America Needs to Cut Chinese Germanium: Why Loss-Making IR Optics Company LPTH Trades at P/S 16x

$LPTH | LightPath Technologies Deep Dive

LightPath Technologies ($LPTH), an Orlando-based IR optics company with $50.6M in revenue over the first nine months of FY26 (Jul 2025 to Mar 2026) and ongoing net losses, is trading near a $1B market cap. FY26 Q3 standalone revenue was $19.1M (YoY +109%), with backlog at $110.6M (+196%). The investment thesis here is that supply chain regulation and material substitution are pushing in the same direction: in the U.S. defense IR optics market, where dependence on Chinese-dominated germanium must be unwound, a domestically integrated chalcogenide glass producer commands a procurement eligibility premium. This article covers a material property comparison based on SPIE paper data, the regulatory drivers from NDAA Sections 834/844, and the competitive landscape.

Table of Contents

Why I Started Looking at This Stock

The Germanium Problem: Why Now

The Alternative Material: Chalcogenide Glass and What the SPIE Paper Shows

LightPath Technologies: Company Anatomy (Products, NRL License, M&A, Lockheed Martin Program)

Financials: Fast Growth, Unproven Profitability

Competitive Landscape: Not a Monopoly

Bull Case, Gap, Optionality

Valuation: Three Futures That a $1B Market Cap Demands

Scenario Framework 10. Monitoring Checklist

1. Why I Started Looking at This Stock

A company with $50.6M in FY26 nine-month revenue carries a $1B market cap. It is still losing money.

One of the most dramatic stock moves in the photonics sector this year was $AAOI (Applied Optoelectronics). It ran from a 52-week low near $15 to an intraday high of $233. AAOI is not a large platform company that dominates optical materials, lasers, and modules the way Lumentum or Coherent does. What the market bought was “a rare supply chain position: U.S.-anchored vertical integration from laser chips and subassemblies in Sugar Land, Texas to high-speed optical modules, with expanding AI datacenter transceiver capacity.” The onshoring premium kicked in across the AI datacenter supply chain.

I saw a similar structure in $LPTH. The sector is different. AAOI is datacenter optical interconnect. LPTH is defense IR optics. Both are vertically integrated in the U.S., and both are receiving multiples based on supply chain positioning rather than platform dominance. That said, AAOI is already at a $600M+ total revenue run-rate with Q1 2026 datacenter revenue of $81.4M, while LPTH is still at $67M annualized with defense backlog conversion yet to be proven. The comparison has its limits in scale and visibility.

I like doing DD on small-cap tech stocks. Holding $POET and $LWLG, I have seen firsthand that photonics small caps can work when the technology fits the cycle. I have been looking for the next one, and $LPTH caught my eye while I was building a defense sensor investment map.

[Investment Map] When War Drags On, Sensors Make the Money

![[Investment Map] When War Drags On, Sensors Make the Money](https://substackcdn.com/image/fetch/$s_!jmWf!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fa14e0f1e-8249-49eb-8a7f-d405fe9f4a29_1704x892.png)

On March 3, 2026, while KOSPI crashed 7.24%, LIG Nex1 hit the daily limit up. Hanwha Systems surged +29%, Hanwha Aerospace +20%. But among the names that rallied that day, RFHIC and i3system barely registered on most investors’ radar.

It is an infrared optics company. It makes lenses and camera modules that go into EOIR (Electro-Optical/Infrared) systems: night vision, thermal imaging cameras, missile seekers. My first reaction was honest: “Lenses and mirrors? Isn’t that a commodity?”

Then I thought about ASML. A TWINSCAN DUV scanner costs $100M+, and a significant portion of that price comes from the lens column built by Zeiss. Dozens of SiO₂/CaF₂ glass elements, polished and aligned to nanometer precision. A “glass-cutting company” is one of the most irreplaceable suppliers in the semiconductor industry. ASML’s UV lithography optics and LightPath’s IR thermal optics are completely different in precision, materials, customers, and ASP. But one structural parallel holds: when optical materials and lens assemblies define the performance ceiling of a system, the “glass-cutting company” is not a commodity supplier. It becomes a bottleneck supplier. Detection range, resolution, and focus stability across temperature extremes in a thermal camera all start with the physical properties of the lens material.

$LPTH caught my eye during the defense sensor mapping work precisely because there was an interesting story at the material level. And this is not limited to defense. In AI datacenters, optical interconnects are becoming the key to unlocking power and bandwidth constraints in GPU cluster scaling. In semiconductor manufacturing, ASML/Zeiss optics push the physical limits of advanced nodes. In defense, IR lens materials set the performance ceiling of EOIR systems. The sectors are different, but the common thread is clear. Optics is no longer a peripheral component. It has become a constraint on system architecture.

