The Next Materials War in Silicon Photonics: Polymer EO Modulators, Who Wins?

Abstract

As of OFC 2026, organic electro-optic (EO) polymer modulators are simultaneously entering the PDKs of major SiPho foundries. Within two weeks, LWLG (Perkinamine) and NLM Photonics (Selerion) initiated integration at Tower, GlobalFoundries, and SilTerra. This article analyzes how organic EO polymers overcome the ~50 GHz bandwidth ceiling of silicon depletion modulators, the technical differences between Perkinamine and Selerion (guest-host vs crosslinkable thermoset glass), foundry-by-foundry PDK integration status, a fair comparison with TFLN (including CTE thermal stress concerns), and the hurdles remaining before commercialization. From an investment perspective, we map the value chain across LWLG (the only listed pure-play), TSEM, GFS, and ***, and present a H2 2026 event calendar.

Contents

Intro

Background: Why Silicon Alone Is Not Enough

The Materials Race: Perkinamine vs Selerion

Foundry Integration Status: Who Is Using Whose Material?

Hurdles Remaining Before Commercialization

Investment Implications

Closing

Intro

It has been a week since OFC 2026 wrapped up. One of the most striking themes at this year’s show in LA was organic electro-optic (OEO) polymer modulators.

On March 16 alone, three press releases dropped. NLM Photonics announced a 1.6T/3.2T SOH (Silicon-Organic Hybrid) PIC tapeout at GlobalFoundries (GFS) AMF HP process [1] and validation of SOH modulators on Tower Semiconductor’s (TSEM) PH18M platform via an MPW run [2]. On the same day, LWLG announced integration of its modulator platform into the GDSFactory PDK for GFS’s silicon photonics platform [3]. Two material companies opening PDKs at GFS and Tower simultaneously.

Five days earlier, on March 11, Lightwave Logic (LWLG) announced a development agreement with Tower Semiconductor [4]. And on March 3, it unveiled an EO polymer modulator platform available through a Luceda Photonics PDK on the SilTerra foundry [5].

Here is what happened in the span of two weeks: two organic EO material companies began integration at three SiPho foundries simultaneously.

I covered the LWLG-TSEM development agreement in a previous article [6]. Today, I am widening the scope to look at the organic EO polymer material category itself. Why these materials are getting attention now, who is competing with what technology, how foundries are moving, and what investment implications emerge from this trend.

