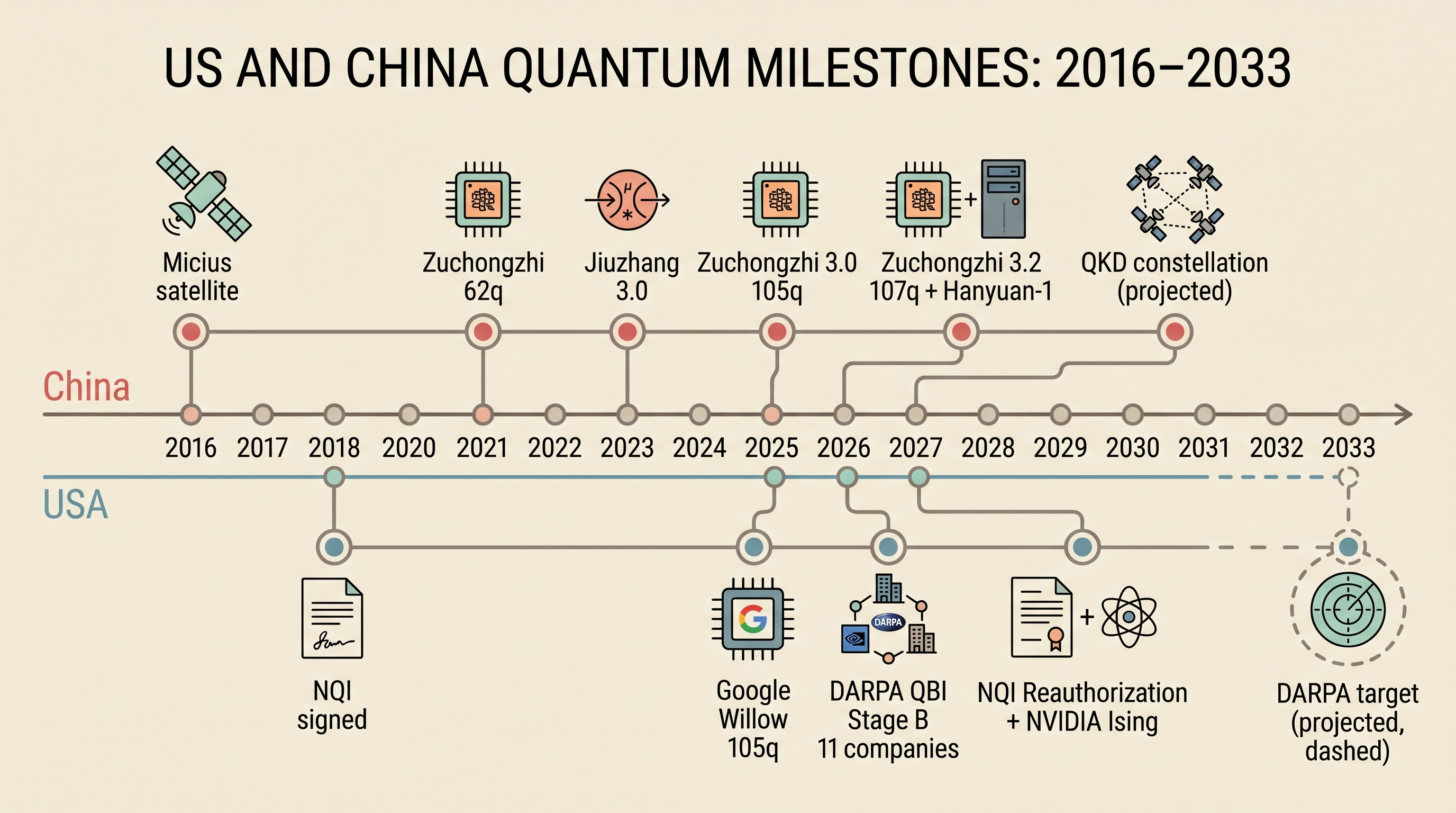

As of April 2026, quantum computing has moved beyond the laboratory and into the arena of national strategic competition. NVIDIA announced its quantum AI model Ising on April 14, and the US Senate Commerce Committee advanced the NQI (National Quantum Initiative) Reauthorization Act on April 14. DARPA’s QBI (Quantum Benchmarking Initiative) has moved 11 companies to Stage B, and the White House is drafting a quantum executive order. On the other side, China has designated quantum technology in its 15th Five-Year Plan, and is targeting a 4-satellite QKD constellation for operational deployment in 2026 following the Micius satellite. This article reframes the US-China quantum competition through an investment lens.

Contents

Intro: NVIDIA Ising and “AI as the Operating System of Quantum Machines”

Background: Where Quantum Computing Actually Stands

The Three Pillars of US Quantum Strategy (NQI + DARPA QBI + White House EO)

China’s Quantum Strategy: From Micius to Zuchongzhi 3.2

DARPA QBI Stage B: 11 Companies + US2QC Comparison (paid)

US vs China Quantum Tech: Architecture-by-Architecture Comparison (paid)

Investment Insights (paid)

