[Investment Map] When War Drags On, Sensors Make the Money

RF GaN, EO/IR, Fiber Laser, Electronic Warfare: 28 Listed Companies in the Defense Sensor Cycle

On March 3, 2026, while KOSPI crashed 7.24%, LIG Nex1 hit the daily limit up. Hanwha Systems surged +29%, Hanwha Aerospace +20%. But among the names that rallied that day, RFHIC and i3system barely registered on most investors’ radar.

This article breaks the defense supply chain into 4 tiers and applies PhotonCap’s GVM (Global Value Map) framework across 28 listed companies from materials to system integration. The core thesis is simple. On the first day of war, platforms (fighters, tanks, warships) rally. When war drags on, the sensors and components inside those platforms make the money. Why nLIGHT (LASR) climbed +533% from its 52-week low near $12 to over $80, why ASELSAN hit a $47B market cap, why RFHIC landed a KRW 50.6B contract from Raytheon: the answer is in this tier structure.

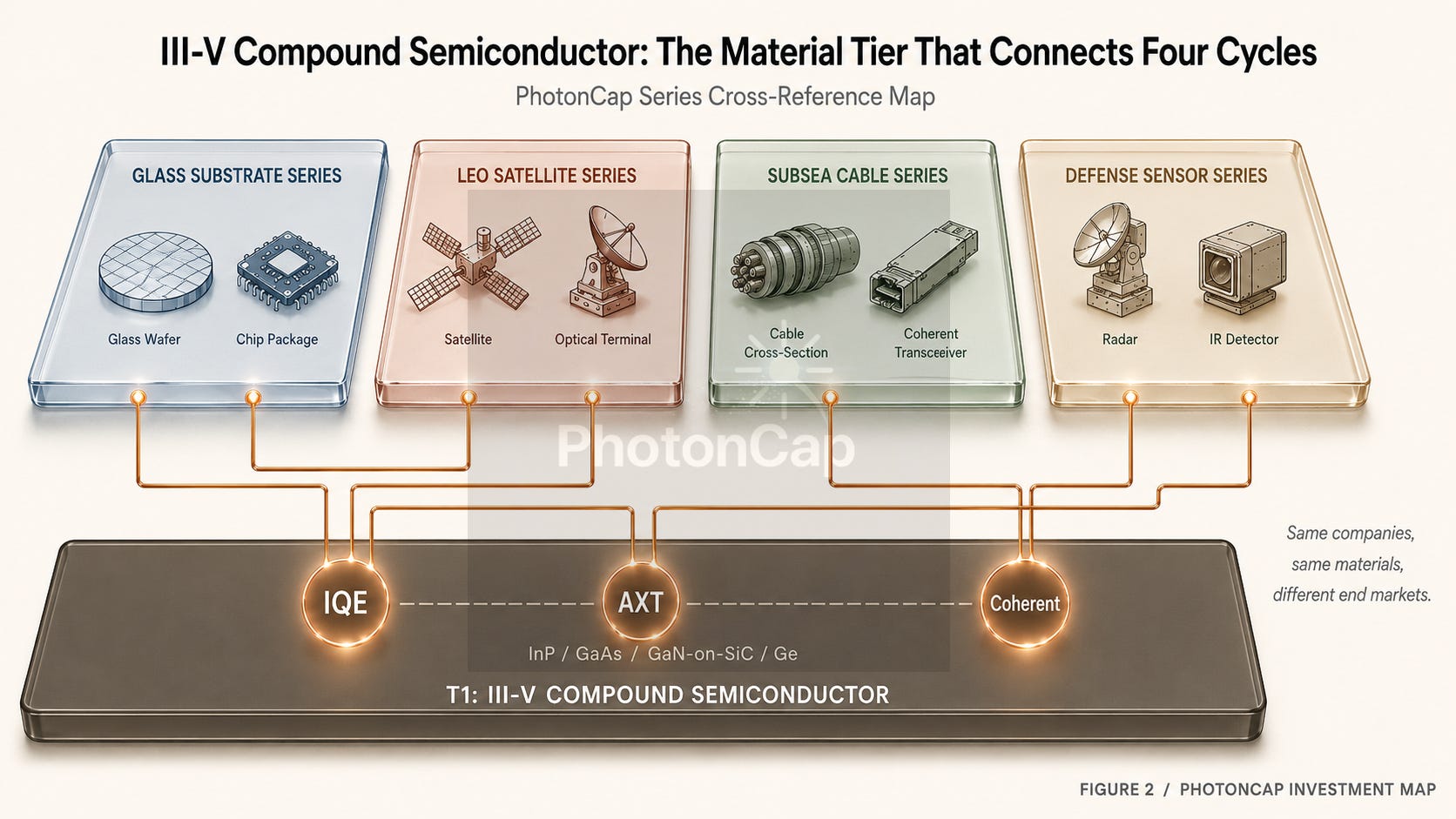

If you have been following the PhotonCap series, familiar names will appear. IQE and AXT from the glass substrate series, Coherent from the subsea cable series. III-V compound semiconductor as a material tier connecting optical communications to defense: that is why PhotonCap covers this topic.