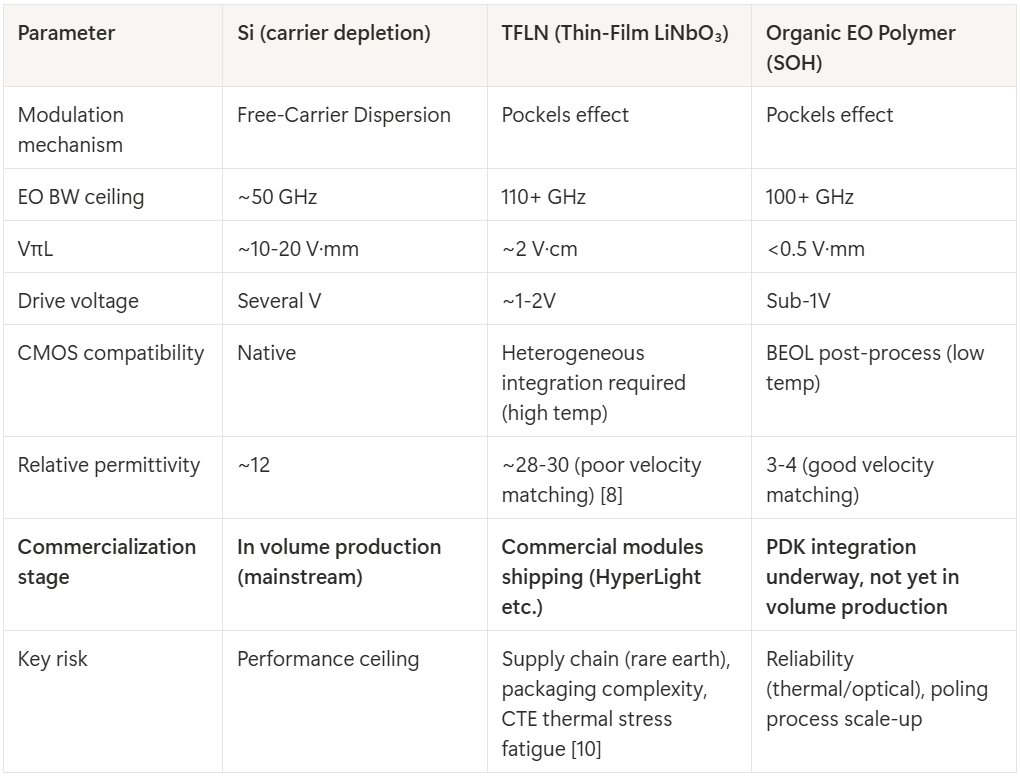

Core thesis: Organic EO polymer material companies are racing to secure PDK slots at major SiPho foundries, and the foundries are embracing this as an opportunity to expand their modulator menu. Organic EO polymers do not replace silicon. They extend silicon into performance territory that silicon alone cannot reach.

Background: Why Silicon Alone Is Not Enough

Before we jump in, a quick word on what “organic EO polymers” actually are. Most materials familiar in semiconductors and optoelectronics are inorganic: silicon, lithium niobate, InP, GaAs. These are crystalline materials with atoms arranged in regular lattice structures. They are well understood, stable, and thoroughly covered in textbooks. Polymers, by contrast, are carbon-based organic macromolecules. Think plastics. They can be deposited onto silicon wafers through solution processes like spin coating, and they process at low temperatures. The traditional weakness has been degradation under heat and light. The reaction “an organic material for optical modulators?” is understandable.

So why are SiPho foundries paying attention to this organic material now? Let’s start with the market context.

According to LightCounting Research estimates cited by LWLG CEO LeMaitre in the Q4 2025 earnings call (3/5), silicon photonics’ share of optical transceiver revenue rose from 10% in 2018 to 33% in 2024, and is projected to cross 50% for the first time in 2026 [7]. The 100G+ Ethernet optical transceiver and CPO market is expected to grow from ~$16.5B in 2025 to ~$26B in 2026, marking two consecutive years of 60% growth [7]. 1.6T transceiver revenue alone is projected to exceed $1B in 2026, with 3.2T volume production slated for 2028 [7].

Silicon photonics is taking over the transceiver market at a rapid pace. So why is there talk of “silicon alone not being enough”? The modulator’s physical limits.

To understand this article’s context, we need to start with how silicon photonics modulators work.