Closing

References & Sources

1. Intro

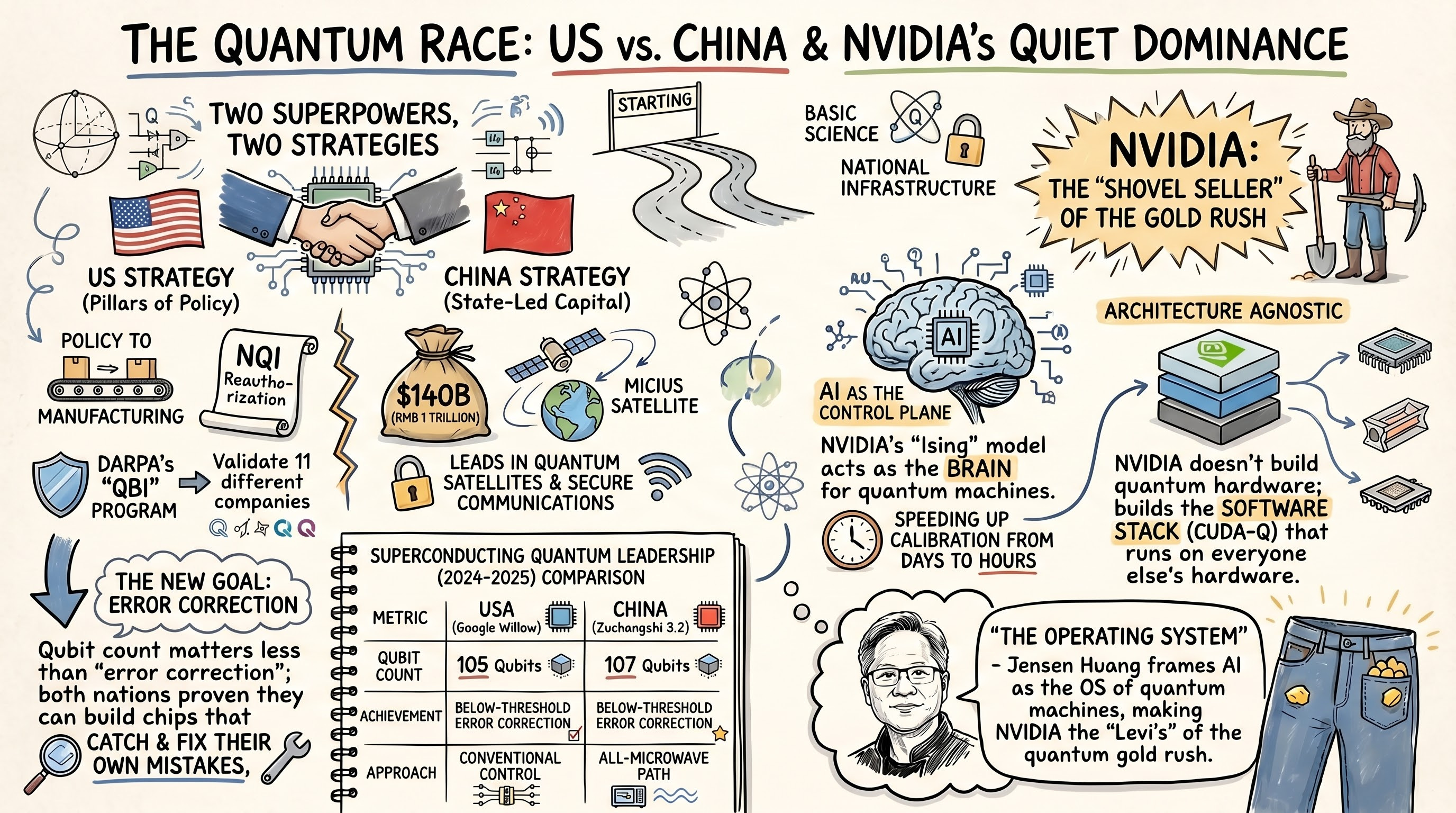

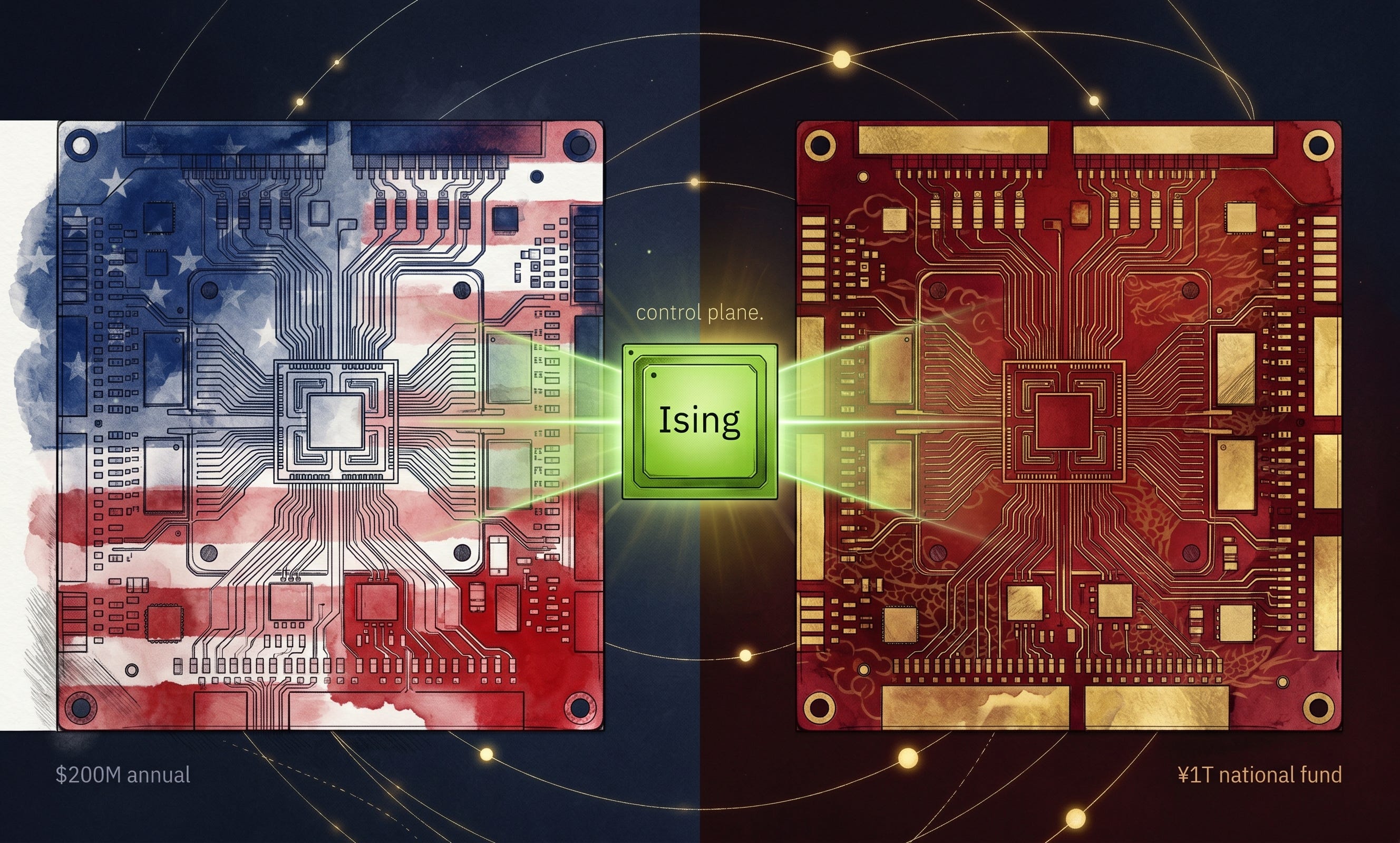

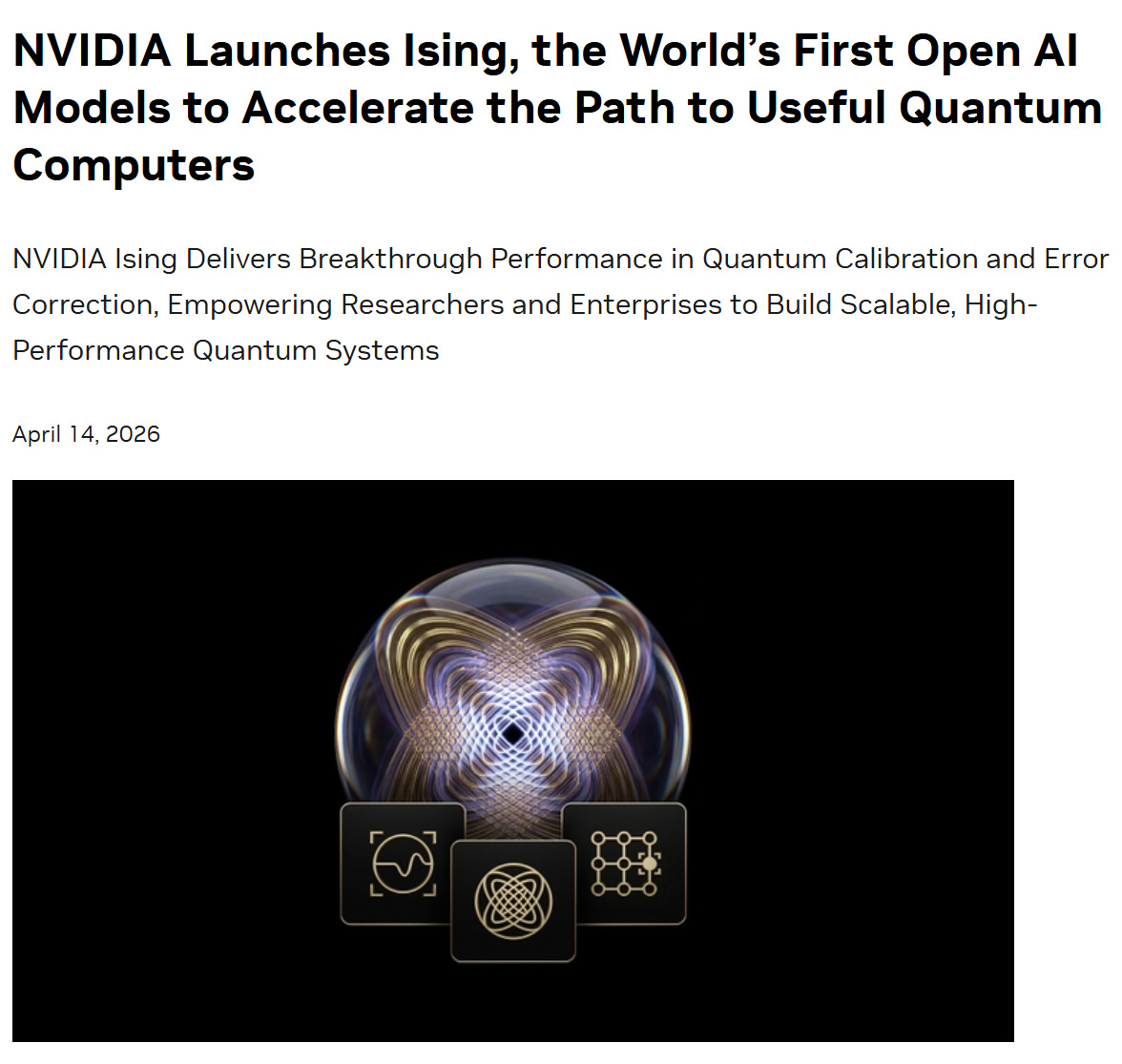

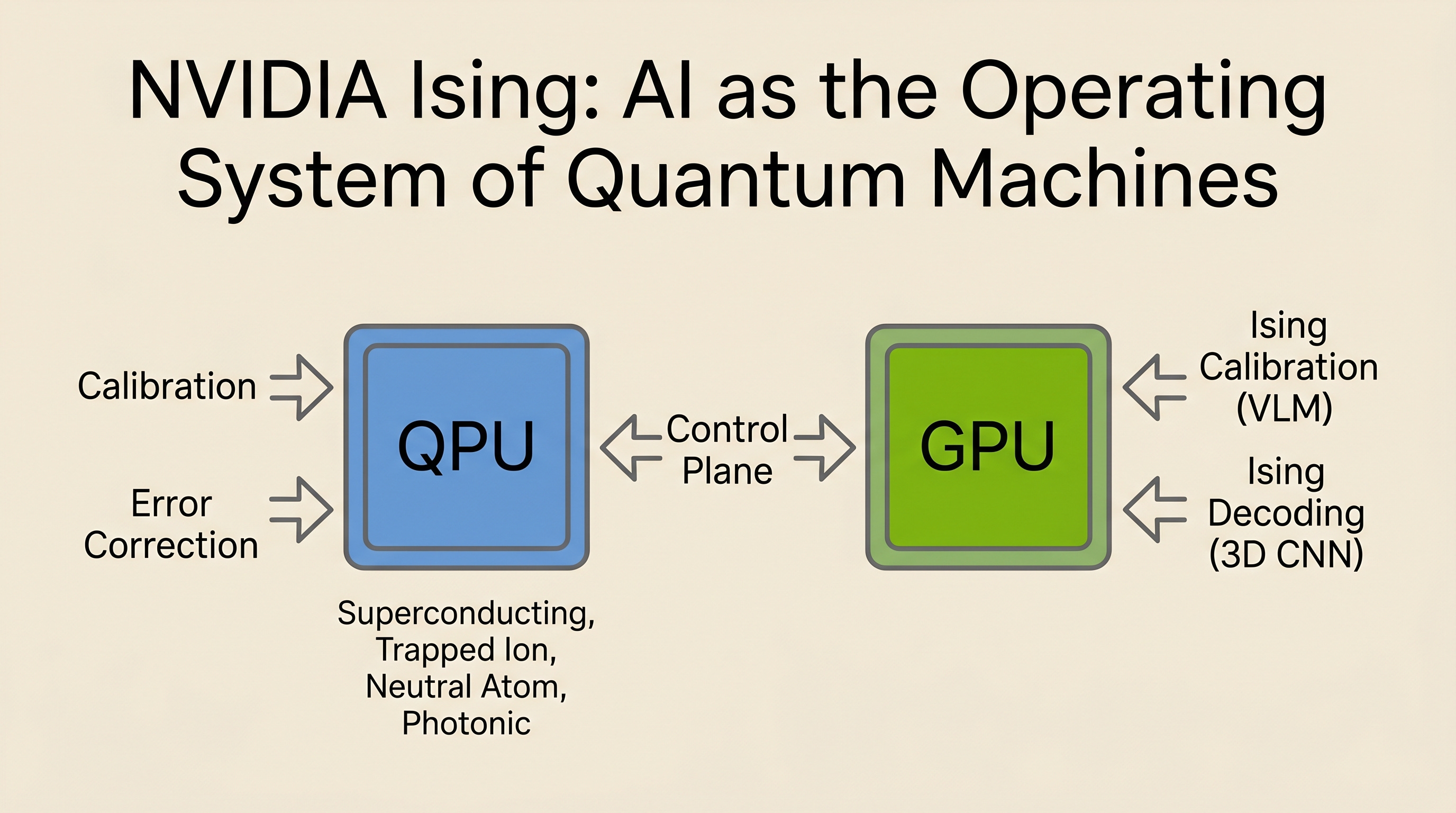

While Washington and Beijing traded national-strategy announcements this week, NVIDIA quietly moved to make every quantum computer on Earth its customer. On April 14, NVIDIA released an open-source AI model family for quantum computing called “Ising.”[1] On the same day, the US Senate Commerce Committee advanced the NQI Reauthorization Act with seven amendments.[2] The timing is not coincidence. Regardless of which qubit architecture eventually wins, if GPUs become the standard at the error correction and calibration layer, the winner of the quantum race is not the hardware maker. It is whoever owns the control plane. This article confronts that structure directly.

Jensen Huang’s framing was striking. AI becomes the “control plane” of quantum machines. In his words: “AI becomes the control plane... the operating system of quantum machines.”[1] This is not just marketing. According to NVIDIA, QPU calibration goes from days to hours, and QEC decoding gets 2.5x faster and 3x more accurate than pyMatching, the current open-source standard.[1]

The NQI Reauthorization Act advanced on the same day includes a dedicated Manufacturing USA Institute for quantum manufacturing, a public-private “Quantum Sandbox” for near-term quantum application development, and a national strategy for post-quantum cryptography (PQC) migration.[2] In a single week, the US redefined quantum computing as a national strategic industry backed by federal budgets, industrial policy, and state-directed capital.

In a previous article, we analyzed Google Quantum AI’s cryptocurrency quantum vulnerability whitepaper.[3] This article extends that work, zooming out from individual companies to the national-level strategic competition. On the US side, we cover three pillars: NQI, DARPA QBI, and the White House executive order draft. On the China side, we trace the technology arc from Micius to Zuchongzhi 3.2 and the 15th Five-Year Plan. The thesis of this piece is that the real winner of this national competition does not live at the hardware layer.