[Investment Map] 15 Companies in the Glass Substrate Cycle: From Material to Mass Production

![[Investment Map] 15 Companies in the Glass Substrate Cycle: From Material to Mass Production](https://substackcdn.com/image/fetch/$s_!3Hj1!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fef44434b-7610-45ea-a7bc-00f695710237_1704x923.png)

For the past 30 years, high-performance CPU/GPU package substrate stacks have been built almost entirely on organic build-up substrates, specifically ABF (Ajinomoto Build-up Film) variants. 2026 is the first year glass substrates cross from R&D into pilot/qualification phase. Intel has committed to a “second half of this decade” production window [1], TSMC is reportedly preparing its CoPoS pilot line for mid-2026 completion [2], and Absolics has entered AMD certification at its Georgia Covington fab [3]. This article evaluates 15 publicly traded companies across six countries using a glass-substrate-specific GVM Score (5-axis framework), maps them to a 4-tier cascade, and distributes them across a 12-month Catalyst Calendar. Identification, mapping, and scenario analysis for all 15 companies are covered in the paid section.

[Investment Map] The Real Bottleneck 7,000m Below: The $13B Cycle Held by 60 Ships

![[Investment Map] The Real Bottleneck 7,000m Below: The $13B Cycle Held by 60 Ships](https://substackcdn.com/image/fetch/$s_!03SO!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F37b01d9f-a794-4891-8e8b-25cc5c306121_1704x890.png)

Over 95% of international internet data travels through subsea fiber optic cables. Yet only about 60 dedicated cable-laying vessels exist worldwide, with an average fleet age of 25 years. New subsea cable investment for 2025 to 2027 is projected at $13B, nearly double the prior three-year period [1]. With Google, Meta, Amazon, and Microsoft all placing orders simultaneously, the bottleneck sits at cable-laying ships and EDFA repeaters. This article breaks down the subsea cable supply chain into 5 tiers (fiber, cable, wet plant, optical components, installation) and scores 8 listed companies using the PhotonCap GVM 5-axis framework. The market has already repriced fiber and cable. Wet plant scarcity has not yet been recognized as a standalone asset.

The GVM Score is a framework I built for my own investment decisions. Of the 28 companies analyzed, I held existing positions in 3 before writing, and initiated positions in 3 additional companies immediately after constructing the GVM table. Which companies those are is disclosed inside the article.

Contents

March 3, 2026: The Day Sensors Beat Platforms

The Physics of Modern Warfare: Why Sensors Are the Bottleneck

28 Companies, 4 Tiers, and Names Not Yet Revealed

Company Identification + Peer Comparison

4 Clusters + Differentiators + Company Analysis

GVM Dashboard + Scenarios + Monitoring

References & Sources

1. March 3, 2026: The Day Sensors Beat Platforms

On March 3, 2026, the market bought sensors before platforms.

On February 28, the U.S. and Israel struck Iran. When the Korean market opened on Monday, March 3, KOSPI crashed 7.24% [1]. Samsung Electronics, SK hynix, Hyundai Motor all fell in unison. But defense stocks went the opposite direction. LIG Nex1 hit the daily limit (+29.86%), Hanwha Systems gained +29.14%, and Hanwha Aerospace rose +19.83% [1]. The entire market was in panic mode while defense was celebrating.

That much was all over the news.

What caught my attention was something else.

Scanning the list of stocks that rallied that day, names like RFHIC (intraday +17%), i3system, FiberPro, and KOTS Technology appear [2]. These companies do not build fighters, tanks, or missiles. What they make is GaN power amplifiers for radar (RFHIC), infrared imaging sensors for guided weapons and tanks (i3system), and fiber optic gyroscopes for inertial navigation systems (FiberPro).

Hanwha Aerospace builds the K9 self-propelled howitzer. LIG Nex1 builds the Cheongung-II air defense system. In systems like the Cheongung-II, the multi-function radar (MFR) and active radar seeker determine core performance. The RF power amplifiers inside this radar system are the bottleneck. RFHIC signed a KRW 50.6B high-power amplifier supply contract with Raytheon Canada [3], and is positioned to benefit from expanding K-defense guided weapon exports. i3system supplies infrared imaging sensors and FPA (Focal Plane Array) units for the K2 tank gunner sight and guided weapon seekers [4]. A core name in the K-defense IR sensor supply chain.

Platforms are the visible weapons. Sensors are those weapons’ eyes and ears.