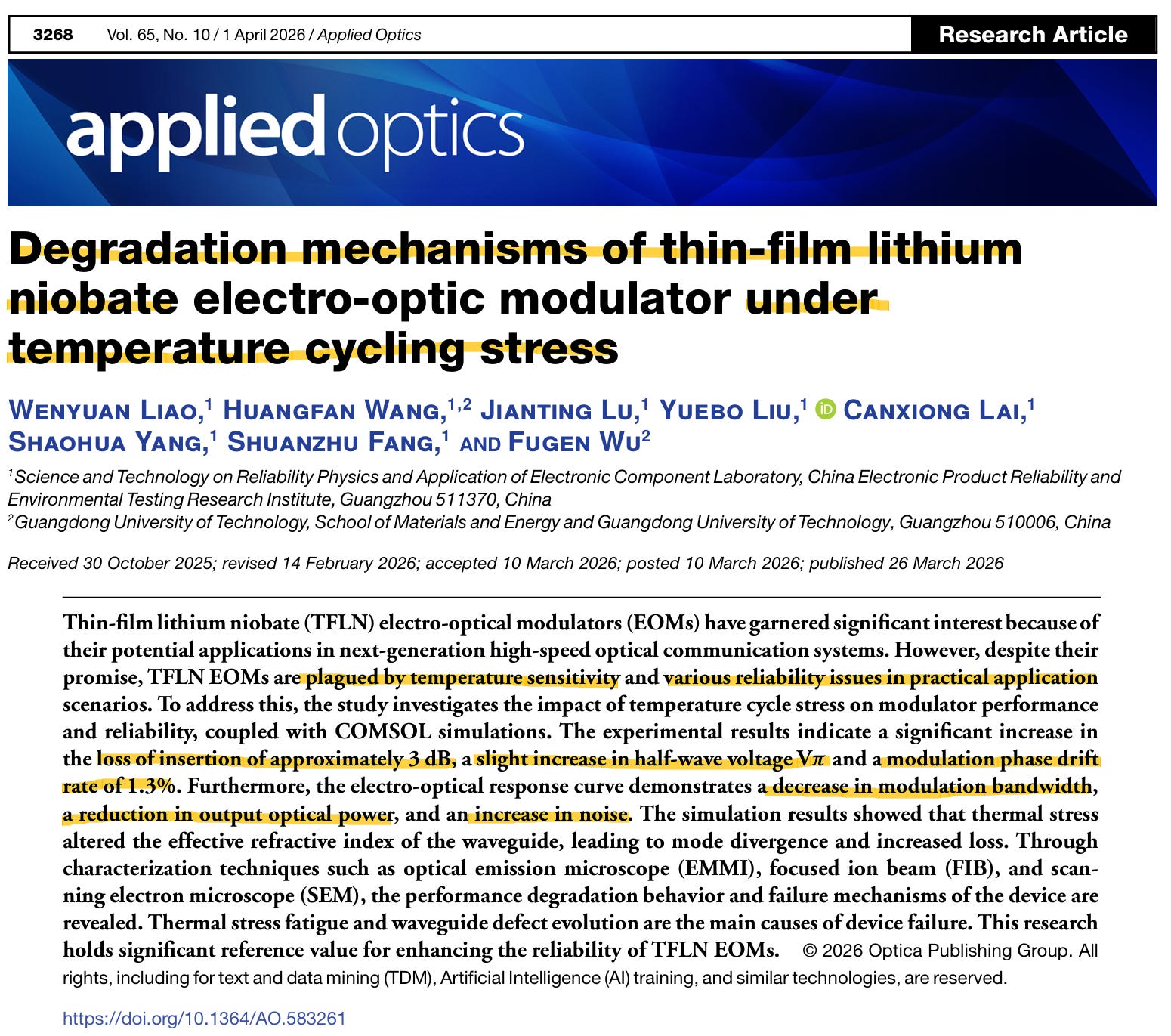

Most commercial silicon modulators today use carrier depletion. A reverse bias is applied to a PN junction, widening the depletion region, changing the free carrier density, and altering silicon’s refractive index to create phase modulation [8]. This is known as the Free-Carrier Dispersion (FCD) effect.

The problem is that this effect is inherently weak. Because the refractive index change (Δn) is small, you need modulator lengths of several mm and drive voltages of several volts to get sufficient phase shift. On top of that, FCD is not a pure phase modulation. It also produces electroabsorption, which degrades signal quality at high speeds [8].

As a result, silicon modulators hit an EO bandwidth ceiling around 50 GHz [8]. This limit comes from a combination of photon lifetime and RC time constant constraints. A comprehensive IEEE JSTQE review of SOH/POH modulator technologies reaches the same diagnosis [9]. Until now, that was fine. For 100G/lane, 50 GBaud PAM4 was sufficient. But 200G/lane and 400G/lane change the picture. Hitting 100 GBaud or even 200 GBaud PAM4 requires EO bandwidths above 100 GHz, and silicon depletion modulators simply cannot get there.

One point to make here: why drive voltage matters.

Power efficiency is a core metric in AI datacenter optical interconnects. The industry roadmap (OIF and others) targets around 5 pJ/bit for next-generation links. High modulator drive voltage means high driver IC power consumption, which eats into the total transceiver power budget. Ideally, you want a modulator that can be driven directly at CMOS logic levels (sub-1V). That is how you eliminate or minimize the driver, which is the path to LPO (Linear Pluggable Optics).

