The Truth Behind Marvell-Polariton: Is LWLG the First Candidate, or Just a Backup Bet?

$LWLG $MRVL $LITE $COHR: What Marvell bought, what it didn't, and where LWLG actually stands

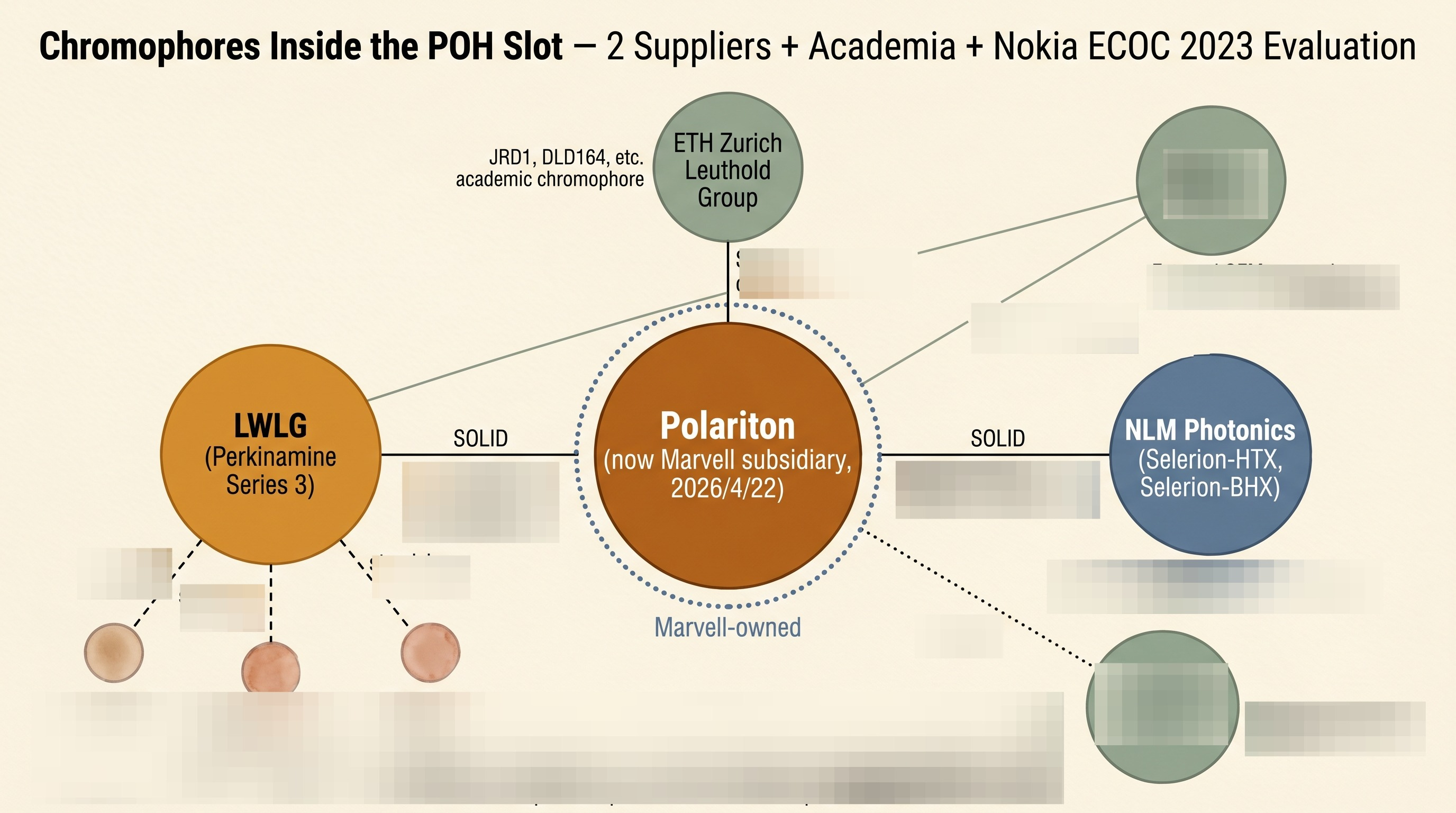

On April 22, 2026, Marvell acquired Polariton Technologies, an ETH Zurich spinoff. The press-release target: “3.2T and beyond.” Marvell acquired Polariton’s POH slot architecture, device IP, and engineering team. But the chromophore that operated the public record device remained outside Marvell’s disclosed acquisition perimeter. That distinction matters. Polariton’s POH structure only delivers record performance when an organic EO chromophore is placed inside the plasmonic slot. The Optica 2025 record device measured up to 1.14 THz and reported 997 GHz 3-dB EO bandwidth; its acknowledgment explicitly names Lightwave Logic ($LWLG)’s Perkinamine series 3 as the material used. That does not prove LWLG is in Marvell’s production BOM. It does make LWLG a documented material contributor to Polariton’s record POH stack.

This piece walks through that structure in four steps: (1) how the device works, (2) what exactly Marvell did not acquire, (3) how Marvell’s supplier relationship reorganization aligns with LWLG’s operational stance, and (4) whether $LWLG’s value comes from Polariton exposure or from the standalone foundry track (Tower / GlobalFoundries / AMF). The full landscape of EO polymer modulator industry and the comparison with NLM Photonics was covered in detail in a previous piece [5], so this piece narrows down to the Marvell-Polariton-LWLG vector.

Contents

Intro: The day Marvell bought Polariton, and the landscape one week later

What a POH modulator is, and why µm scale is decisive

Why this mapping is the key variable for the next 12 months

The one axis Marvell did not acquire: the chromophore layer

Six modulator platforms and LWLG’s standalone track

$LWLG (Perkinamine) vs NLM Photonics (Selerion): real second-source risk and CPO suitability

