[Investment Map] 20 Companies in the Humanoid Cycle: From Rare Earth Magnets to Vision Language Action

$NVDA $MP $6324.T and 17 more across the humanoid supply chain. Customer anchors $TSLA, Figure AI

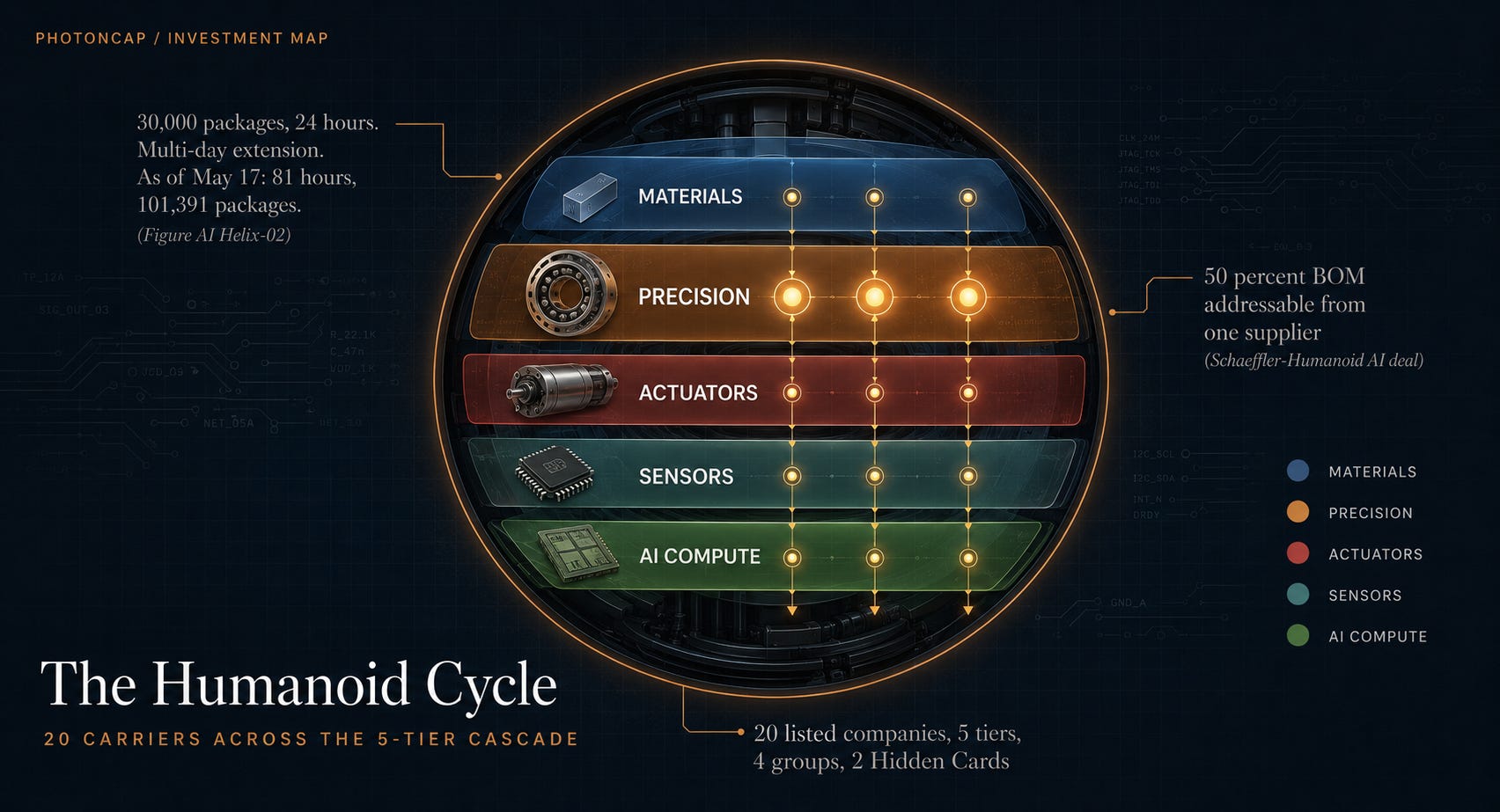

On May 13, 2026, two events landed on the same day in the humanoid cycle. Figure AI livestreamed Helix-02, three robots autonomously sorting 30,000 packages in 24 hours with zero failures. The livestream extended into a multi-day run. As of May 17, the counter showed 81 hours and 101,391 packages. The same day, Schaeffler announced two parallel deals with UK humanoid startup Humanoid AI, deploying up to 1,000 to 2,000 robots at Schaeffler global plants by 2032 plus a separate 5-year actuator supply agreement covering seven-digit (1M plus) joint actuators through 2031. This is an Investment Map of the 20 listed companies sitting on the cascade behind 11 humanoid makers globally. The thesis is that the cycle alpha is in the component cascade, not in the robot maker race. PhotonCap GVM (Global Value Map) scores 20 names across 5 axes (Technology Barrier, Supply Concentration, Bottleneck Value, Verifiable Incumbency, Catalyst Proximity) and reveals 2 Hidden Cards positioned for re-rating. Among the five tiers, Tier 2 Precision Components is the bottleneck where automotive valuations and humanoid component exposure intersect.

Contents

24-Hour Livestream and the Fremont Pivot: Investment Hook

The 5-Tier Component Cascade Behind One Humanoid

Beyond the Public Framework: 4 Groups and the Hidden Card Label

Identifying the 20 Companies and the Multiple Gap vs Auto Components

4-Group Classification, Differentiation, and Company-by-Company Analysis

Scenarios, Monitoring, and Closing

References and Sources

1. 24-Hour Livestream and the Fremont Pivot: Investment Hook

On the evening of May 13, 2026, Figure AI CEO Brett Adcock posted a short sentence on X: “Watch a team of humanoid robots running a full 8-hr shift at human performance levels. Fully autonomous running Helix-02.” In the video, three Figure 03 humanoids stood beside a conveyor belt, flipping packages so their barcodes faced down, pressing plastic-wrapped boxes so the scanner could read the labels, and walking to charging stations autonomously when batteries depleted. Business Insider reported that the