The Nuclear Cycle AI Data Centers Revived: 13 Listed Companies Beyond Constellation and Cameco

The source of power $MSFT $GOOG $AMZN $META contracted for | $CEG $CCJ $LEU + 10 more

AI data center power demand has triggered a nuclear renaissance. As of April 2026, over 75 reactors are under construction worldwide (WNA), and the U.S. DOE has set a target of adding 200GW of new nuclear capacity by 2050. This article deconstructs the nuclear supply chain into 5 tiers (Fuel, Reactor Design, Components, EPC, Operations/Services) and scores 13 globally listed companies (4 Korean, 9 international) using the PhotonCap GVM framework. With 1-year returns ranging from +322% to -50% across the same supply chain, we map where alpha remains.

Contents

Introduction

The Physics Behind the Nuclear Renaissance

The 5-Tier Supply Chain

Framework Preview

13-Company Identification + GVM Score

5-Group Classification + Company Analysis

Scenarios + Monitoring + Conclusion

References & Sources

1. Introduction

One-year stock returns.

+322%. +300%. +105%. +98%.

And within the same nuclear supply chain: -4%, -15%, -50%.

This is not simply a story of “nuclear stocks went up.” The market has already repriced one bottleneck in the nuclear value chain at a $100B+ valuation while leaving another below $5B. That gap is the signal.

Which stocks? This article answers that.

Of the few options capable of delivering 24/7 carbon-free firm power at scale and on multi-decade contracts, nuclear has re-emerged as a leading candidate.