Supplier relationship reorganization and LWLG’s disclosure discipline

12-24 month scenarios and monitoring

References & Sources

1. Intro: The Day Marvell Bought Polariton, and the Landscape One Week Later

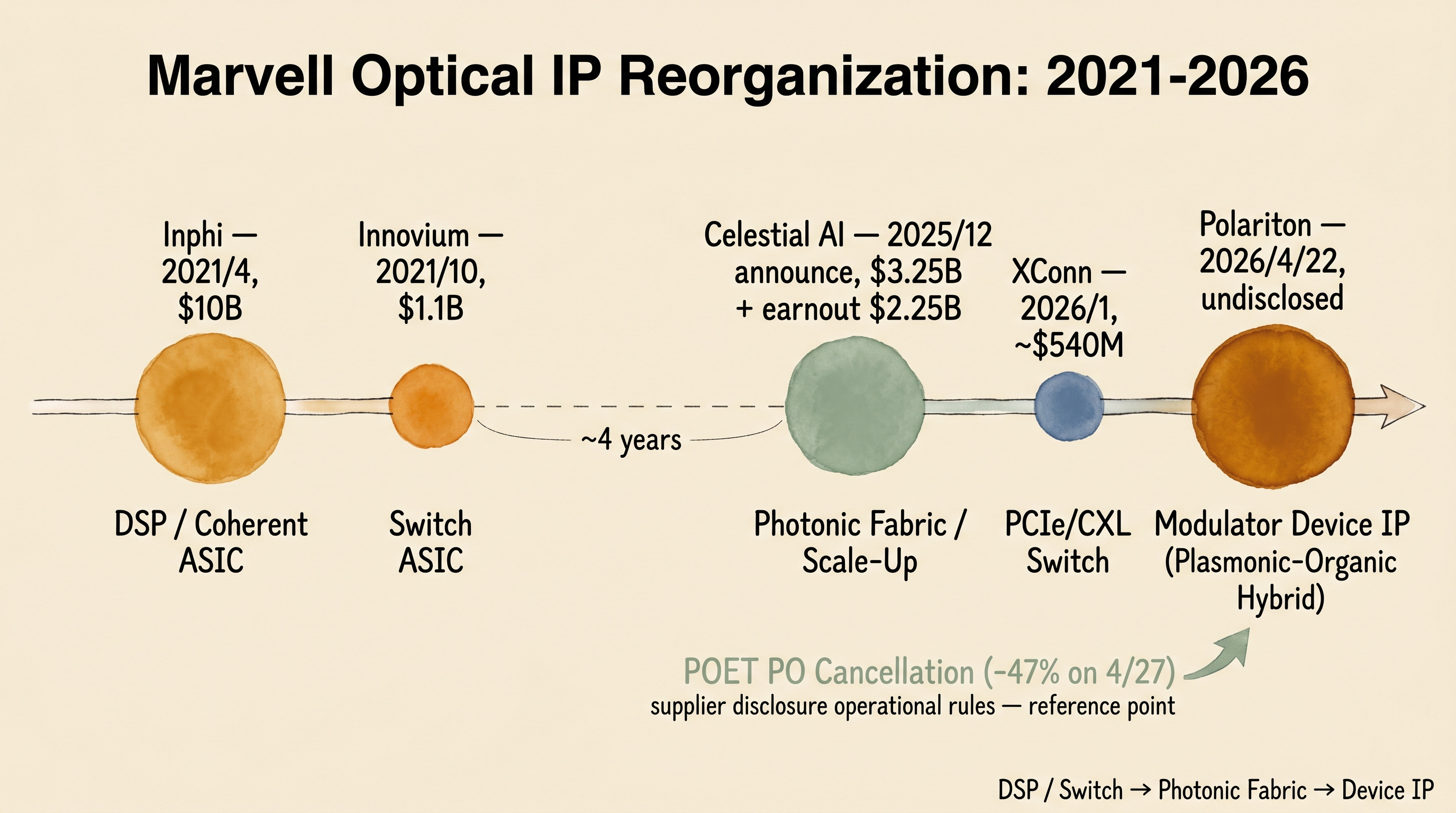

April 22, 2026. Marvell announced its acquisition of Polariton Technologies, an ETH Zurich spinoff. The deal price was undisclosed. The press release was titled “Advancing Optical Performance Scaling to 3.2T and Beyond,” with quotes from Sandeep Bharathi, President of Marvell Data Center Group.[1] The Marvell IR press release explicitly names the application target as “scale-across, DCI, ZR/ZR+ coherent, 3.2T and beyond.” That is, Polariton POH is, from Marvell’s perspective, a device-level modulation IP aimed at scale-across, DCI, ZR/ZR+ coherent optical interconnect. On the same day, the market interpreted this transaction as a strengthening of Marvell’s optical roadmap.

April 22, around 5 PM ET. A POET Technologies ($POET) CFO interview aired on Stocktwits TV. He explicitly named Marvell as the “industry-leading customer” for the Sivers ELS PIC and disclosed Foxconn / Luxshare partnership negotiations.[3]

April 23-27. Marvell sent POET an NDA violation notice and canceled all Celestial AI purchase orders.[2] According to POET, Marvell stated that disclosures regarding POs and shipping information violated confidentiality obligations. External media coverage pointed to the CFO interview context.[3] This event is not the main subject of this piece, but it works as a reference point for how Marvell operates supplier-relationship disclosure rules after acquisitions, which is revisited in §7.