On the first day of war, the headline is “Hanwha Aerospace builds the K9.” But when war stretches to 3 months, 6 months, a year, the story changes. The platforms are already built. What runs short is replenishing missiles, upgrading radars, replacing electronic warfare suites. Every time a missile is fired, a seeker is consumed. Every time threats evolve, radars and EW suites get replaced. Platform lifespan is 20 to 30 years, but the sensors and RF components inside them are upgraded or consumed on 5 to 7 year cycles. And the companies making these sensors and components have market caps 10x to 100x smaller than the platform companies.

The Cheongung-II intercepted Iranian missiles in actual combat in the UAE. According to operational data disclosed by Representative Yoo Yong-won, the UAE-deployed Cheongung-II reportedly neutralized approximately 29 out of 30 targets, reportedly achieving roughly 96% interception effectiveness [5]. This was the first time in K-defense history that an exported weapon system proved its performance in live combat. The UAE requested additional batteries, and Qatar and Kuwait began showing interest.

But who benefits most directly from this combat validation? A 96% intercept rate is not simply the performance of a single missile. It is the combined result of the multi-function radar, engagement control, seeker, launch vehicle, and field operations. What this article focuses on is the sensor and RF component layer that is repeatedly consumed and upgraded. The supply chain of these components is the subject of this article.

Key takeaway: When war breaks out, platforms rally. When war drags on, sensors make the money. The investment map of 28 companies across the supply chain starts here.

2. The Physics of Modern Warfare: Why Sensors Are the Bottleneck

Understanding the defense sensor supply chain requires knowing four technology axes. RF GaN, EO/IR, Fiber Laser, Electronic Warfare. These four are the “eyes, ears, fists, and brain” of modern weapons systems.

2.1 RF GaN: The Heart of Radar

Radar performance is determined by the transmit/receive (T/R) module. The industry is transitioning from silicon (Si) and gallium arsenide (GaAs) to gallium nitride (GaN). GaN can deliver over 10x the output power per unit area compared to Si. That means seeing farther, tracking more targets simultaneously, and withstanding stronger jamming.

The problem is that very few places in the world can fabricate GaN-on-SiC wafers. Growing GaN epitaxy on silicon carbide (SiC) substrates requires high temperature, high vacuum, and extreme crystal quality control. If this tier gets bottlenecked, the entire AESA (Active Electronically Scanned Array) radar supply chain halts.

MACOM fabricates GaN/GaAs RF semiconductors in its own fab. Its recent GBP 45M investment in IQE (a III-V epitaxial wafer specialist) with a long-term supply agreement signals an intent to directly manage upstream bottlenecks [6][7]. RFHIC is the only company in Korea that produces GaN transistors in-house, and it received a KRW 50.6B power amplifier supply contract from Raytheon Canada [3]. Based on analyst coverage, RFHIC’s GaN power amplifiers are also estimated to supply core RF components for the Cheongung-II radar [8].

This structure follows the same grammar as previous PhotonCap series. IQE and AXT from the glass substrate series make InP/GaAs substrates. Those substrates are used not only for optical communication lasers but also connect to radar GaN-on-SiC, SWIR sensor InP/InGaAs, and some cooled IR detector materials within the III-V compound semiconductor ecosystem. III-V compound semiconductor is the material tier that runs through optical communications, satellites, and defense.

2.2 EO/IR: The Eyes of Weapons

EO/IR (Electro-Optical/Infrared) is the technology that detects infrared radiation to identify targets. It converts thermal radiation invisible to the human eye into a camera image. Missile seekers, tank sights, drone surveillance cameras, naval surveillance systems: all use EO/IR sensors.

The core component is the FPA (Focal Plane Array). It is the detector that converts IR energy into electrical signals, and comes in two types.

Cooled: Uses InSb (indium antimonide) or MCT (mercury cadmium telluride) materials. Requires cryogenic cooling (77K) but offers high sensitivity for long-range target identification. Used in missile seekers and fighter IRST (Infrared Search and Track) systems. Uncooled: Uses VOx (vanadium oxide) microbolometers. No cooling required, making it suitable for miniaturization. Used in personal weapon sights, drone cameras, vehicle night vision.

Teledyne (formerly FLIR Systems) is the pioneer in this market. i3system is the only company in Korea that develops both cooled and uncooled IR sensors in-house, supplying FPA units for the K2 tank gunner sight and guided weapon seekers. i3system sensors are also mounted on the K2 tanks exported to Poland. The company is currently building a new uncooled factory, scheduled for full operation from Q2 2026 [4].

LightPath Technologies makes IR optical lenses. The company produces BlackDiamond, a proprietary chalcogenide glass, under an exclusive license from the U.S. Naval Research Laboratory (NRL) [9]. As a germanium (Ge) replacement material, it supplies IR cameras for L3Harris’s naval SPEIR program [9]. The most recent quarter (FY2026 Q3) showed revenue of $19.1M, up +109% year over year, with a backlog of $110.6M [10].