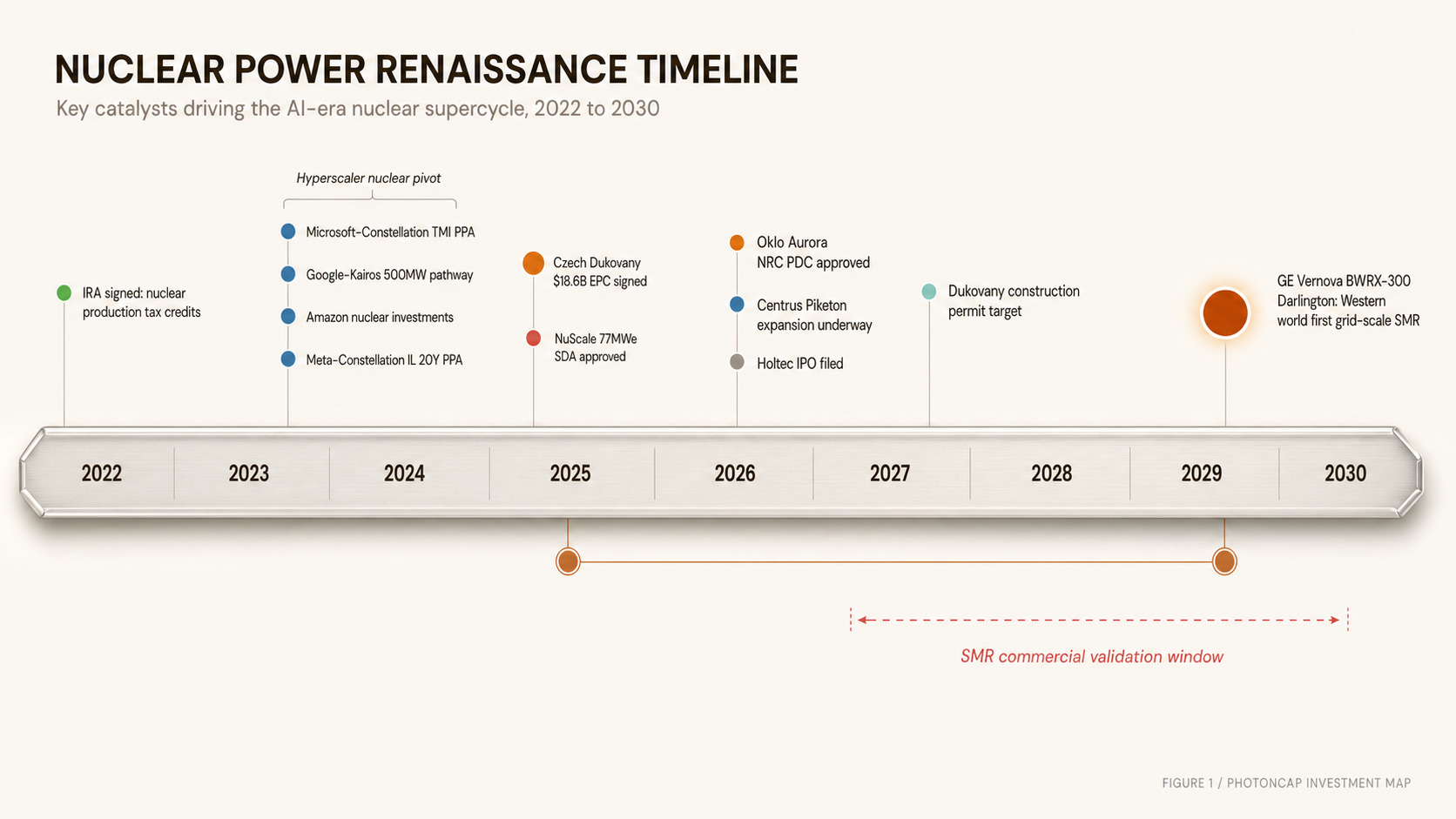

Microsoft signed a 20-year PPA with Constellation Energy to restart the Three Mile Island reactor. Google signed an agreement with Kairos Power to open a pathway for up to 500MW of SMR power by 2035 [1]. Amazon is backing multiple nuclear projects. Meta signed a 20-year PPA with Constellation’s Illinois fleet. All four hyperscalers placing nuclear into their AI power procurement strategies at roughly the same time signals that the demand narrative for nuclear has shifted from utility-centric to hyperscaler-centric.

Most investors hear “nuclear stocks” and think of Constellation or Cameco. The nuclear cycle runs much deeper. From uranium mines through enrichment, reactor design, pressure vessel manufacturing, construction, operations, and maintenance, it spans 5 tiers, each with different bottlenecks, and therefore returns that diverge by orders of magnitude: +322% versus -50%.

This article’s core question is not which company operates nuclear plants, but which tier collects tolls when the nuclear renaissance actually creates bottlenecks.

PhotonCap has previously analyzed the glass substrate cycle (15 companies), LEO satellite cycle (26 companies), subsea cable cycle (8 companies), and defense sensor cycle (28 companies) using the same framework. The nuclear cycle steps outside photonics, but it directly connects to the existing series as the power layer of the AI infrastructure supercycle. We analyzed the optical transceivers inside data centers, so analyzing the power source that turns those data centers on is a natural extension.

[Figure 1: Nuclear Power Renaissance Timeline, 2022-2030]

2. The Physics Behind the Nuclear Renaissance

Why nuclear, why now

Global data center capacity is projected to roughly double to 200GW by 2030. That implies 100GW of new capacity needed. Solar and wind face intermittency. Natural gas emits carbon. Hydro is site-constrained. Geothermal remains limited in scale. Nuclear has re-emerged as one of the most realistic large-scale options for 24/7 carbon-free firm power.

Hyperscalers recognized this starting in 2024. This is not ESG messaging. It is multi-GW procurement on long-term contracts.