Key takeaway: NVIDIA Ising and NQI Reauthorization landed in the same week. Quantum computing is shifting from “basic science” to “national infrastructure.” And the layer that monetizes first in this structure is not the qubit.

2. Background: Where Quantum Computing Actually Stands

A one-sentence explanation: while classical computers process 0s and 1s one at a time, quantum computers can process 0 and 1 simultaneously. Think of a classical computer navigating a maze by trying one path at a time, while a quantum computer explores all paths at once. That is the theoretical promise. Making it work in practice is a different story.

The key is not qubit count but error rate. Here is an analogy for where quantum computers stand in 2026. Imagine a calculator that gives you the wrong answer 3 to 5 times out of every 100 button presses. Would you file your taxes with it? That is why quantum error correction (QEC) matters. It bundles multiple physical qubits into a single “logical qubit” and catches errors in real time.

The real question is not how many qubits you have. It is whether you have crossed the error correction “threshold.”

In December 2024, Google published results in Nature showing that its Willow chip (105 qubits) achieved exponentially decreasing error rates as more qubits were added, demonstrating “below threshold” performance.[4] This was a goal that the field had considered theoretically possible but practically elusive for years.

About a year later, in December 2025, China’s Zuchongzhi 3.2 (107 qubits) achieved below-threshold error correction at surface code distance 7, publishing the results in Physical Review Letters.[5] The error-suppression factor was 1.4, published as an Editors’ Suggestion in Physical Review Letters.[5] This is in the same ballpark as Google’s Willow, though independent replication has not yet been reported.

On market size, the quantum computing market stood at $1.8B to $3.5B in 2025,[6] and is projected to exceed $11B by 2030 (analyst firm Resonance estimate, as cited in NVIDIA’s press release).[1] According to a March 2026 GAO report, federal agencies collectively spend about $200M per year on quantum computing. Total QIS spending across all agencies is approximately $1B per year.[7] China’s national venture fund reportedly committed RMB 1 trillion (approximately $140B) to quantum technology,[6][8] although this is a total allocation (not annual spending) covering all of quantum technology (computing + communications + sensing). Accounting conventions, timeframes, and scope differ enough between the two countries that dollar-for-dollar comparison runs into real limits. What is clear is that China is allocating state-directed capital systematically, while the US is layering federal budgets on top of a corporate-driven ecosystem.

But the central claim of this article is not about the total dollars on either side. In both countries, the company that captures the control plane, not the qubit hardware, is positioned to monetize first. The reasoning for that claim, with the CUDA-Q / NVQLink / Ising stack broken down piece by piece, sits in the paid section below. First, the strategic structures on each side.

Key takeaway: The qubit count race is becoming less meaningful. Crossing the error correction threshold is the real benchmark. Both the US and China crossed that line in 2024-2025. And the layer that monetizes first in this competition is not the qubit hardware on either side.