But LightPath’s real catalyst is elsewhere. The company was selected as a subcontractor to deliver IR thermal camera systems for Lockheed Martin’s NGSRI (Next Generation Short Range Interceptor) program, the next-generation Stinger missile replacement. It passed a qualification milestone in 2024 and began delivering flight-capable hardware to Lockheed Martin test units [11]. Following an initial order of 10,000 systems, annual follow-on orders of up to 10,000 rounds are possible over a 10-year program [11]. Per company forward guidance, LightPath’s contribution per missile is estimated at $5,000 to $10,000. If Lockheed Martin wins final selection, LightPath’s annual revenue could grow by $50M to $100M, with a lifetime value of $500M to $1B (author estimate). The CEO called this the program that could “nearly double the size of the company overnight.”

This example illustrates the core thesis of this article. Lockheed Martin builds the missile, but the missile’s eyes (IR seeker) are still made by a sub-$1B small-cap. This asymmetry is the investment logic of the sensor tier.

2.3 Fiber Laser: The Economics of the Drone Age

Directed Energy Weapons (DEW) use lasers to shoot down drones. The reason this matters comes down to economics.

Shooting down a single drone with a missile costs $0.5M to $3M. A single Patriot missile costs $4M. But defending against swarms of $500 commercial drones with dozens of Patriot interceptors is a cost structure the defender can never win.

Laser weapons cost $1 to $10 per shot. All they need is electricity. A 30kW laser can burn a small drone. A 70kW laser can intercept mortar rounds and rockets. The core of these laser systems is the high-power fiber laser, and nLIGHT is the pure-play in this market.

nLIGHT (LASR) was still doing industrial laser cutting and welding through 2025. Then it deliberately exited the industrial business and went all-in on defense DEW. The company launched the HADES directed-energy product line, with its first product being a 70kW-class high-energy laser effector [12]. It delivered lasers to the U.S. Army’s DE M-SHORAD (Directed Energy Maneuver Short-Range Air Defense) program and is expanding an assembly plant in Turin, Italy, for European customers.

From a 52-week low near $12 to over $80 recently. 1-year return is +533%. Q1 2026 revenue came in at $80.2M, up +55% year over year, with A&D (Aerospace and Defense) revenue nearly doubling [13]. Market cap is approximately $4.6B.

Coherent from the subsea cable series comes to mind here. Coherent was core to subsea cable coherent optics, but another business pillar is GaN-on-SiC substrates and high-power laser materials. The same photonics technology sends data through subsea cables and shoots down drones in defense.

2.4 Electronic Warfare: The Invisible War

Electronic Warfare (EW) is the technology that detects, jams, and deceives enemy radar and communications. In modern warfare, if EO/IR sensors are the “eyes,” EW is the “brain.” Blinding the enemy’s eyes while protecting your own.

An EW suite integrates multiple receivers, transmitters, signal processors, and antennas into a single system. It also uses GaN RF components (high power is needed to transmit jamming signals), IR sensors (missile approach warning), and software-defined architecture.

Elbit Systems (Israel) has combat-proven EW technology. The Mini-MUSIC DIRCM (Directed Infrared Countermeasure) system blinds the IR seeker of an incoming missile with a laser. In 2026, it received a $275M EW suite contract from an Asia-Pacific country [14]. Hensoldt (Germany) has the Kalaetron EW product family, and as of Q1 2026, new orders surged year over year, pushing the order backlog to EUR 9.8B [15].