April 21. LWLG filed an 8-K disclosing an amendment to its Roth Capital Partners ATM Sales Agreement, increasing the program capacity to $51.4045M. The same filing disclosed that 8,079,319 shares had already been sold under the prior agreement for gross proceeds of approximately $35M.[18]

April 29. LWLG announced the engagement of Michael Best & Friedrich LLP as outside IP counsel. The stated purpose: building a “licensing-friendly ecosystem” for foundry and design partners. Aref Chowdhury, who joined LWLG as CTO & Head of Strategy on January 1, 2026 (formerly Nokia Network Infrastructure VP & CTO), was the named voice on the announcement.[4]

The same industry, the same week, multiple events. Different headlines, but the same underlying pattern. PhotonCap’s reading: Marvell is internalizing the layers where differentiated IP condenses (optical modulator, system interconnect), and reclassifying specific external assembly/interposer supply relationships into options it can control more strictly. Having secured DSP[15] and switch layers in 2021 with Inphi and Innovium, Marvell moved through the December 2025 Celestial AI announcement / February 2026 closing (upfront approximately $3.25B + earnout up to $2.25B)[16] and arrived at the April 2026 Polariton acquisition. While the first three were DSP, switch, and system interconnect, Polariton stands apart in that Marvell directly secured plasmonics-based device-level modulation IP.

[Figure 1: Marvell Optical IP Reorganization Timeline 2021-2026]

This piece walks through that structure in four steps: (1) how the device works, (2) what exactly Marvell did not acquire, (3) how Marvell’s supplier relationship reorganization aligns with LWLG’s operational stance, and (4) whether $LWLG’s value comes from Polariton exposure or from the standalone foundry track (Tower / GlobalFoundries / AMF). The full landscape of EO polymer modulator industry and the comparison with NLM Photonics was covered in detail in a previous piece [5], so this piece narrows down to the Marvell-Polariton-LWLG vector.

§1 Summary: One week of events (Marvell-Polariton acquisition, POET PO cancellation, LWLG ATM + Michael Best engagement) read as a single current. Marvell pulls device-level modulation IP inside while reorganizing external assembly/supplier relationships into more strictly controlled options. PhotonCap’s reading.