The construction pipeline

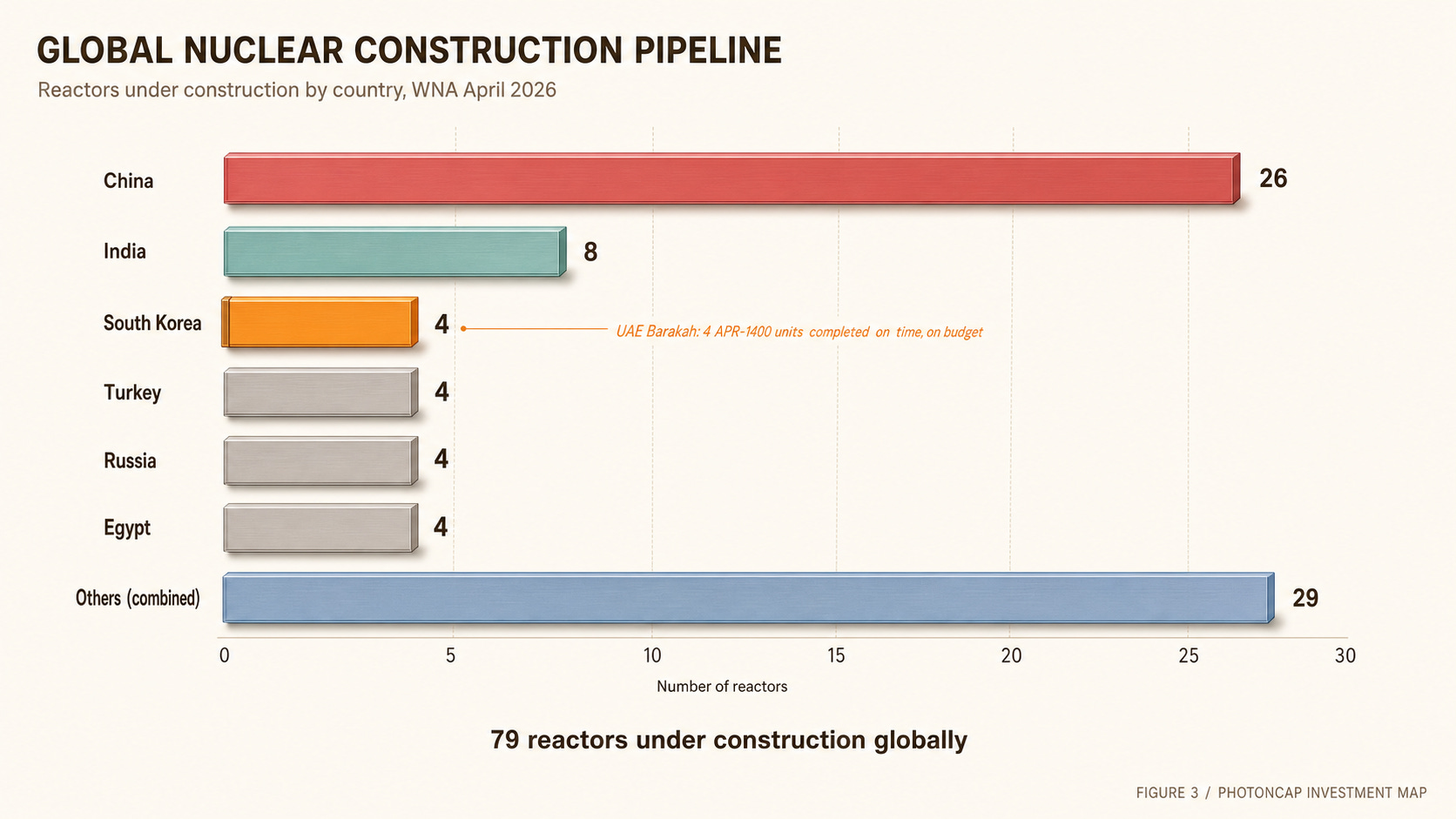

As of April 2026, the World Nuclear Association counts over 75 reactors under construction globally, with the dashboard showing 79 [2]. China leads, followed by India, South Korea, Turkey, and Russia. The U.S. is simultaneously pursuing fleet life extensions, reactor restarts, and new SMR construction.

The U.S. DOE set a target in 2024 to add 200GW of new nuclear capacity by 2050 [3]. Subsequently, executive-level targets have gone as high as quadrupling current capacity from roughly 100GW to 400GW. Either scenario requires capacity that conventional large reactors alone cannot deliver. That is why SMRs are essential.