But the interesting question about this stock is not “Is it a good company?” Good materials, good customers, good regulatory tailwinds are already substantially reflected in the stock price. A $1B market cap on a company with $50M-range nine-month revenue is the evidence. The real question is more uncomfortable. For a company with $50M in FY26 nine-month revenue to sustain a $1B market cap, what has to go right from here?

Simply selling more BlackDiamond lenses is not enough. Backlog has to convert to revenue. Assemblies and modules have to keep climbing as a share of the mix, pushing gross margin toward 40%. Large defense options like the Lockheed Martin program have to turn into actual production revenue. This article is less about “Is LPTH a good company?” and more about “Has the market already gone too far, or is this the beginning of a re-rating into a $1B defense optics platform?”

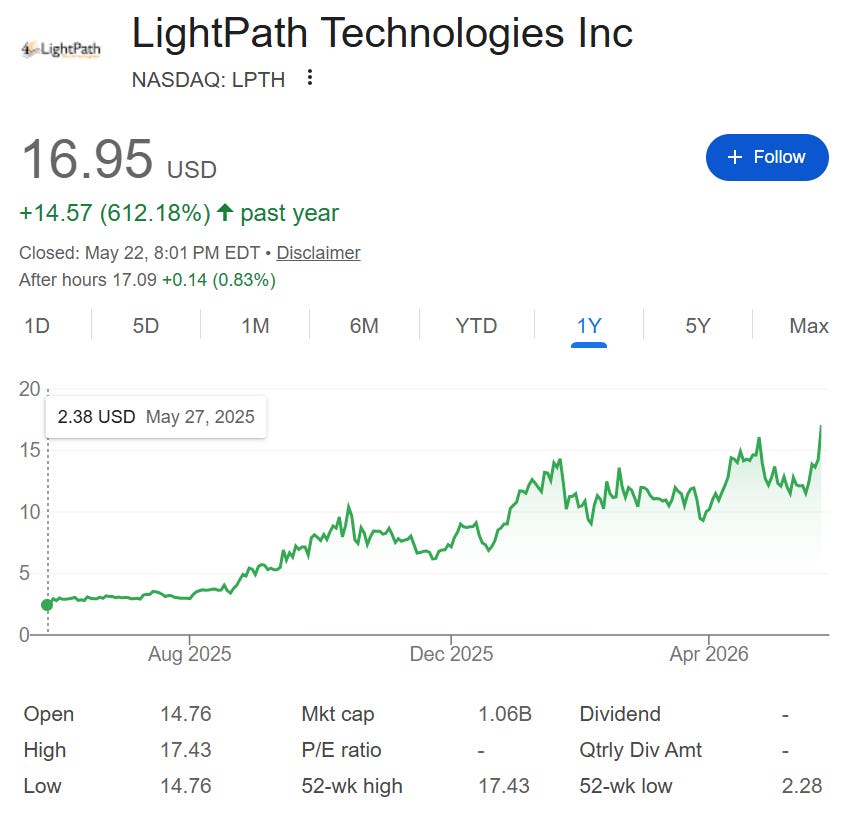

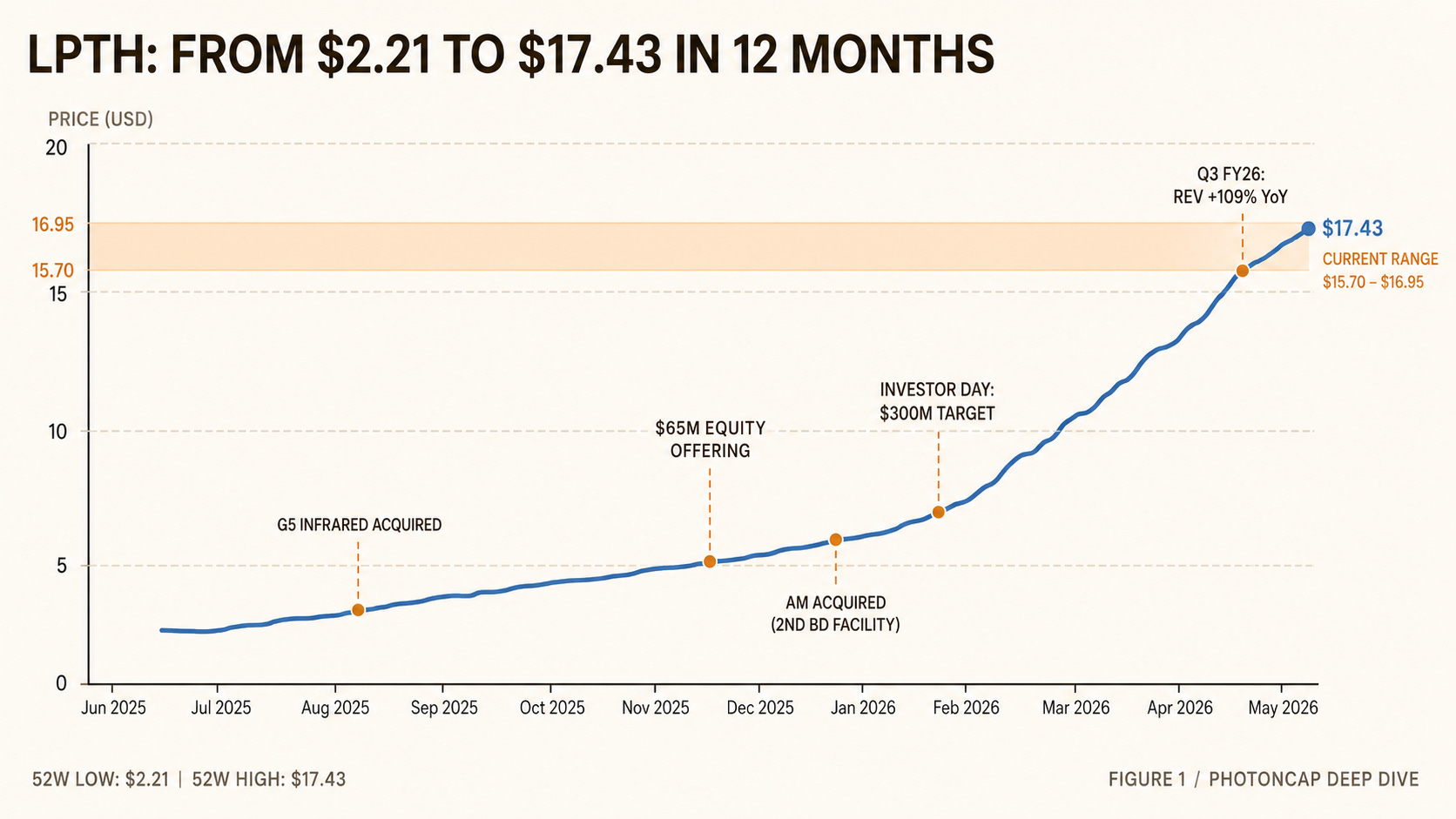

[Figure 1: LPTH Stock Price, 52-Week Range, Key Event Markers]

2. The Germanium Problem: Why Now

The traditional workhorse material for infrared lenses is germanium (Ge). It is a single-crystal semiconductor with strong IR transmission. The problem is who makes it.