stream passed 24 hours and 30,000 packages with over 3 million views and zero failures [2]. Seoul Economic Daily later reported that the run had extended to 81 hours and 101,391 packages as of May 17 [35]. TechRadar reported more than 10 million views on the original X video [34]. Business Insider has separately reported that Amazon and GXO have tested humanoid robots in warehouse settings, while Microsoft is better framed as a Figure AI investment context rather than a confirmed warehouse deployment [4]. This was one of the clearest public demonstrations yet that humanoid robots can perform a full warehouse-style shift without teleoperation.

[Figure 1: Humanoid 5-Tier Supply Chain Cascade]

[Figure 2: Humanoid BOM Value Distribution per Robot]

The robot maker landscape shows 11 companies spread globally across the same cycle. In the US, Tesla (Optimus), Figure AI (Figure 03), Boston Dynamics (Atlas, acquired by Hyundai Motor Group in 2021, with planned deployment at Hyundai Georgia plant starting 2028) [33], Agility Robotics (Digit, Amazon fulfillment and GXO Logistics paid pilots), and Apptronik (Apollo, Mercedes-Benz partnership plus Google DeepMind collaboration). In China, Unitree (G1 and H1, the lowest-price line) and UBTech (Walker S, with deployments at BYD and Geely automotive plants). Norway has 1X Technologies (NEO, OpenAI investment), Canada has Sanctuary AI (Phoenix, Magna partnership, relatively small scale), the UK has Humanoid AI (the one-year-old startup that emerged with the May 13 Schaeffler thousand-unit deal), and South Korea has Rainbow Robotics (RB-Y1 dual-arm humanoid plus the Hubo series, Samsung Electronics 35 percent subsidiary, descended from the KAIST HUBO program, the clearest pure-play public humanoid stock in Asia) [30]. These 11 companies have different robot designs and different customers, but even if the winners differ, the demand pool of actuators, reducers, magnets, sensors, and edge compute largely repeats. Supplier mix and geography do vary by platform. Tesla weights toward Sanhua and Leader Drive in China, Apptronik and Boston Dynamics lean toward automotive incumbents like Schaeffler and Allegro, Rainbow Robotics leans toward SPG and the Korean cluster. Vendor share per maker shifts, but the 20-supplier demand pool fills from the sum of all robot makers.