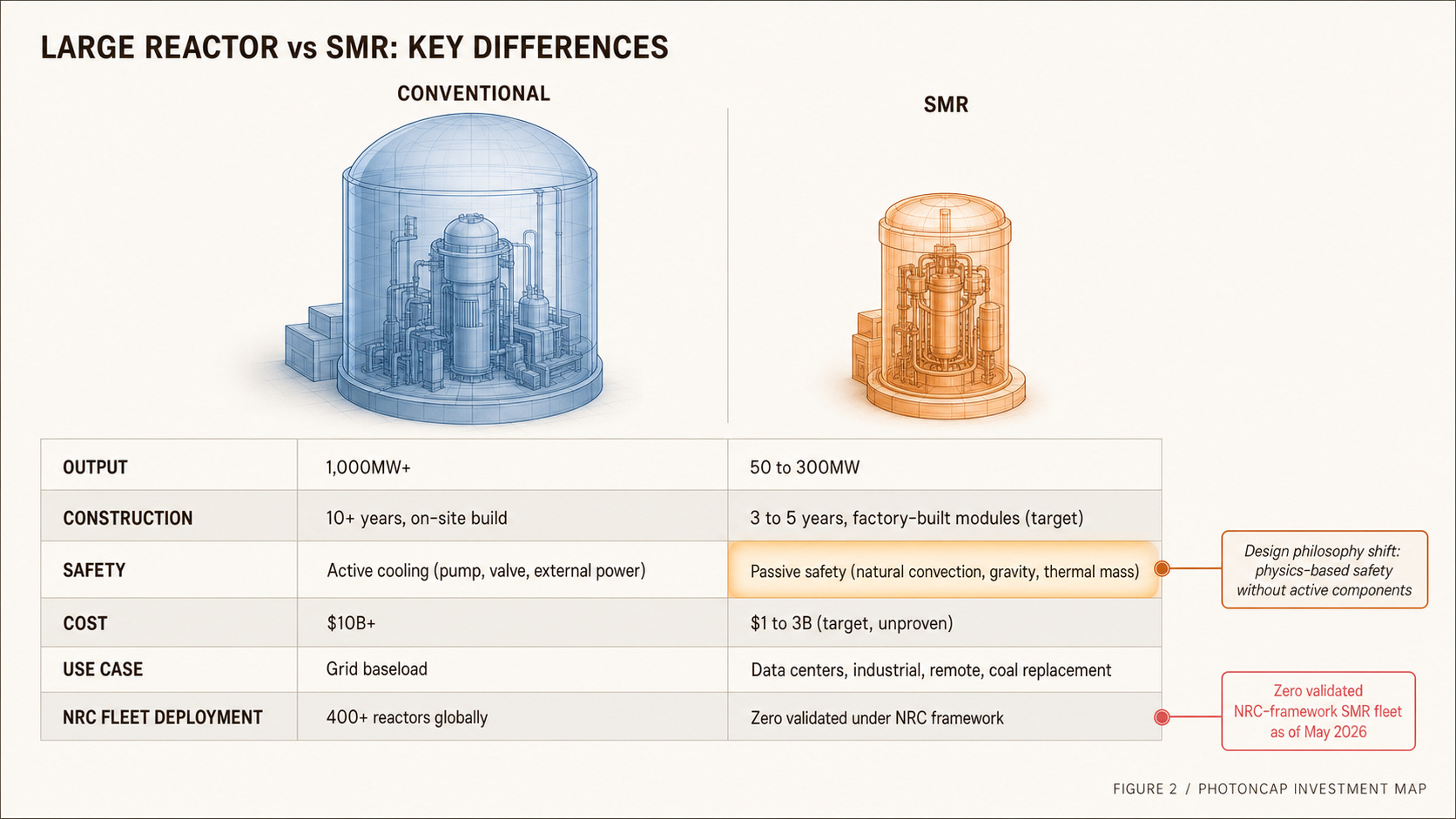

SMR: what is different

Traditional large reactors produce 1,000MW+, take 10+ years to build, and cost $10B+ (Vogtle being the textbook example). SMRs target 50 to 300MW output, factory fabrication with on-site assembly in 3 to 5 years (target).

The key is passive safety. Rather than relying on active pumps, valves, and external power, passive safety systems use natural convection, gravity, and thermal mass to reduce dependence on active components and significantly extend the response window in accident scenarios. Fukushima was a failure of active cooling (power-dependent). SMR design philosophy is fundamentally different.

However: no SMR fleet has been commercially validated through repeated deployment under the U.S. NRC framework. (Individual cases exist outside this context, such as Russia’s floating nuclear plant and China’s HTR-PM, but the regulatory and deployment model differs from Western grid-scale SMR fleet deployment.)

NuScale is the most advanced SMR vendor on the NRC certification/approval track. Its 50MWe design received NRC design certification in 2023, and the 77MWe US460 received Standard Design Approval in 2025 [4]. GE Vernova’s BWRX-300 is under construction at OPG Darlington in Canada (2029 to 2030 target). And Oklo is pursuing a fundamentally different approach with a fast reactor that recycles spent nuclear fuel. In May 2026, the NRC approved Oklo’s Aurora Principal Design Criteria on an accelerated schedule [5].

[Figure 2: Large Reactor vs SMR Comparison]

Korea’s position: Team Korea

Among countries with nuclear construction track records, only three can credibly compete in Western markets: South Korea, France, and the United States. Russia and China are effectively excluded from Western markets. EDF lost the Czech Republic bid to KHNP.

South Korea is the only country to have completed a recent nuclear build (UAE Barakah, 4 APR-1400 units) on time and on budget. This track record was the decisive factor in winning the Czech Dukovany contract: $18.6B, two APR-1000 units [6]. The “Team Korea” consortium comprises KHNP (lead), KEPCO E&C (design), Doosan Enerbility (equipment/construction), KEPCO NF (fuel), and KEPCO KPS (maintenance) [6].

The EPC contract was signed on June 4, 2025 [7]. A Czech-Korean ministerial committee was established in February 2026 [8]. Construction permit target is 2027, groundbreaking 2029. Doosan Skoda Power has secured the turbine supply contract [9].

There is an important risk attached to the Team Korea export thesis, however. Following the 2025 IP settlement with Westinghouse, certain market access restrictions and/or royalty structures reportedly apply [10]. The specific terms are confidential, but Korean media and FT reporting have cited restrictions covering North America, the UK, Japan, Ukraine, and parts of the EU. Czech Dukovany proceeded as an exception within this settlement. Extrapolating EU and North American follow-on orders without a Westinghouse cooperation structure is not straightforward.

How has the market reflected this thesis? Doosan Enerbility’s 1-year return is +322.4% [11]. The market has finally started pricing “proven export capability.” Whether the Westinghouse risk is fully priced in remains uncertain.

Korean nuclear companies are fundamentally different investments from U.S. SMR companies in that they have actual construction track records. At the same time, they carry the unique risk of the Westinghouse IP structure.