2. What a POH Modulator Is, and Why µm Scale Is Decisive

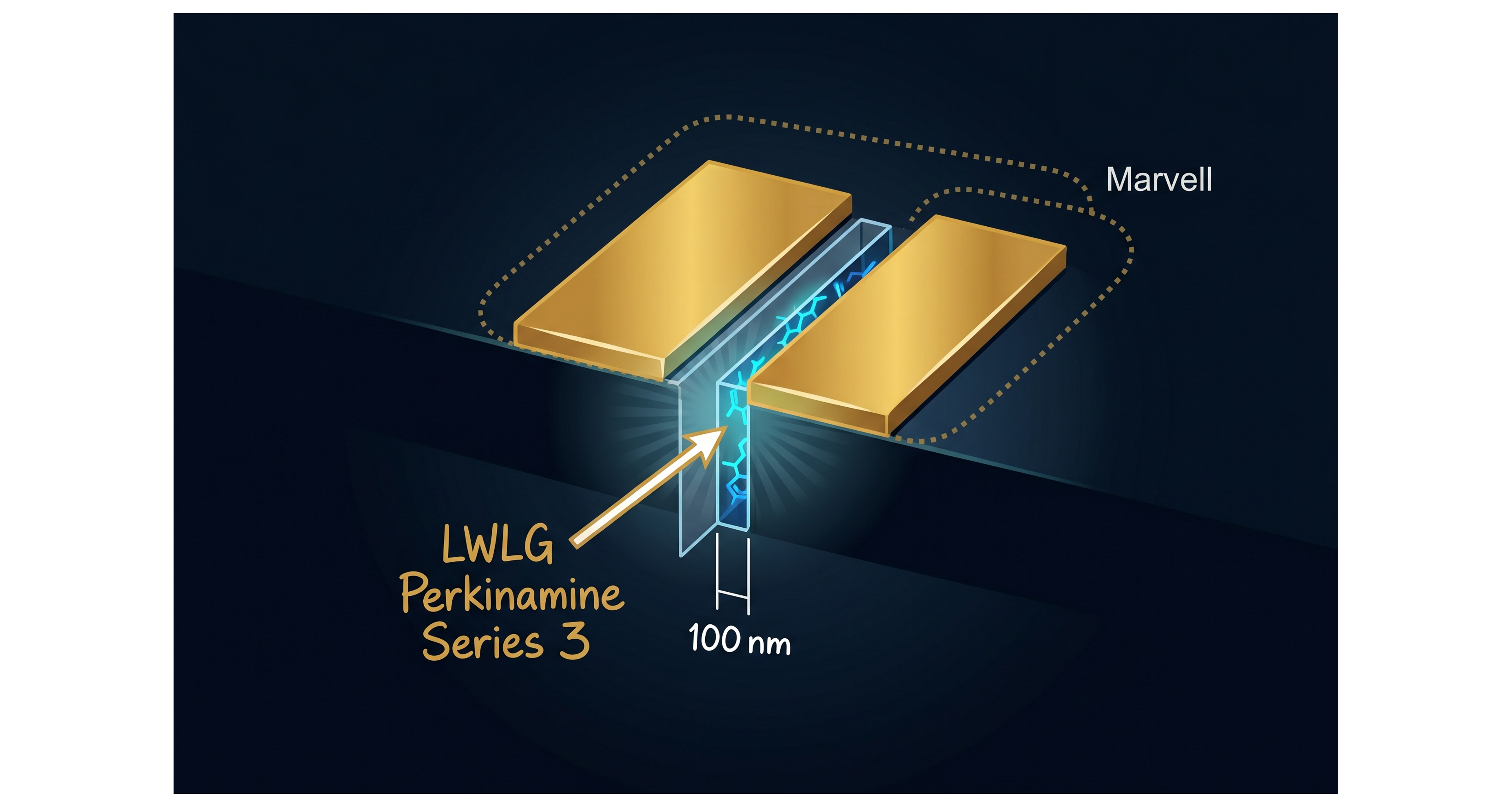

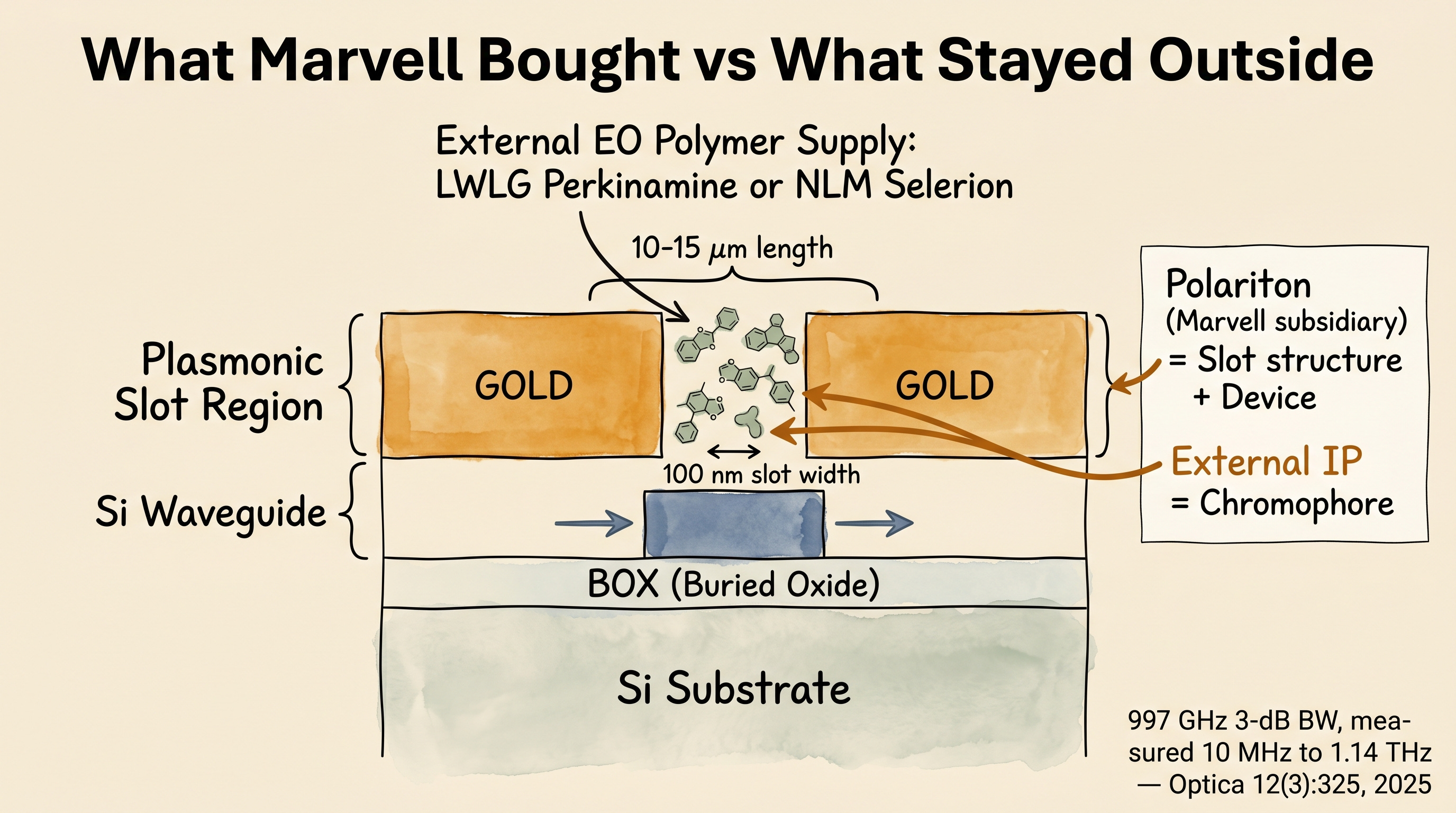

POH (Plasmonic-Organic Hybrid) is a modulator that places organic EO chromophore inside a 100 nm metal slot,[9] then uses surface plasmon polariton (SPP) field compression to dramatically amplify EO efficiency. The mechanism itself is not new. Linear EO modulation based on Pockels effect (χ⁽²⁾) is the same approach as TFLN (Thin-Film Lithium Niobate), but POH’s distinct point is µm-scale active length.

The Optica 2025 record device (Polariton + ETH joint result) reported measurements up to 1.14 THz, 997 GHz 3-dB EO bandwidth, with active length of just 10-15 µm.[6] The slot width is 100 nm. The 100 nm slot is filled with organic EO chromophore, and the SPP field is concentrated only inside that slot, dramatically amplifying the field intensity. Compared to silicon Mach-Zehnder modulators that require lengths of several mm, this is roughly two orders of magnitude shorter.