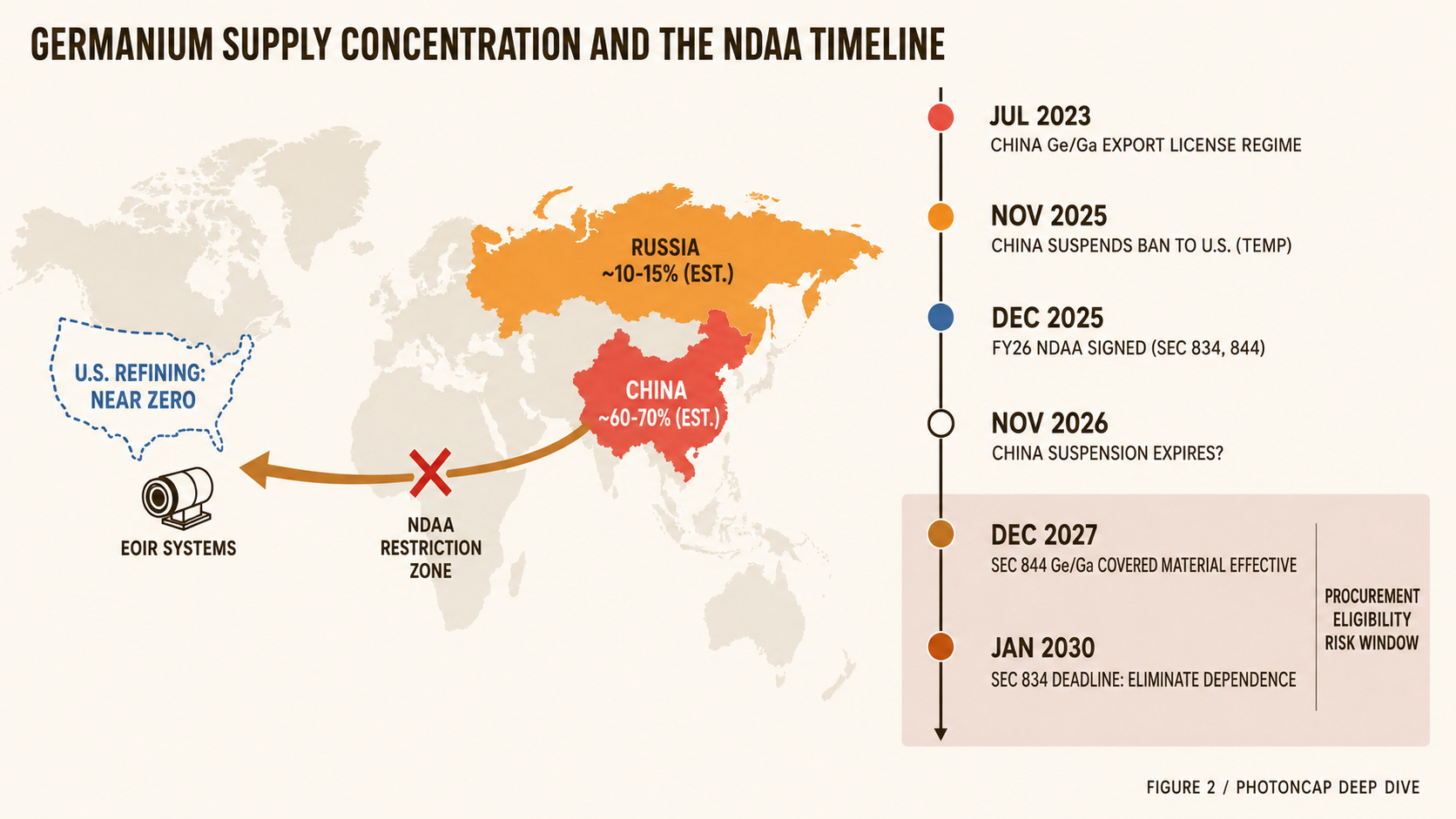

China is estimated to account for roughly 60 to 70% of global germanium refining (USGS does not publish exact shares but describes China as the “leading producer”; independent estimates from Nordic geological surveys put the figure around 68%) [1]. Including Russia, some estimates place the combined share above 80% (based on 2021 data) [2]. The U.S. has virtually no domestic germanium refining infrastructure.

In July 2023, China introduced an export license regime for gallium and germanium [3]. Price spikes and procurement uncertainty hit defense and industrial IR programs worldwide.

Then in December 2025, the FY26 NDAA was signed into law, turning this into a regulatory mandate.

Section 834: Directs the DoD to develop and implement a strategy to eliminate dependence on covered nations (China, Russia, Iran, North Korea, Belarus) for optical glass and optical systems by January 1, 2030 [4].

Section 844: Adds germanium and gallium to the covered material list. The effective date is two years after enactment (December 2025) [5].

These provisions do not impose an immediate ban. They require strategy development and phased implementation. Chinese-sourced Ge lenses are not an overnight “compliance violation.” But over the 2027 to 2030 timeframe, procurement eligibility will be affected, and contract flow-down conditions in defense programs are likely to shift [4].

One more thing to know. In November 2025, China suspended certain export bans on gallium, germanium, and antimony to the U.S. until November 2026 [21]. The investment thesis is therefore closer to “long-term procurement risk created by the license regime and NDAA” than “immediate supply cutoff.” The uncertainty itself, the fact that China can reimpose restrictions at any time, is what motivates material substitution for defense program managers.

The market at stake is significant. The global IR and thermal imaging systems market is estimated at approximately $8B in 2025, projected to reach $10.6 to $11.7B by 2030 at a CAGR of 5.9 to 6.2% [13][14]. Defense accounts for roughly 35% of this, while automotive ADAS is the fastest-growing segment (CAGR 7.7 to 7.9%) [15]. Uncooled LWIR represents 72% of total revenue, and the core optical materials for this segment are germanium and chalcogenide glass [15]. In other words, the germanium supply chain issue touches a multi-billion-dollar market.

Defense EOIR systems have a 5 to 10-year design-to-deployment cycle. With a 2030 deadline, material decisions effectively need to be made now.

Germanium is not a bad material. The problem is that production is concentrated in China and Russia, and the NDAA has legislated a phased elimination of that dependence. This is a long-term procurement risk rather than an immediate ban, but given 5 to 10-year design cycles, the direction is already set.

[Figure 2: Global Germanium Supply Chain + NDAA Regulatory Timeline]