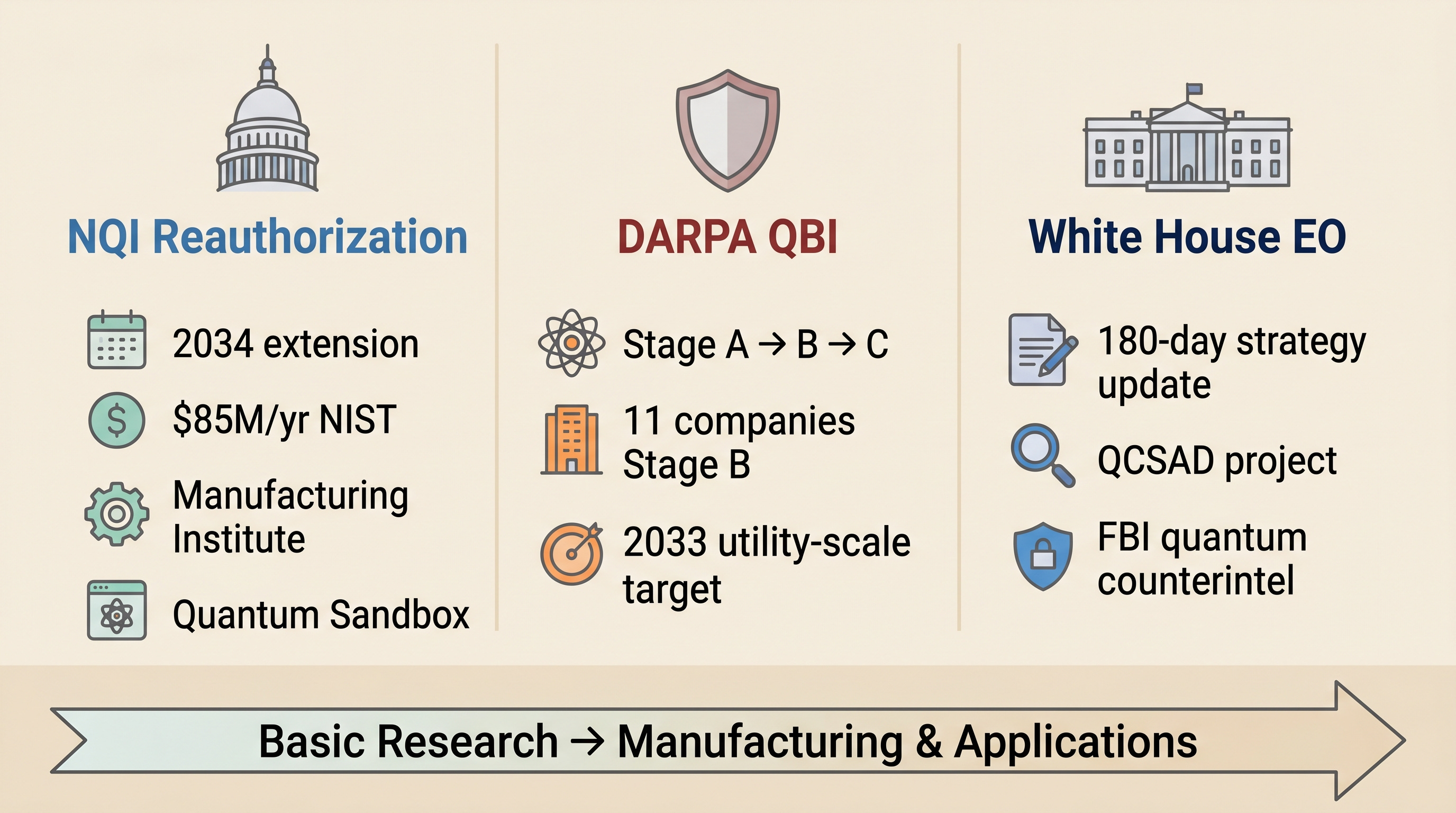

3. The Three Pillars of US Quantum Strategy

The US quantum strategy rests on three pillars: NQI Reauthorization in Congress, DARPA’s QBI benchmarking program, and a White House executive order draft. Each operates on a different timeline and targets a different objective.

3-1. NQI Reauthorization: Extended to 2034, Shifting from Research to Manufacturing

The NQI (National Quantum Initiative) was signed into law during Trump’s first term in 2018. It provided a federal framework for coordinating quantum R&D, but its authorization of appropriations expired in 2023.[9] Without congressional reauthorization, the legal foundation had been shaking.

In January 2026, Senators Todd Young (R-IN) and Maria Cantwell (D-WA) introduced a bipartisan reauthorization bill.[10]

The bill extends the NQI program timeline to December 2034, with appropriations authorized for FY2026-2030. It allocates $85M per year (FY2026-2030) to NIST and $25M per year to NASA, and establishes up to three new NIST quantum centers focused on sensing, measurement, and engineering.[11] For the first time, NASA is formally authorized to conduct quantum satellite communications and quantum sensing R&D.[10]

The version that advanced through the Senate Commerce Committee yesterday (April 14) includes seven amendments, three of which stand out.[2]

First, it creates a dedicated Manufacturing USA Institute for quantum manufacturing, improving coordination between DOE and NSF and defining the industrial capabilities needed for quantum system production.[2] Second, it establishes a public-private “Quantum Sandbox” to accelerate near-term quantum application development.[2] Third, it directs a national strategy for post-quantum cryptography migration.[2]

The important point here is that NQI’s center of gravity is shifting from “basic research” to “manufacturing and applications.” The 2018 bill was driven by the fear of falling behind. The 2026 reauthorization is answering a fundamentally different question: how to get from the lab to the factory floor.

3-2. DARPA QBI: “Can We Build a Useful Quantum Computer by 2033?”

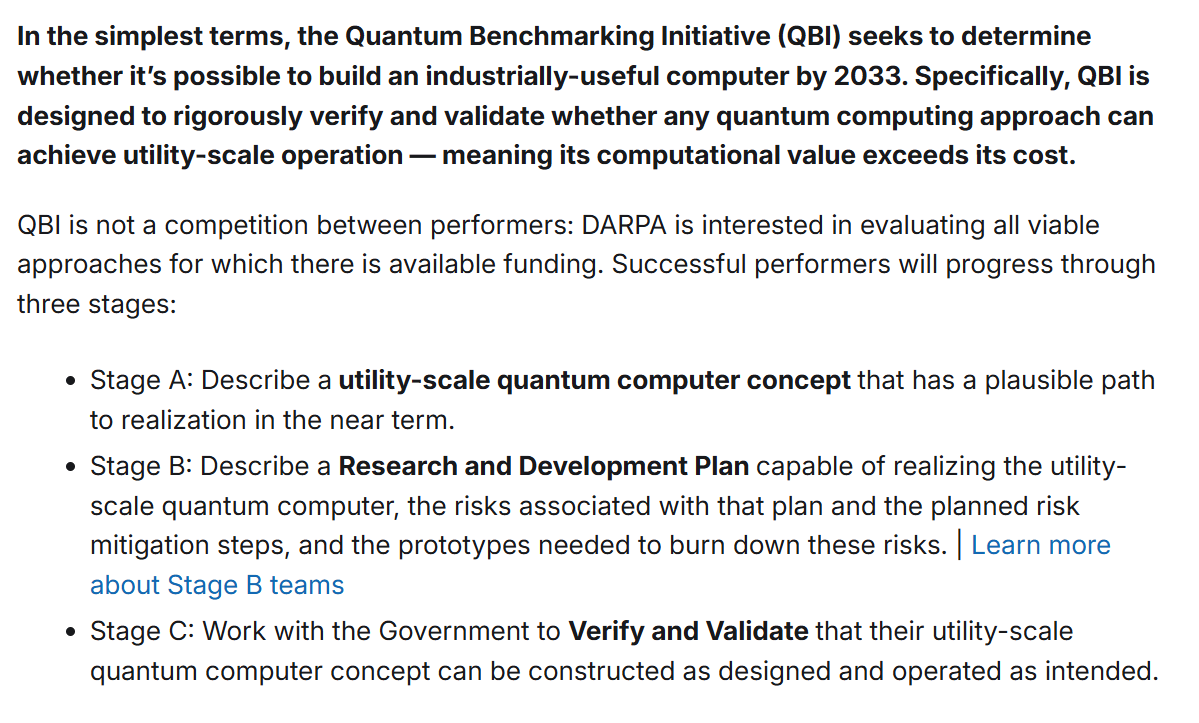

DARPA’s QBI (Quantum Benchmarking Initiative) asks a blunt question. Regardless of quantum computing approach, can a utility-scale quantum computer, one whose computational value exceeds its cost, be built by 2033?[12]