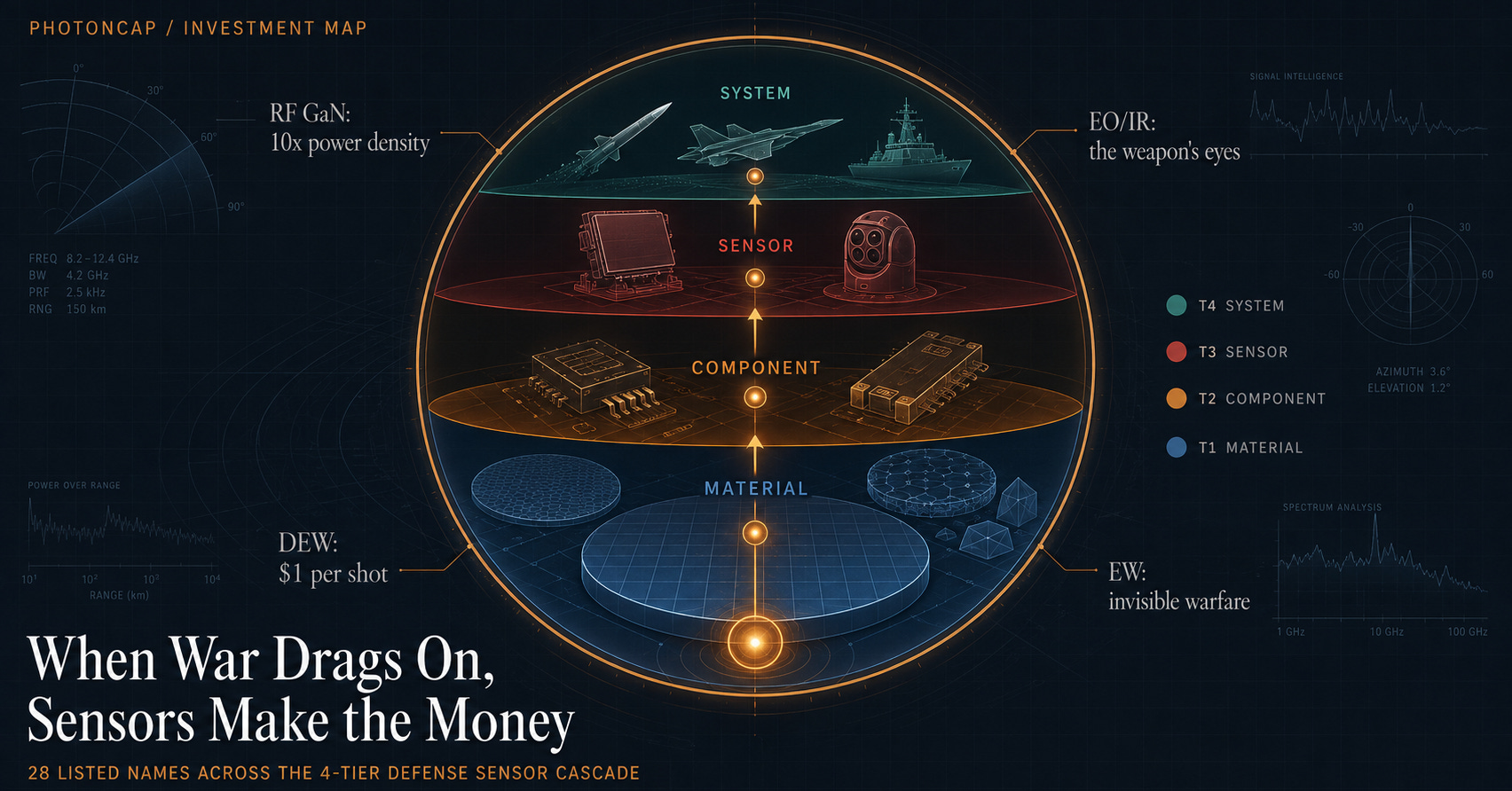

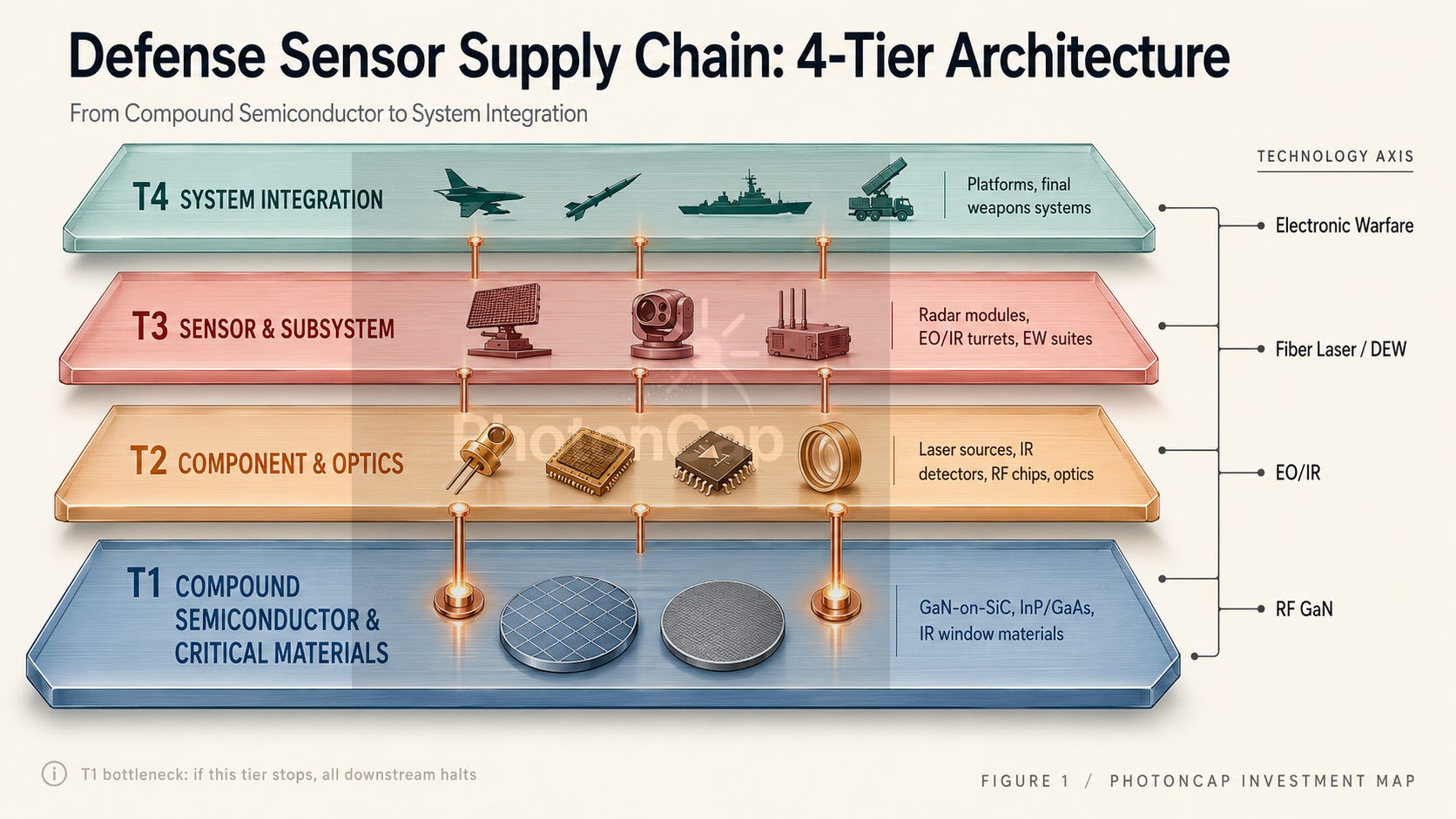

[Figure 1: Defense Sensor 4-Tier Supply Chain Map]

2.5 The 4-Tier Structure: From Materials to Systems

Breaking these four technology axes into a supply chain yields 4 tiers.

T1 Compound Semiconductor and Critical Materials: Companies making GaN-on-SiC wafers, InP/GaAs substrates, and IR window materials. If this tier stops, neither radars nor sensors function.

T2 Component and Optics: Companies using T1 materials to build laser sources, IR detectors, RF chips, and optical lenses. Performance is determined at this tier.

T3 Sensor and Subsystem: Companies assembling T2 components into radar modules, EO/IR turrets, and EW suites. Units mounted directly onto weapons systems.

T4 System Integration: Companies integrating T3 sensors into final weapons systems (missiles, fighters, warships, air defense systems). Hanwha Aerospace, L3Harris, and Elbit sit here.

This structure follows the same grammar as previous PhotonCap series. The LEO satellite series had T1 (materials) through T5 (services). And at the T1 material tier, the same companies appear repeatedly. IQE made InP laser epi for LEO satellites; here it makes GaN epi for radar. AXT made InP substrates for optical communication lasers; here it makes GaAs substrates for IR detectors.

[Investment Map] 26 Companies in the LEO Satellite Cycle: From Deployment to Service

![[Investment Map] 26 Companies in the LEO Satellite Cycle: From Deployment to Service](https://substackcdn.com/image/fetch/$s_!lPvt!,w_1300,h_650,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fc1928833-682c-4872-9ef1-c3bf54eb9fca_1704x893.png)