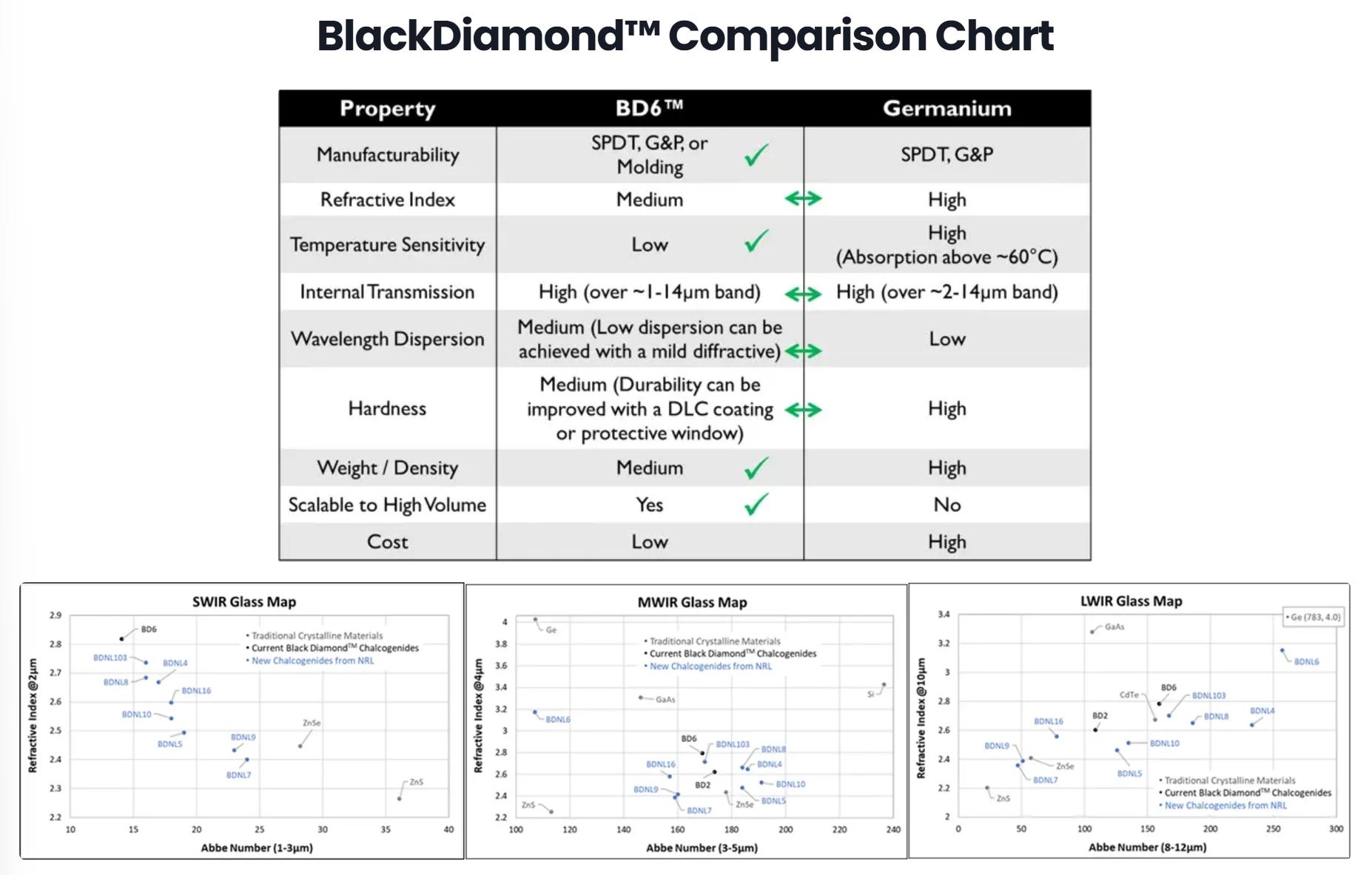

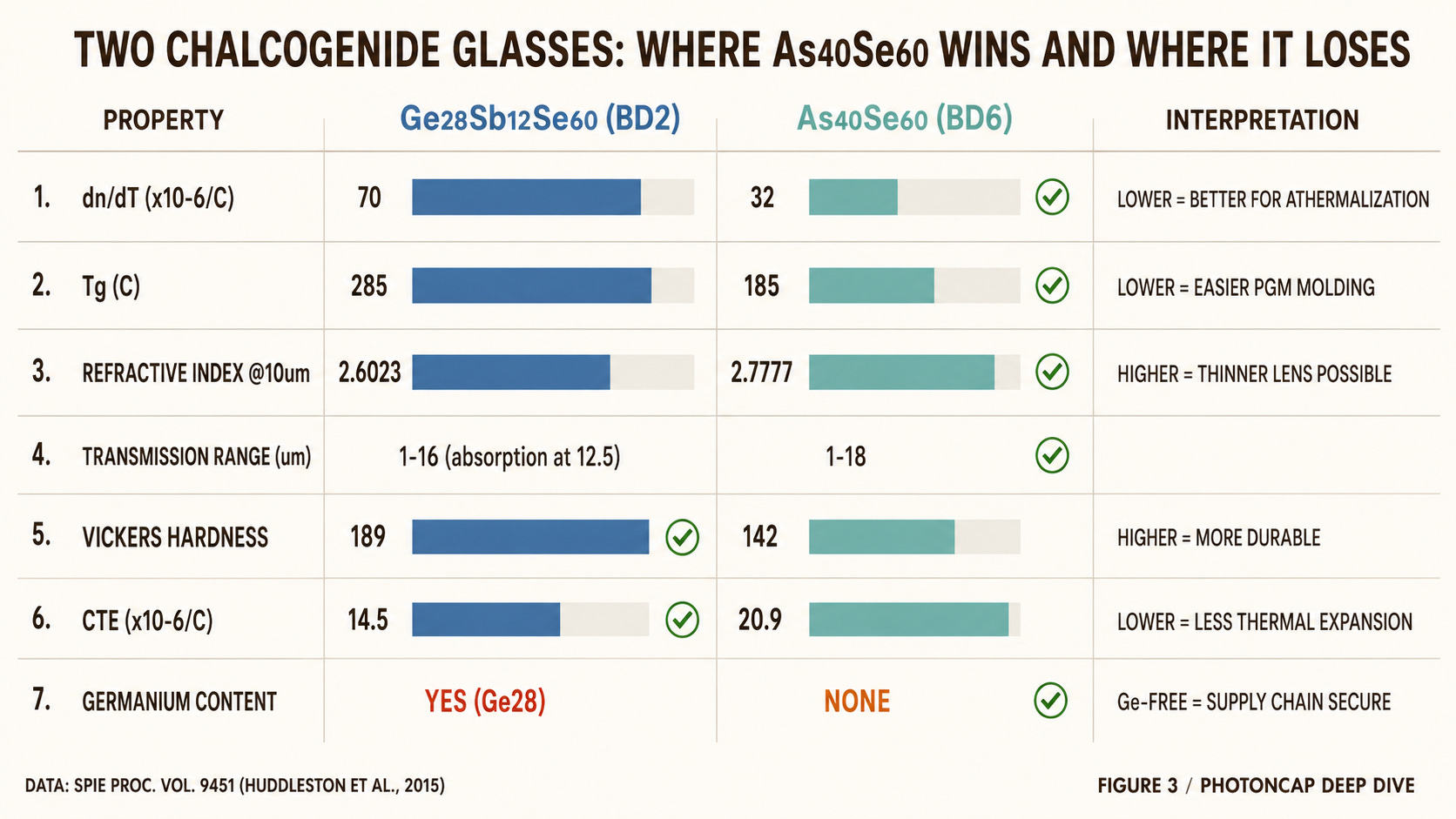

3. The Alternative Material: Chalcogenide Glass and What the SPIE Paper Shows

So what is the alternative? During this DD I found an SPIE conference paper.

“Investigation of As₄₀Se₆₀ chalcogenide glass in precision glass molding for high-volume thermal imaging lenses” (Huddleston, Novak, Moreshead, Symmons, Foote; LightPath Technologies, SPIE Proc. Vol. 9451, 2015) [6]

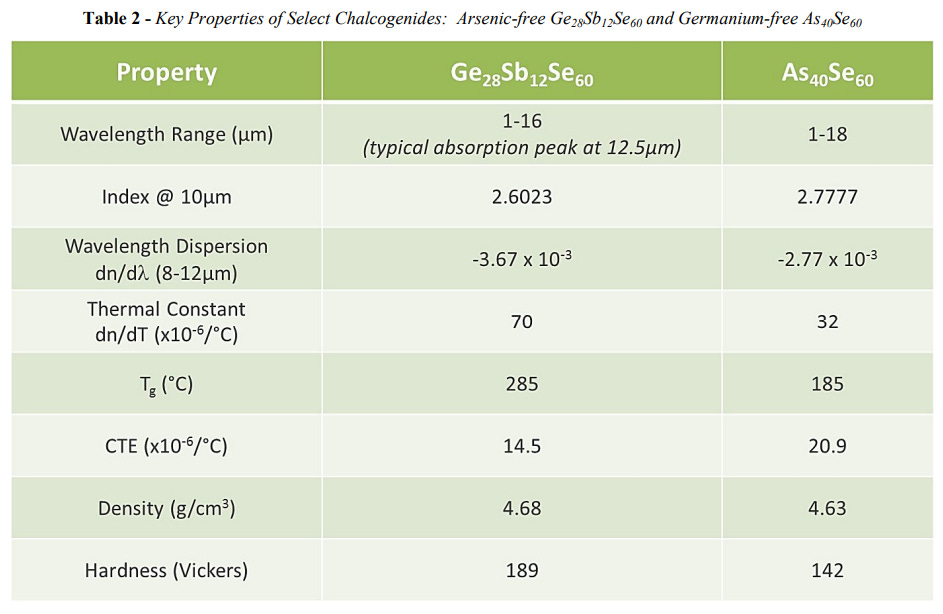

This paper is the key to understanding LightPath’s technical position. It contains head-to-head data comparing the mainstream chalcogenide glass composition Ge₂₈Sb₁₂Se₆₀ (contains germanium) against As₄₀Se₆₀ (germanium-free), which is the composition LightPath is pushing.

Chalcogenide glass is an amorphous glass made from Group 16 elements such as sulfur (S), selenium (Se), and tellurium (Te). Ordinary glass (SiO₂) blocks infrared, but this material transmits IR across the 1 to 18 μm range. It covers both MWIR (3 to 5 μm) and LWIR (8 to 12 μm), the key operating bands for thermal imaging cameras.

Three key differences versus germanium.