[Figure 3: Global Nuclear Construction Pipeline by Country]

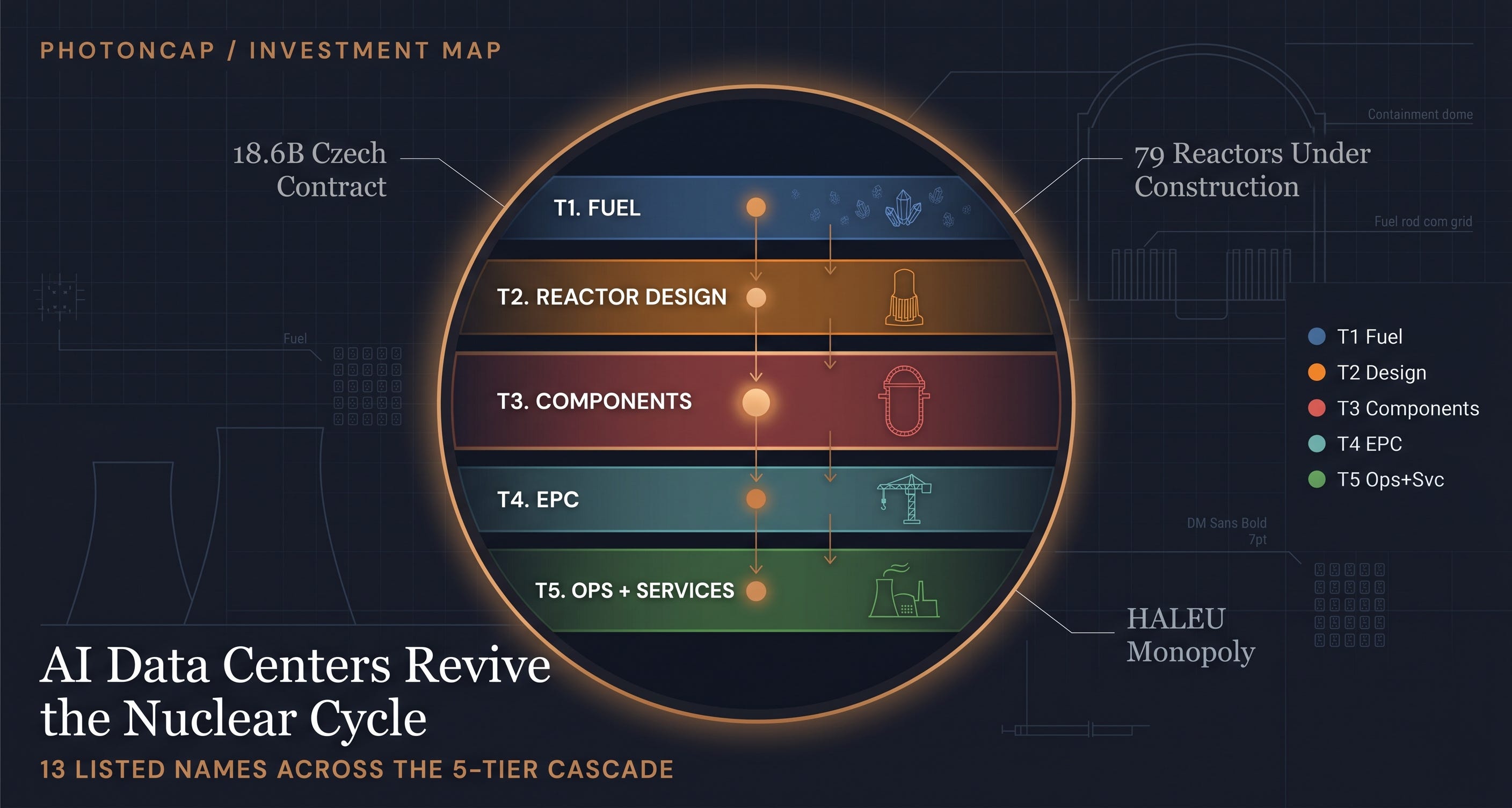

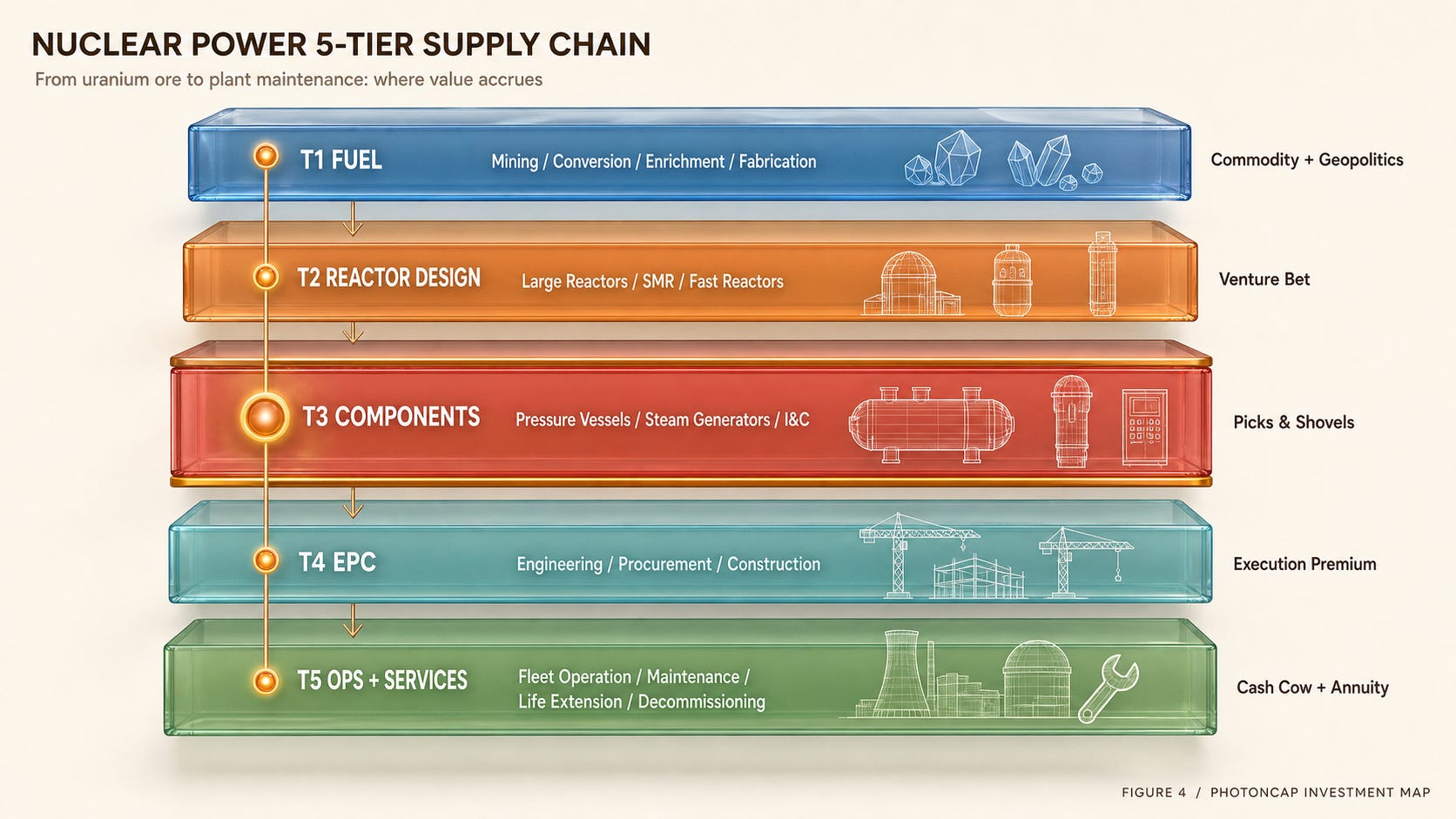

3. The 5-Tier Supply Chain

Deconstructing the nuclear cycle from an investment perspective yields 5 tiers.

T1 Fuel: Uranium mining, conversion, enrichment, fuel fabrication. The “raw material” of nuclear. According to the IEA, Russia accounts for roughly 40% of global enrichment capacity [12]. Western supply chain independence is the core thesis.

T2 Reactor Design: The reactor itself. From large reactors (APR, EPR) to SMRs (VOYGR, BWRX-300) and fast reactors (Aurora). NRC certification is the defining barrier to entry.

T3 Components: Pressure vessels, steam generators, instrumentation and control. ASME Nuclear-certified manufacturing facilities can be counted on one hand globally. “Qualification” is the bottleneck.

T4 EPC (Construction): Integrated engineering, procurement, and construction. Fewer than 10 EPC firms globally have nuclear construction experience. “Experience itself” is the bottleneck.