QBI has three stages.[12]

In Stage A, companies describe their utility-scale quantum computer concepts. In Stage B (approximately one year), DARPA conducts deep reviews of their R&D plans, risk mitigation strategies, and prototype roadmaps. In Stage C, a government verification and validation team tests actual hardware against benchmarks.[12]

As of November 2025, 11 companies have advanced to Stage B.[13] Atom Computing (neutral atoms), Diraq (silicon spin), IBM (superconducting), IonQ (trapped ion), Nord Quantique (bosonic error correction), Photonic Inc. (silicon spin), Quantinuum (trapped ion), Quantum Motion (silicon spin), QuEra (neutral atoms), Silicon Quantum Computing (atom qubits in silicon), and Xanadu (photonic).[13]

Separately, Microsoft and PsiQuantum are participating in the final stage of the US2QC (Underexplored Systems for Utility-Scale Quantum Computing) program, which preceded QBI.[14] The final stage of US2QC shares the same technical objectives as QBI Stage C.[14]

DARPA has been explicit that this is not a competition to pick winners. “Multiple, single, or even no participants will ultimately demonstrate a path to an industrially useful quantum computer.”[12] Multiple companies may succeed, a single one may, or none at all. That is an honest framing.

The real question investors should be asking is not which 11 companies advanced to Stage B, but which of them have a credible path through Stage C. In our view, the list of genuine survivors is closer to 3 or 4, not 11. The architecture-by-architecture case, and the reasoning behind that shorter list, is laid out in Section 5.

3-3. White House Executive Order Draft: QCSAD and FBI Quantum Counterintelligence

In February 2026, Nextgov/FCW reported that the White House is drafting an executive order to restructure US quantum policy.[15] The order has not yet been signed, so final provisions may change.

The draft directs OSTP (Office of Science and Technology Policy), the Departments of Commerce, Energy, and Defense to update the national quantum strategy within 180 days of signing.[15] Agencies would then have 30 days after the strategy is released to submit implementation plans.[15]

One notable element is “QCSAD,” a new national project to build a Quantum Computer for Scientific Applications and Discovery at a DOE facility.[15]

On the security side, the FBI would expand its QIST Counterintelligence Protection Team, and ODNI (Office of the Director of National Intelligence) would coordinate budgets and resources for protecting quantum research.[15]

A GAO report released in March 2026 identified weaknesses in the current national quantum strategy: no performance measures, no specification of required infrastructure levels, and unclear agency roles and responsibilities.[7] The Trump administration’s FY2026 budget request maintained quantum research spending at existing levels but included no new programs or workforce development investments.[16] DOE, however, separately allocated $625M over five years to renew five National QIS Research Centers in November 2025.[17] The executive order appears designed to coordinate these fragmented efforts.

From an investment perspective, there is one question that matters: which layer of this structure generates revenue first? Before answering that, we need to look at the other side.

Key takeaway: US quantum strategy operates on three axes: NQI (legislation), DARPA QBI (technical validation), and White House EO (policy coordination). The common direction is the shift from basic research to manufacturing and applications.

4. China’s Quantum Strategy: From Micius to Zuchongzhi 3.2

To understand China’s quantum strategy, we need to go back to 2016.