3-1. Athermalization: dn/dT

The first number that stands out in Table 2 of the paper is dn/dT, the rate at which refractive index changes with temperature. Ge₂₈Sb₁₂Se₆₀ has a dn/dT of 70 × 10⁻⁶/°C. As₄₀Se₆₀ comes in at 32 × 10⁻⁶/°C. Less than half. For reference, single-crystal germanium has a dn/dT of approximately 396, making As₄₀Se₆₀ roughly 1/12th of that value.

What this means in practice: military thermal cameras must operate from -40°C to +60°C. Germanium lenses shift focus across that range, requiring separate mechanical compensation mechanisms. The low dn/dT of As₄₀Se₆₀ increases the design freedom for passive athermal lens systems and can reduce the need for mechanical focus correction. Whether correction hardware disappears entirely in a real system depends on the optical prescription, housing CTE, and detector package design. But the direction is clear. Design freedom in SWaP-C (Size, Weight, Power, Cost) goes up.

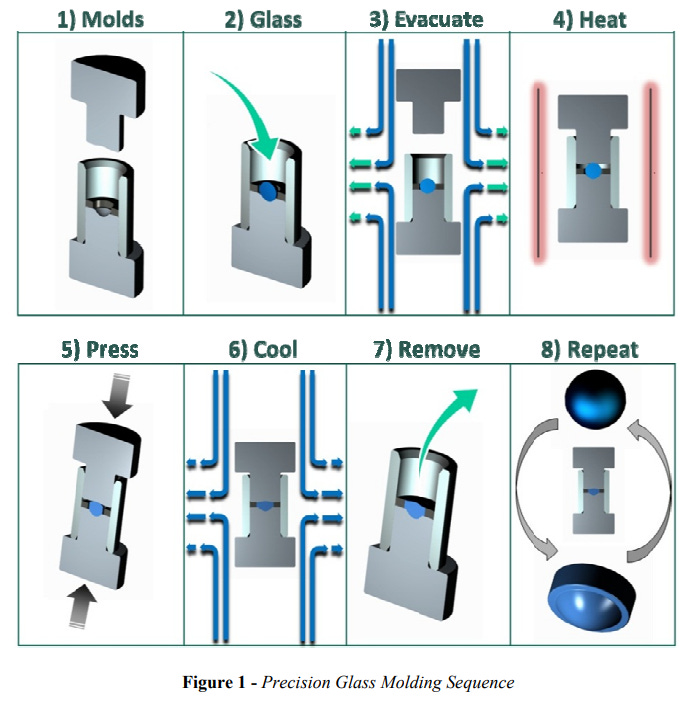

3-2. Precision Glass Molding (PGM): Volume Production

Germanium is a single-crystal material. It has to be shaped one piece at a time using diamond turning. Chalcogenide glass is amorphous. Heat it up and it softens, allowing it to be pressed into a mold. This process is called PGM (Precision Glass Molding).

The glass transition temperature (Tg) of As₄₀Se₆₀ is 185°C, versus 285°C for the Ge-containing composition. A 100-degree difference. Lower molding temperature means less process energy and longer mold life. Complex shapes like aspheric lenses can be molded in a single step. Compared to diamond turning, production cost is inherently lower at the process level.

3-3. Transmission Range and Refractive Index

As₄₀Se₆₀ transmits from 1 to 18 μm, broader than Ge₂₈Sb₁₂Se₆₀’s 1 to 16 μm range (which has an absorption peak near 12.5 μm). Refractive index at 10 μm is 2.7777 versus 2.6023. Higher refractive index means the same optical effect can be achieved with a thinner lens. This is favorable from a SWaP-C perspective.

Tradeoffs

As₄₀Se₆₀ is not perfect. The same table in the paper reveals weaknesses. Vickers Hardness is 142 versus 189 for Ge₂₈Sb₁₂Se₆₀. It is mechanically softer and scratches more easily. CTE is 20.9 × 10⁻⁶/°C versus 14.5 × 10⁻⁶/°C. In harsh environments, DLC (diamond-like carbon) coatings are used to supplement surface hardness.

There is also a risk that should not be overlooked. Arsenic toxicity. As₄₀Se₆₀ is, as the name suggests, composed of arsenic and selenium. Arsenic is classified as “fatal if inhaled (H330)” under UN GHS, and strict safety controls are required during manufacturing to prevent dust and fume inhalation [16]. In finished lens form, the arsenic is locked within the glass matrix and poses low risk during routine handling. But regulatory burden during manufacturing and disposal is real.

As₄₀Se₆₀ is an arsenic-based glass, so substance-specific REACH/RoHS/CLP review is required at the manufacturing, polishing, and disposal stages. ECHA’s SVHC Candidate List is substance-specific rather than a blanket ban on all arsenic compounds. Finished lenses have arsenic locked in the glass matrix, but regulatory compliance verification remains a separate risk for expansion into commercial markets such as automotive and industrial applications. The industry is also developing arsenic-free compositions using antimony (Sb), and it is likely that some of the nine additional NRL-licensed compositions held by LightPath include such alternatives.