So what are the alternatives?

Both TFLN and organic EO polymers use the Pockels effect (linear change in refractive index proportional to electric field) instead of silicon’s FCD. FCD changes carrier density to alter the refractive index, an “indirect” approach. The Pockels effect changes the refractive index directly through the applied electric field. The response is inherently fast, and pure phase modulation is possible, which means better signal quality. But silicon crystals have centrosymmetry, so the Pockels effect does not exist in silicon. To use it, you need to place a non-centrosymmetric material like LiNbO₃ or organic EO polymers on top of silicon.

TFLN (Thin-Film Lithium Niobate) is already commercializing rapidly through companies like HyperLight, and it has real strengths in bandwidth and material stability. As an inorganic crystal, it does not have the thermal degradation or photo-oxidation issues that organic materials face. That is a significant advantage.

But TFLN is not completely free from reliability concerns either. A study published in Applied Optics in March 2026 by CEPREI (China Electronic Product Reliability and Environmental Testing Research Institute) is interesting. They applied temperature cycling tests (-30°C to 95°C) to TFLN MZMs, and after 168 cycles, insertion loss spiked by ~3 dB, exceeding the failure criterion [10]. The root cause is residual stress accumulation from a ~15x CTE mismatch between the LN thin film (CTE ~7.5x10⁻⁶/K) and the SiO₂ cladding (CTE ~0.5x10⁻⁶/K). This stress alters the waveguide’s effective refractive index through the stress-optic effect, causing mode divergence and light leakage [10].

Some caveats apply. The tested device specs (Vπ 3.5V, BW 20 GHz) are significantly behind the current TFLN state of the art (VπL < 2 V·cm, BW > 100 GHz). Only 1 out of 3 samples failed. And it is unclear whether the observed defects were generated by temperature cycling or were pre-existing fabrication artifacts. Still, this study provides counter-evidence to the assumption that TFLN, being an inorganic crystal, is “inherently safe.” If organic EO polymer’s reliability risks are photo-oxidation and depoling, TFLN’s reliability risk is CTE-mismatch-driven thermal stress fatigue. Both sides carry their own reliability challenges.

Beyond reliability, TFLN has other structural disadvantages. LiNbO₃ crystal supply is concentrated in China, and its high relative permittivity (~28-30) makes RF-to-optical velocity matching difficult [8]. Most importantly, from a foundry’s perspective, TFLN integration requires high-temperature processing and heterogeneous material handling that are hard to reconcile with existing CMOS lines.

Organic EO polymers take a different approach. A slot waveguide is formed on the silicon wafer, and EO polymer is deposited into the narrow slot. This is called the SOH (Silicon-Organic Hybrid) platform [8]. The polymer is deposited via spin coating or solution processing at below 150°C, which means it can be inserted at the BEOL (Back-End-Of-Line) stage of a silicon foundry [8][11]. Since you build the SiPho chip first and then add the polymer in the final step, contamination risk to the foundry line is relatively low.

LWLG uses an analogy with OLEDs. Just as organic emitting materials in OLED displays are deposited onto TFT backplanes, EO polymers are deposited onto SiPho wafers as a “post-process” [11]. From a foundry’s perspective, this is an option to boost modulator performance one level up while keeping the existing SiPho process line intact.

Key takeaway: In the 400G/lane era, the physical limits of silicon depletion modulators (~50 GHz, multi-V drive) are becoming clear. Organic EO polymers offer a Pockels-effect-based path to high-speed (100 GHz+), low-voltage (sub-1V) modulation through a CMOS BEOL-compatible process.

The Materials Race: Perkinamine vs Selerion

Two companies are pushing the hardest to commercialize organic EO polymers right now. Lightwave Logic (LWLG) with Perkinamine, and NLM Photonics with Selerion. Both target hybrid integration with silicon photonics, but their technical approaches and go-to-market strategies are distinctly different.