4-1. Micius: The 21st Century Sputnik

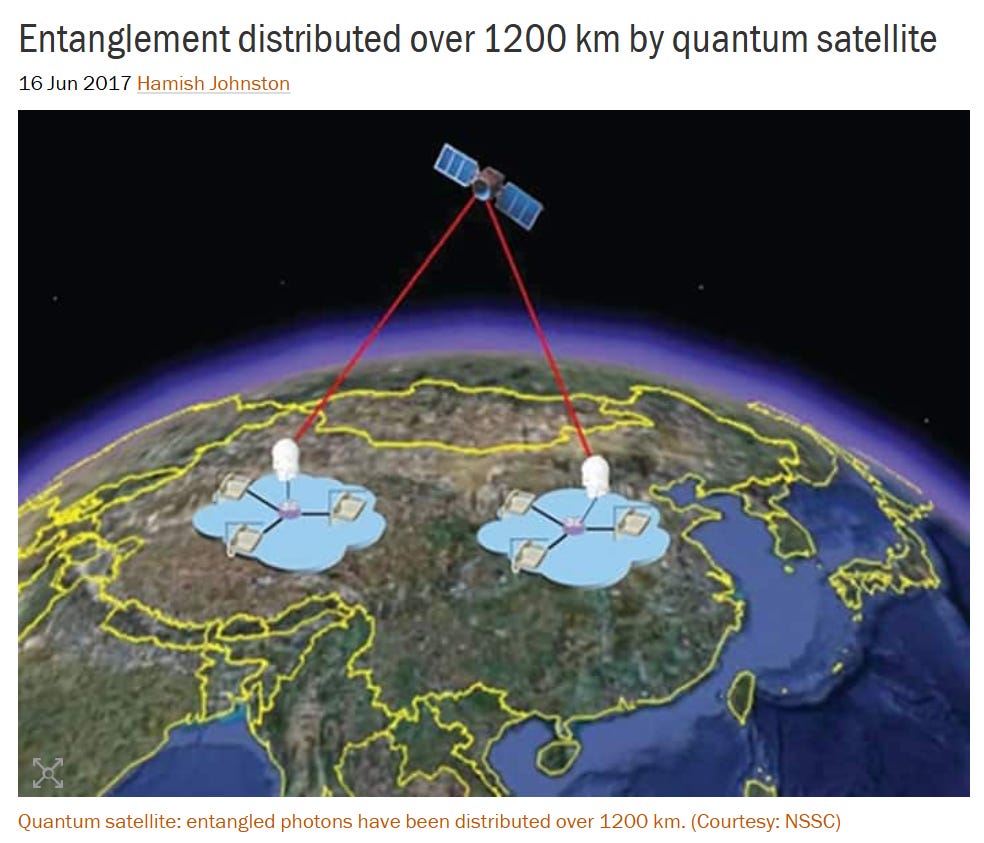

In August 2016, China launched the world’s first quantum science satellite, Micius.[18] Named after the ancient Chinese philosopher Mozi, the satellite successfully generated entangled photon pairs in orbit and transmitted them to two ground stations 1,200 km apart.[18]

Why does this matter? Quantum communication over optical fiber is limited to a few hundred kilometers because the fiber absorbs photons. But from space to ground, most of the path is vacuum, meaning virtually zero loss.[18] Micius was the first satellite to demonstrate this principle.

Setsuko Aoki, a space policy expert at Keio University in Japan, called it “the 21st century’s Sputnik moment.”[19] Just as the Soviet Sputnik shocked the United States in 1957, Micius showed that China had overtaken the US in the cutting-edge field of quantum communications.

In 2017, Micius enabled the world’s first quantum-encrypted video conference between Beijing and Vienna over a distance of 7,500 km, though this used a trusted-relay method where the satellite itself held the quantum keys. In 2020, the team took it a step further, demonstrating entanglement-based QKD (quantum key distribution) over 1,200 km for the first time, a method where even the satellite does not know the keys.[20] Then in March 2025, the quantum microsatellite Jinan-1 demonstrated real-time QKD between China and South Africa over approximately 12,900 km, published in Nature.[21] GQI (Global Quantum Intelligence) projects that China plans to deploy a constellation of four LEO QKD satellites in 2026.[22]

4-2. Quantum Computing: Superconducting, Photonic, and Neutral Atoms

If China leads in quantum communications, where does it stand in quantum computing?

Pan Jianwei’s team at USTC (University of Science and Technology of China) is pushing three tracks simultaneously.

First, the superconducting Zuchongzhi series. Starting at 62 qubits in 2021, it expanded to 105 qubits (version 3.0) in 2024 and 107 qubits (version 3.2) in 2025.[5][8] Zuchongzhi 3.2 achieved below-threshold error correction using an “all-microwave quantum state leakage suppression architecture,” a distinct approach from Google’s method.[5]

Second, the photonic Jiuzhang series, which specializes in Gaussian boson sampling. Jiuzhang 3.0 solved a specific sampling problem in one microsecond in 2023.[23] It should be noted, however, that this is a different track from universal quantum computing.

Third, the neutral-atom quantum computer Hanyuan-1, a 100-qubit system that began commercial deployment in October 2025.[8] This puts it in direct competition with US companies like QuEra and Infleqtion.

On the industrial ecosystem side, Origin Quantum stands out. Its 72-qubit superconducting processor Origin Wukong launched commercially in 2024 and has been rapidly expanding its global cloud user base.[8] China Telecom Quantum Group operates the Tianyan quantum cloud platform, hosting an 880-qubit superconducting cluster and serving users from over 60 countries.[24]

4-3. National Strategy: The 15th Five-Year Plan and RMB 1 Trillion

China’s government designated quantum technology as one of seven emerging industries in its 15th Five-Year Plan (2026-2030). “Promote cutting-edge industries such as quantum technology to become new economic growth points.”[23] If the 14th Plan was about catching up, the 15th is about leading.

In January 2025, the Ministry of Industry and Information Technology (MIIT) issued open-competition tasks for the quantum sector, including a target to build quantum measurement and control systems capable of supporting at least 1,000 qubits, with measurement-based feedback latency of under 1 microsecond, by 2026.[25]

In terms of investment scale, China’s national venture fund reportedly committed RMB 1 trillion (approximately $140B) to quantum technology.[6][8] Compared to the US federal government’s annual QIS spending of about $1B, this is a multi-order-of-magnitude difference. However, this is a total fund allocation covering all of quantum technology (computing + communications + sensing), and actual annual disbursement and distribution are difficult to verify.

The quietest observation from the past 12 months is this. First, Microsoft’s topological qubit claim has been walked back, effectively, by Nature’s own editors in the peer-review file attached to the companion paper. Second, NVIDIA open-sourced Ising while simultaneously locking the entire control-plane layer into its proprietary stack through CUDA-Q and NVQLink. Third, the academic frontier of neutral-atom quantum computing (Lukin, Vuletić, Greiner) is concentrated inside a single private company, QuEra. These three threads decide who actually survives DARPA QBI Stage C. The architecture-by-architecture case, the specific companies, and the reasoning are laid out below.

Key takeaway: China leads in quantum communications but is pursuing superconducting, photonic, and neutral-atom quantum computing on three parallel tracks. The investment numbers are large, but technology quality is a separate question. And the true layering of that quality sits behind the paywall.