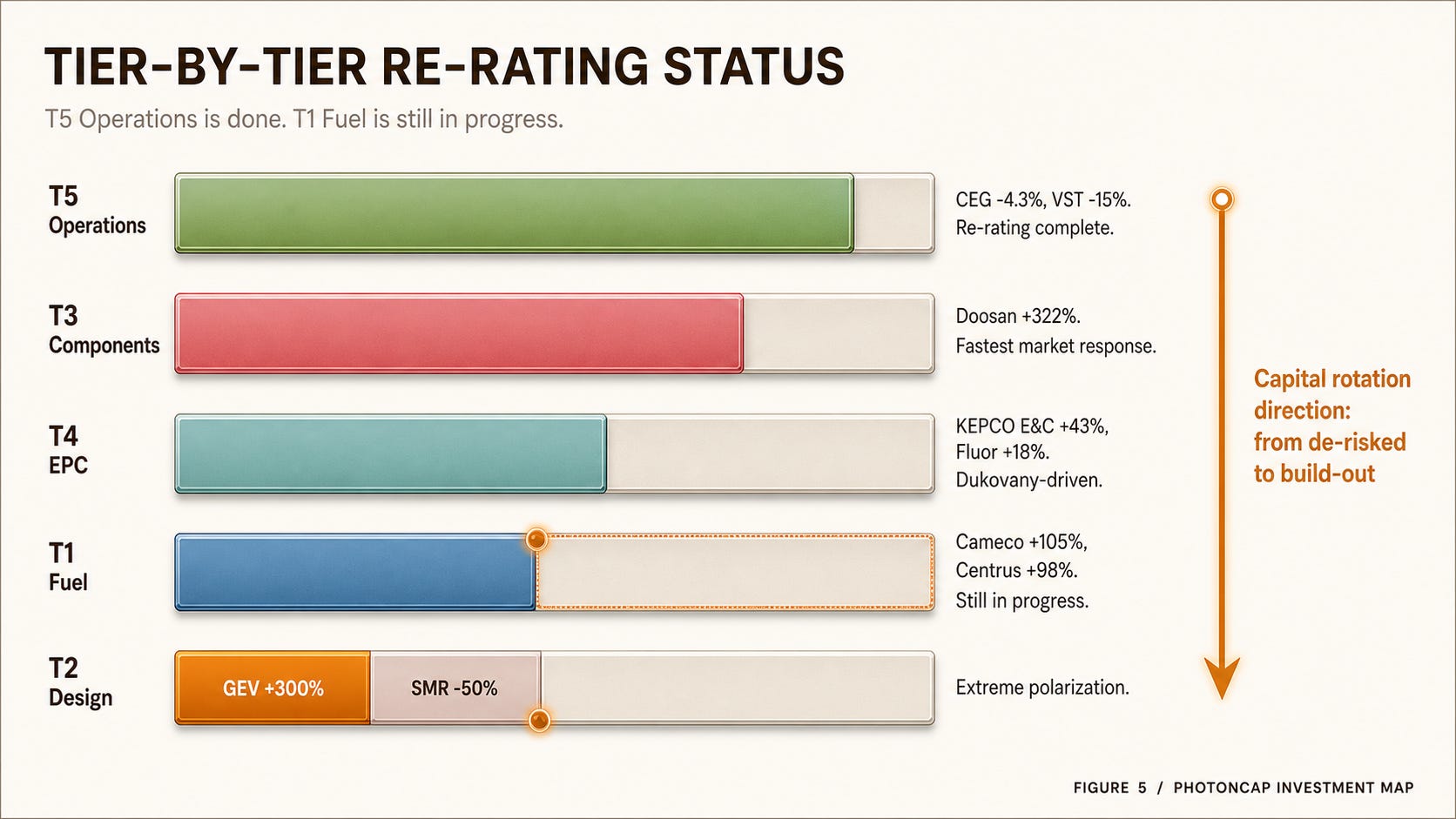

T5 Operations/Services: Plant ownership/operation + maintenance/life extension. The most stable cash flows, but the market appears to have already completed re-pricing. Constellation -4.3%, Vistra approximately -15%.

[Figure 4: Nuclear Power 5-Tier Supply Chain Value Map]

Investment character by tier:

T1 Fuel: Commodity + geopolitics. Uranium price and enrichment capacity constraints are drivers. T2 Reactor Design: Venture bet. NRC certification and first commercial operation are de-risking events. T3 Components: Picks and shovels. Regardless of which reactor design wins, components are needed. ASME certification is the moat. T4 EPC: Execution premium. Construction track record equals competitive advantage. T5 Operations/Services: Cash cow + annuity. Fleet revaluation is done. Recurring maintenance revenue is the next wave.

Actual 1-year returns make the re-rating pattern clear. T3 Components (Doosan +322%) and T1 Fuel (Cameco +105%, Centrus +98%) moved the most. T5 Operations (Constellation -4.3%) is resting. T2 Reactor Design is severely polarized: GE Vernova at +300% (as the AI power infrastructure anchor) versus NuScale at -50% (patience exhausted over zero commercial revenue).

The key: the market has repriced “nuclear renaissance” but has not repriced all 5 tiers evenly. Capital is rotating from T5 Operations toward T3 Components and T1 Fuel. If this rotation is not over, the remaining T1 bottleneck is where alpha sits.

[Figure 5: Tier-by-Tier Re-rating Status]

4. Framework Preview

Everything above is visible from public data. AI power demand revived nuclear. 13 listed companies sit across 5 tiers. Each tier’s re-rating speed differs.

What the paid section reveals is not simply a stock list, but which bottleneck remains under-reflected in price.