LEO mega-constellations are moving from a “deployment phase” to a “service phase.” Amazon Leo (formerly Project Kuiper) began its enterprise preview in November 2025 and confirmed a mid-2026 commercial launch [1][7]. AST SpaceMobile received FCC commercial authorization for its 248-satellite direct-to-device constellation [2]. Starlink operates an active constellation of roughly 10,000 satellites by tracker count [3]. This piece evaluates 26 listed names spread across nine or more countries (North America, Europe, Korea, Japan) using a satellite-comm-cycle-specific 5-axis GVM Score, maps them onto a 4-tier cascade, and distributes them across a Catalyst Calendar through the end of 2027. Identification, mapping, and scenario analysis for the 26 names are covered in the paid section.

That is why this article reads defense through III-V materials and sensor supply chains, not through platforms. Other defense analyses do not show this connection. You have to understand the physics inside the sensors to see it.

Key takeaway: The defense sensor supply chain has a 4-tier structure where T1 materials are the most scarce and irreplaceable. And the companies at T1 overlap with the III-V semiconductor names PhotonCap has already covered across other series.

[Figure 2: III-V Compound Semiconductor Cross-Series Map: T1 material overlap across Glass Substrate, LEO Satellite, Subsea Cable, and Defense Sensor series]

3. 28 Companies, 4 Tiers, and Names Not Yet Revealed

Everything up to this point is visible from public information alone. That GaN is core to radar, that EO/IR sensors are the eyes of weapons, that laser weapon economics are changing missile defense: this is first-order structure that appears in sell-side defense reports.