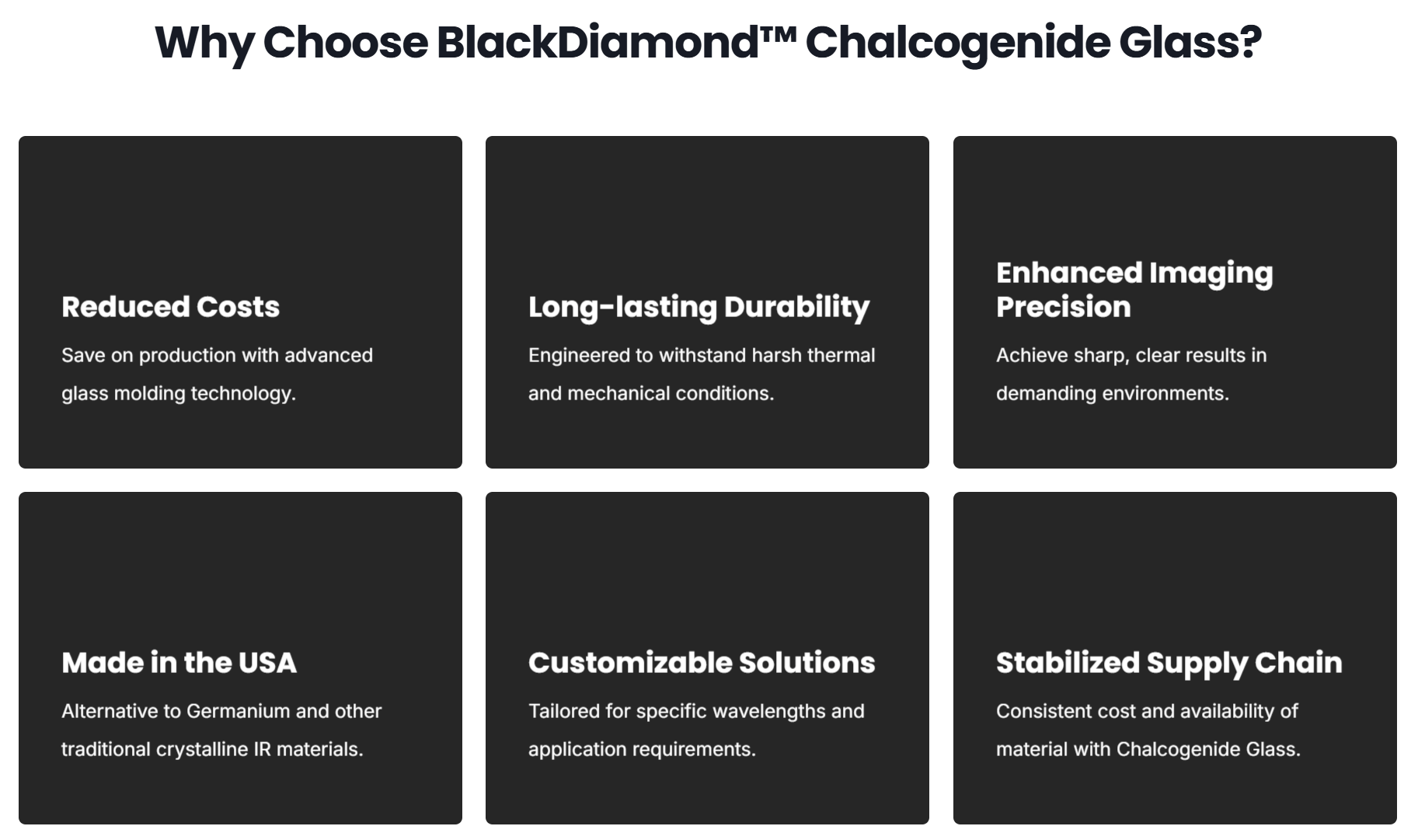

As₄₀Se₆₀ (BD6) offers germanium-free supply chain risk avoidance, athermal design freedom, and PGM volume production cost advantages, but comes with tradeoffs in mechanical durability and arsenic-related environmental regulation.

[Figure 3: Ge₂₈Sb₁₂Se₆₀ vs As₄₀Se₆₀ Material Properties Comparison]

That is the structure of the problem.

Germanium supply is concentrated in China. The NDAA will reshape procurement eligibility over 2027 to 2030. The most mature alternative material is chalcogenide glass, and within that category, the germanium-free composition As₄₀Se₆₀ has material property advantages.

The problem is not the material. The problem is how much of this material transition translates into actual backlog, gross margin, and per-share value after dilution. The harder questions start here.

First, which company can produce this material at volume within the United States? Second, is that company a simple material supplier, or can it be re-rated as a defense IR systems company? Third, and most importantly, at a $1B market cap today, is that re-rating still ahead of us?

LPTH’s story is compelling. But a good story and a good entry price are two different things.