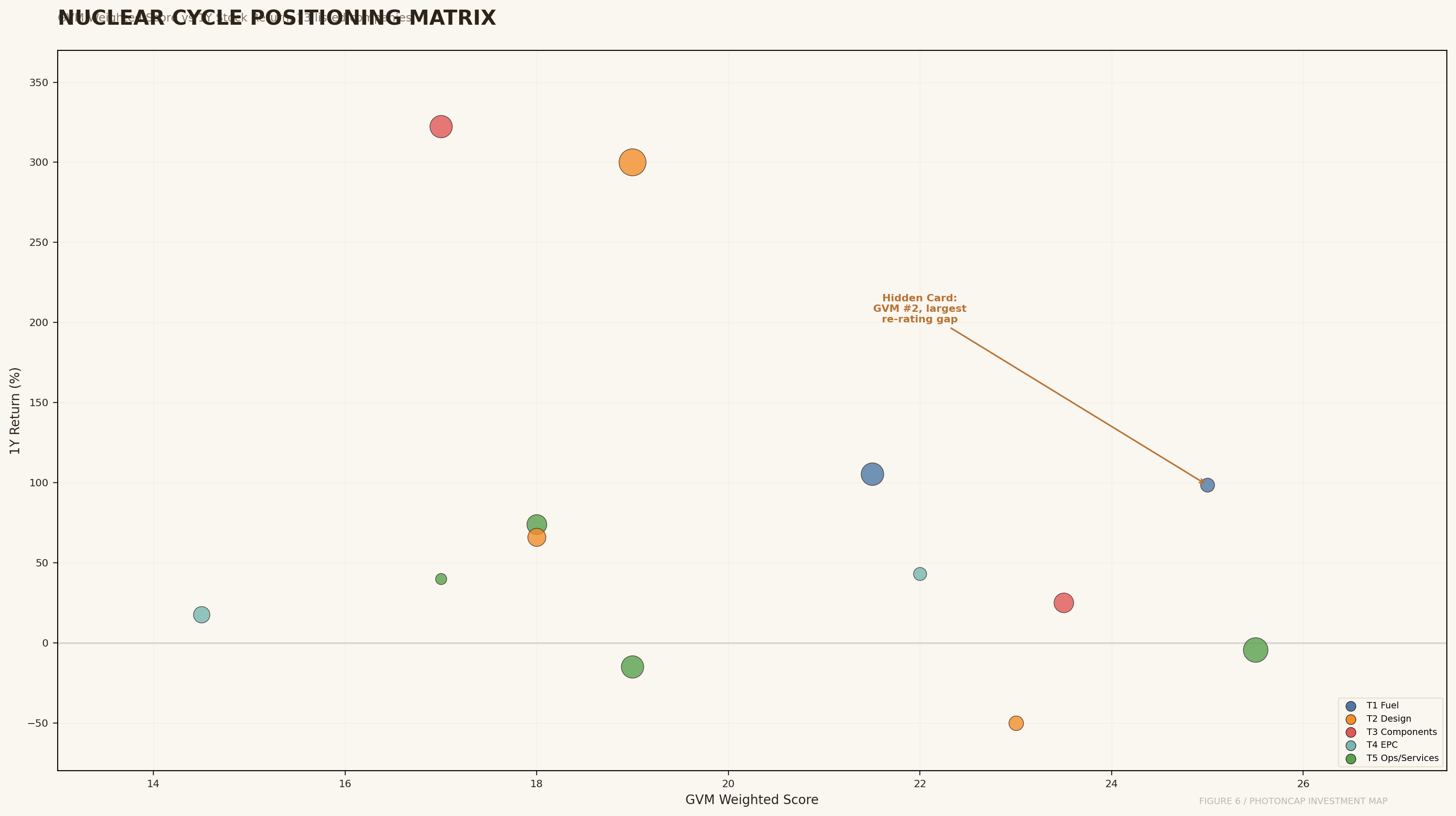

Scoring the 13 companies through the GVM framework yields 5 groups:

Group A: Toll Collector. Positioned to charge every participant in the cycle.

Group B: First Mover. Secured advantage through NRC certification or construction track record.

Group C: Execution Machine. Order-driven + recurring revenue. Team Korea core.

Group D: Venture Bet. Clear technical differentiation but no commercial track record yet.

Group E: Infrastructure Play. Not nuclear-pure but benefiting from the infrastructure cycle.

One of these 5 groups contains a Hidden Card. GVM weighted score ranks #2 overall, yet market cap is roughly 1/30th of #1. It has nearly doubled in the past year, and the gap still remains.

[Figure 6: Positioning Scatter Plot, Free Section (no names, Hidden Card dashed circle)]

Which 13 stocks. How the 5 groups map. Which company is the Hidden Card. This article answers all three.

One more thing: I have personally invested in or currently hold positions in 4 of the 13 companies covered in this map. Which ones and why are disclosed in the paid section.

Pricing update — effective June 3, 2026

PhotonCap started with a simple bet: that there’s demand for silicon photonics research that goes deeper than press releases and earnings recaps.

New pricing — effective June 3:

Monthly: $50/month (currently $30)

Annual: $500/year (currently $300)

Already a paid subscriber? Your rate is locked in permanently. Nothing changes for you.

If you’ve been considering subscribing, now is the time. Lock in the current rate before June 3.

Content offerings, format, and frequency may evolve over time as PhotonCap grows.

— PhotonCap