The differentiation for investors begins here.

Place 28 listed companies across 4 tiers and score them with GVM, and four clusters emerge.

[A] Bottleneck Component / Material: Companies with monopoly or near-monopoly positions in specific materials or sensor components. If these companies stop supplying, radars go dark or missiles cannot fly. Small market caps, but everything upstream depends on them.

[B] Sensor Origin: Companies with deep technology moats. IP that competitors cannot replicate within 5 years.

[C] System Integrator: Companies where backlog equals strength. The longer war lasts, the more backlog accumulates, converting to revenue over the next 3 to 5 years.

[D] Market Cap Dislocation: Companies with high GVM scores but where the market has not yet re-rated. This gap is the cycle alpha.

Which companies belong to [A], which to [D]: that unfolds after the paywall.

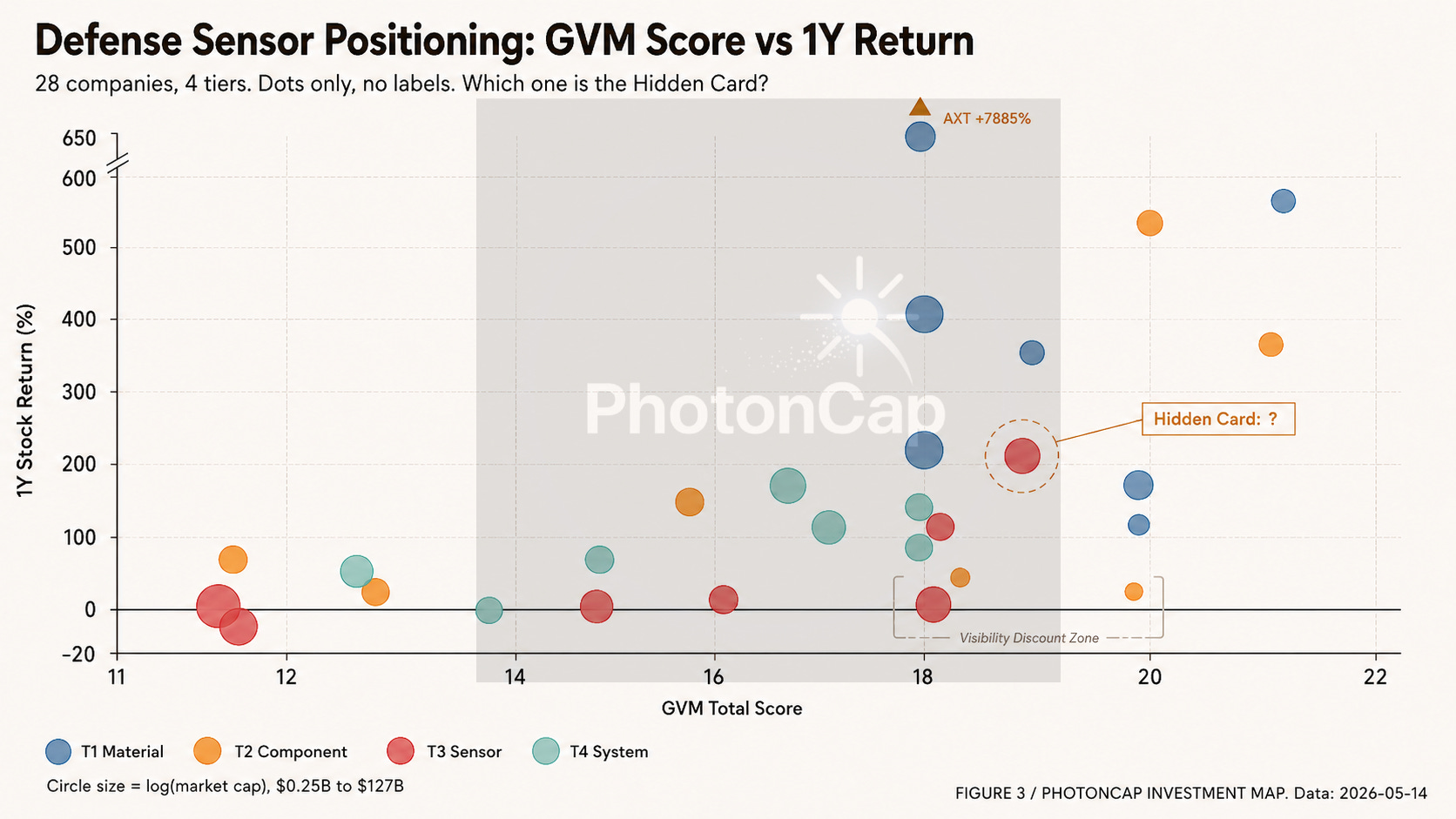

One preview. Among the 28 companies, one recorded a 1Y return of +7,885%, and another hit a $47B market cap while having near-zero awareness among Korean investors. The GVM scores and re-rating velocity of these two companies are the most important data points in this series.