Earlier in 2026, Tesla added a separate capex signal. On January 29, Reuters reported that Tesla planned roughly $20 billion in 2026 capex and was shifting Fremont and Gigafactory Texas factory space toward Optimus production [32]. The Optimus Gen 3 reveal was originally expected in Q1 2026 but has slipped toward mid to late 2026 [36]. Goldman-linked supply-chain reporting has framed Chinese suppliers’ pre-order capacity buildout as a key signal to watch [7].

And on May 13, the exact same day as the Figure livestream, another signal landed on the same cycle. German automotive component centenarian incumbent Schaeffler announced two parallel deals with UK humanoid startup Humanoid AI. First, plans to deploy up to 1,000 to 2,000 robots at Schaeffler global manufacturing sites by 2032 (with phased deployment timing). Second, a separate 5-year actuator supply agreement valid through 2031, under which Schaeffler will supply more than half, over 1 million units, of Humanoid’s wheeled platform joint actuator demand [6][31]. An automotive component company started taking humanoid robots as a customer.

That is the investment question. Not who wins among robot makers (Tesla vs Figure vs Unitree). The question is which 20 component suppliers under that race will be re-rated first. The cycle is beginning to cross from prototype demos toward first commercial production. And in past tech cycles, the supply chain almost always gets re-rated before the platform maker. The same pattern that played out when launch providers were not the first to re-price in the LEO satellite cycle (III-V epi wafer and OISL terminal optics names like IQE, Coherent, AXT moved first), and when a single cable-laying vessel became a bottleneck for one hyperscaler in the subsea cable cycle, plays out here too. In this Investment Map we will look at the 20 companies sitting under that cascade.