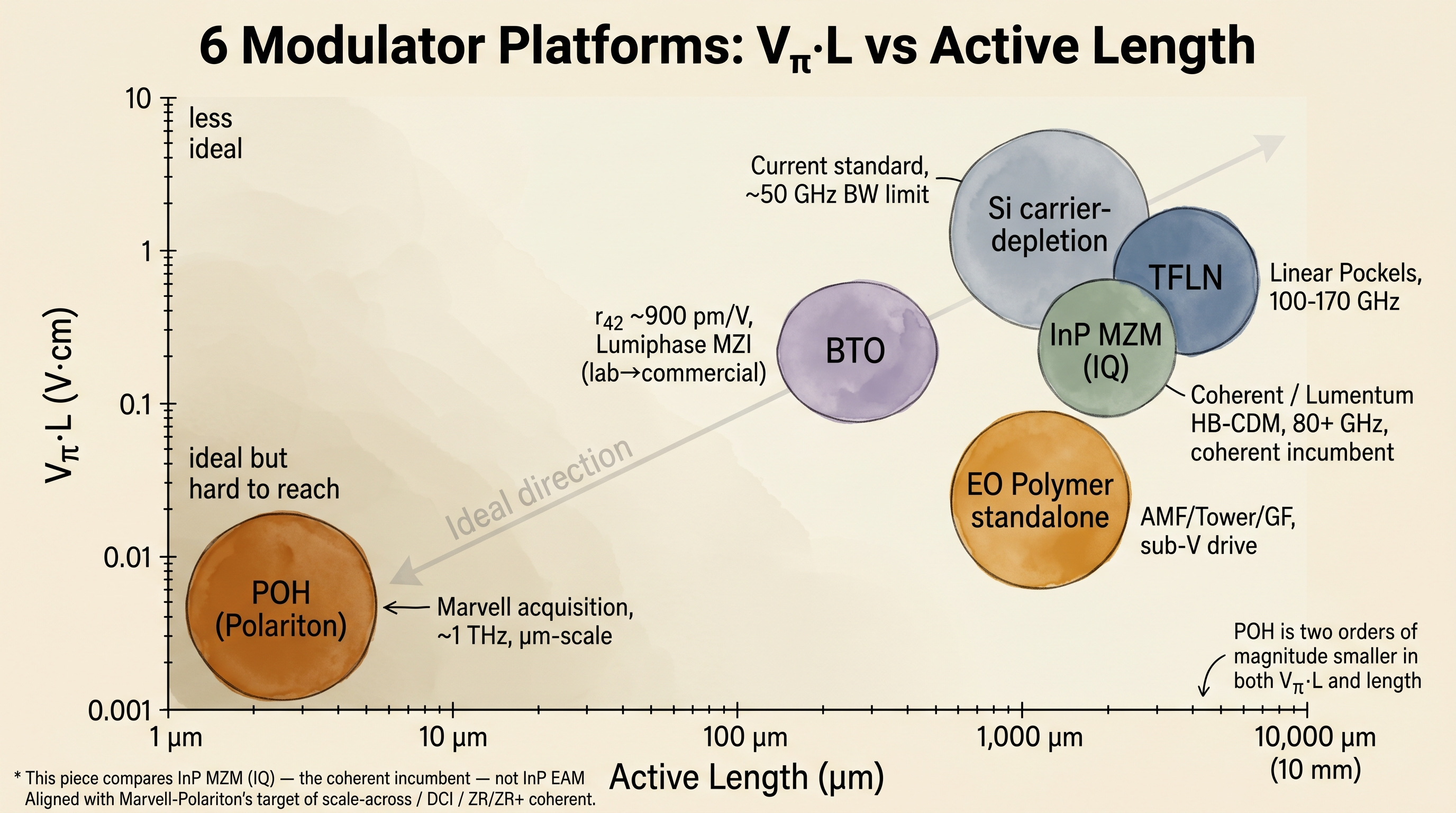

The implication is two-fold. First, footprint shrinks dramatically, allowing high-speed modulators to be densely integrated into transceiver/packaging environments. Second, driving voltage drops sharply. The Optica 2025 paper reports 117 V·µm phase modulator equivalent VπL (= ~0.013 V·cm in MZM equivalent).[6] Compared to TFLN’s typical Vπ·L of ~1 V·cm, this is also two orders of magnitude smaller.

[Figure 2: 6 Modulator Platforms, Vπ·L vs Active Length scatter]

Why does this matter for AI optical interconnect? GPU, HBM, and switch ASIC are the visible capex of AI infrastructure. The next bottleneck is moving toward the electrical-to-optical conversion layer that connects them. The optical modulator that converts electrical signals into light, a µm-scale device, is the next bottleneck.