[Figure 3: Positioning Scatter Plot (dots only, no labels). Dashed circle on the Hidden Card]

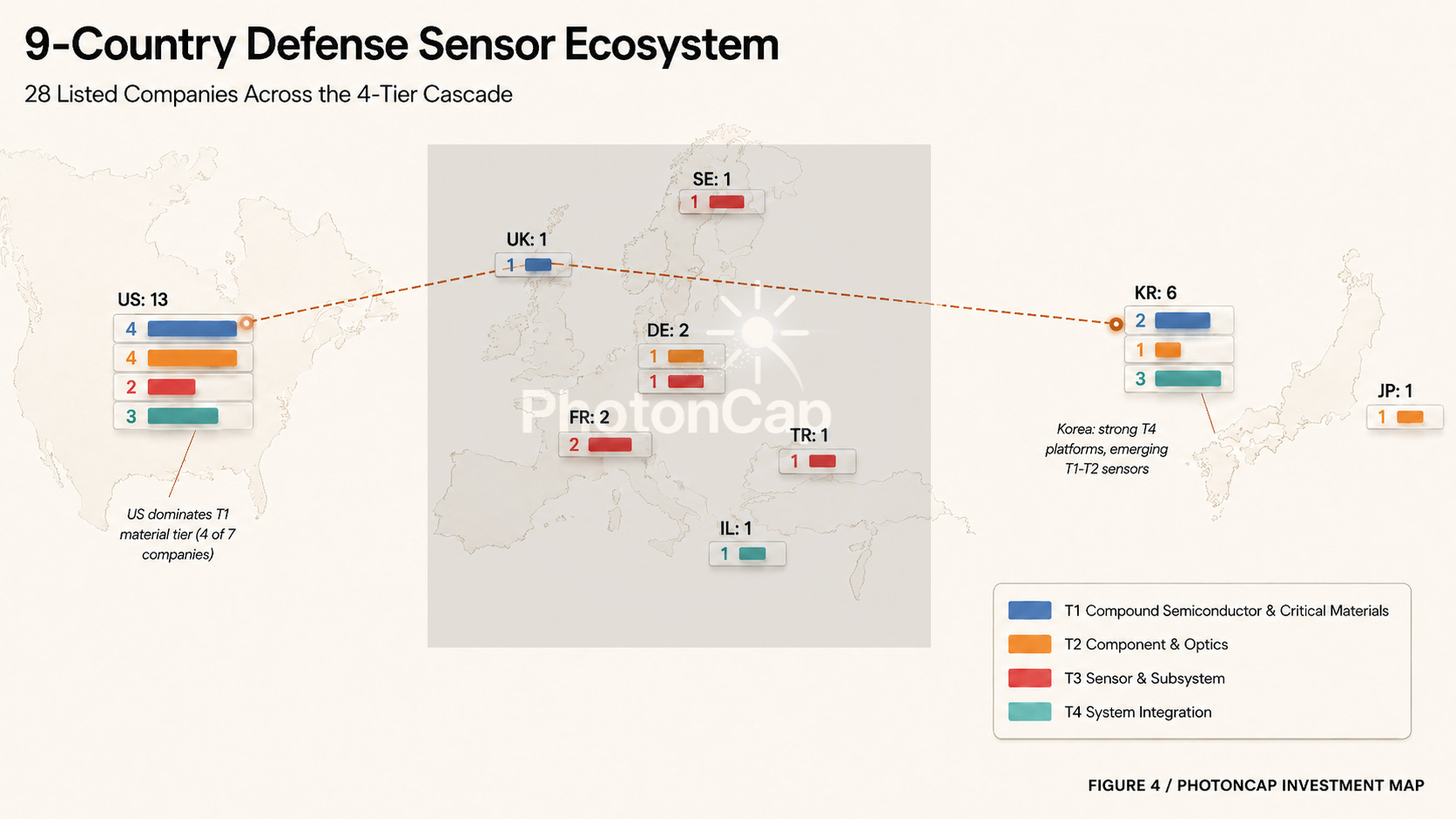

One more thing. This series features companies from 9 countries. The United States, Korea, the United Kingdom, Germany, France, Israel, Turkey, Japan, and Sweden. Only 3 names are familiar to Korean investors (Hanwha Aerospace, LIG Nex1, Hanwha Systems). Among the remaining 25 companies, some have never been covered in a single Korean brokerage report.

Their names, tier placement, GVM scores, and 4-cluster mapping are revealed for the first time in this article.

[Figure 4: 9-Country Defense Sensor Ecosystem Map, country-by-tier distribution]