The key constraint is power per bit. As lane rates climb from 800G to 1.6T to 3.2T+, two metrics tighten simultaneously: per-lane data rate and per-bit power consumption. Conventional silicon modulators (carrier-depletion or carrier-injection, plasma dispersion based) hit the ~50 GHz bandwidth limit. TFLN is faster and has linear Pockels response, but its mm-cm active length keeps the modulator footprint and driving voltage above what hyperscaler optical interconnect roadmaps target. POH is the platform that crosses both bottlenecks: ~1 THz bandwidth and µm-scale length.

§2 Summary: POH = SPP field compression in 100 nm slot + organic EO chromophore. Active length 10-15 µm, ~1 THz bandwidth, sub-fJ/bit class drive. From the AI optical interconnect bottleneck perspective, POH is the platform that crosses both bandwidth and footprint/power bottlenecks. The chromophore inside the slot is the source of all this performance.

3. Why This Mapping Is the Key Variable for the Next 12 Months

Up to this point, the public-record facts are straightforward: Marvell acquired Polariton, the deal price is undisclosed, the application target is scale-across / DCI / ZR/ZR+ coherent / 3.2T and beyond. POH device performance is approximately 1 THz bandwidth, µm scale.

The reading from §4 onwards starts diverging here. Did Marvell really acquire 100 percent of the technology that delivered the Optica 2025 record device? The press release says “Plasmonic-Organic Hybrid technology and the engineering team,” but the chromophore inside the slot is a chemically synthesized organic EO material. Polariton’s slot structure and the chromophore inside that slot are not the same IP. Acquiring the slot and acquiring the chromophore are separate questions.

[Figure 3: POH Device Cross-Section, What Marvell Bought vs What Stayed Outside]

This is where the asymmetry that creates the LWLG opportunity opens up. Specifically, three things: (1) the structural reason why the chromophore must remain external, (2) the gap between standalone track value and Polariton-exposure option value in the LWLG valuation function, (3) whether NLM Photonics’ Selerion can close the second-source risk vector.

This is where the investment-relevant boundary appears. So far, public materials have established the device performance and the acquisition target. The real difference starts in §4. Marvell acquired the slot, but did not acquire the chromophore. Within the next 12 months, the answer to the question “what chromophore goes into Marvell’s POH production line” is the asymmetric position variable. Two hidden cards live in this cycle. One is the single line in the Optica 2025 acknowledgment. The other is the multi-vendor POH ecosystem confirmed in the Nokia ECOC 2023 paper as a primary source. These two are the variables for the next 12 months of asymmetric position.

Paid Section Guide

§4. The one axis Marvell did not acquire (chromophore layer): Optica 2025 acknowledgment primary source + Nokia ECOC 2023 paper primary source. The exact citation showing external OEMs evaluated the Polariton + LWLG combination from approximately 2.5 years before Marvell’s acquisition.

§5. Six modulator platforms and LWLG’s standalone track: Si carrier / InP MZM / TFLN / BTO / EO Polymer / POH order-of-magnitude comparison. The structure where LWLG builds value through Tower / GF / AMF separately from Polariton exposure, plus LWLG company position table (market cap, cash, monthly burn, 4 Stage 3 customers, all primary source).

§6. Perkinamine vs Selerion (real second-source risk and CPO suitability): Material-by-material r₃₃, Tg, GR-468 pass status, and 100°C+ CPO environment suitability. Where NLM Selerion has the upper hand by metric, head-on.

§7. Supplier relationship reorganization and LWLG’s disclosure discipline: What the POET event revealed about Marvell’s post-acquisition supplier operating rules. How LWLG’s anonymous customer naming + Chowdhury CTO appointment + Michael Best IP advisory line align toward a licensing revenue model.

§8. 12-24 month scenarios and monitoring: Scenarios A/B/C classification with LWLG / NLM impact mapping. Seven monitoring points for 2026 H2 (OFC, ECOC, quarterly earnings, Tower/GF tape-out, etc.).