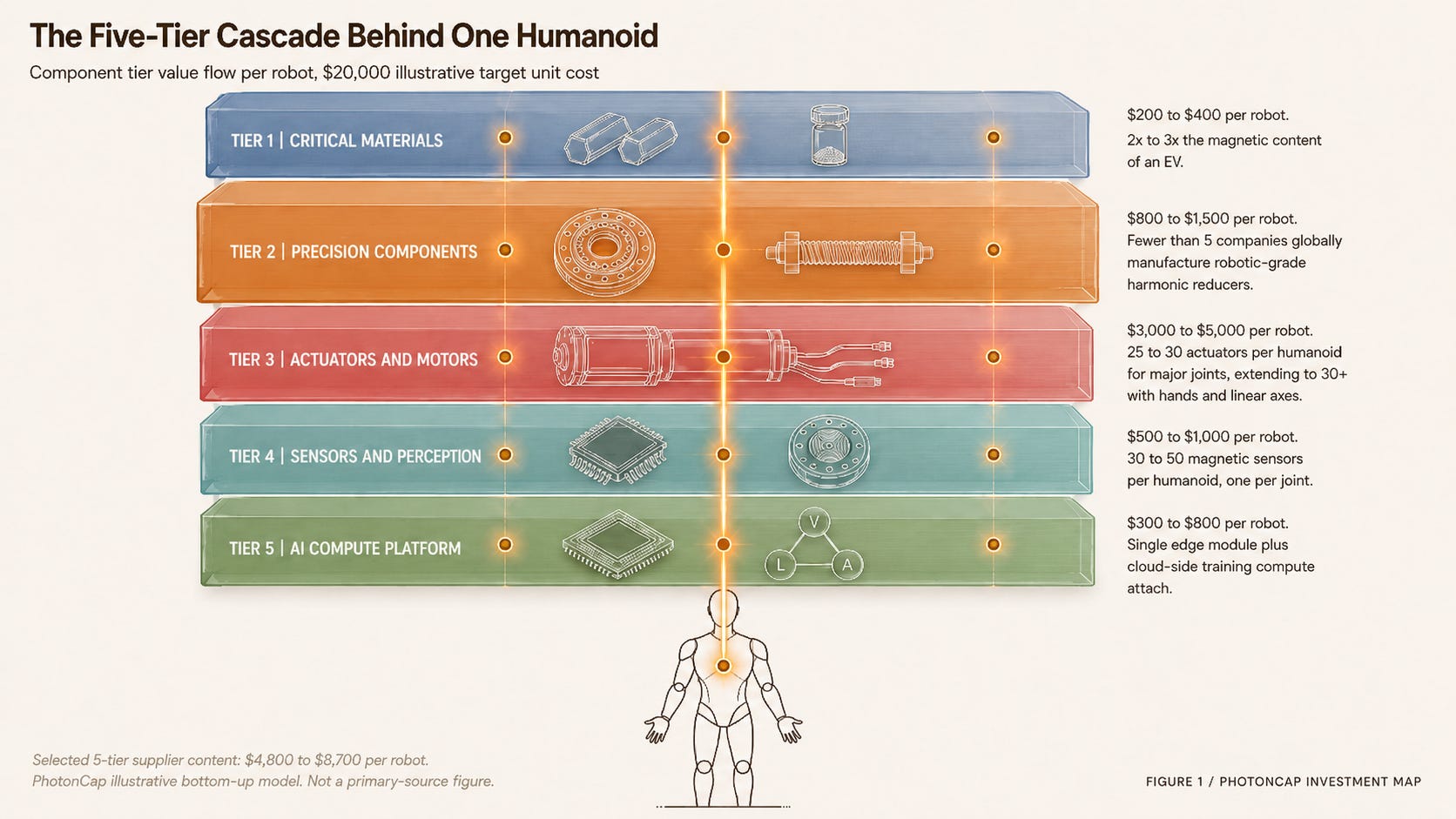

2. The 5-Tier Component Cascade Behind One Humanoid

Before naming who wins, look at the cascade. A humanoid robot is, structurally, a stack of 5 vertical tiers. From the surface down to the unit-economics floor:

Tier 1: Critical Materials. The starting point is rare earth permanent magnets. PhotonCap estimates roughly 2 to 3 kg of NdFeB (neodymium iron boron) magnet content per humanoid depending on actuator count and hand dexterity, 2x to 3x the magnetic content of a typical EV per MP Materials management framing. The 25 to 30 major joint actuators, extending to 30+ with hands and linear axes, each require high-torque motor content, and torque density determines robot weight, agility, and battery life. China currently controls 89.6 percent of the global processing share of rare earths, structurally upstream. MP Materials (US, Mountain Pass mine plus Texas magnet plant), Lynas Rare Earths (Australia plus Malaysia), JL Mag Rare-Earth (China sintered NdFeB leader), and USA Rare Earth (Oklahoma plant commissioning in 2026) are the four listed companies in the Tier 1 layer. All four have already partially re-rated on rare earth supply chain narratives, but the humanoid demand uplift is yet to be priced in [5][7][11][12][24].

Tier 2 Precision Components are 5 companies, the actual bottleneck position in humanoid supply chains. Harmonic Drive Systems (6324.T, Japan) is the global incumbent in strain wave reducers, market cap ~$2.7B, 1Y +16% YTD. Leader Drive = Green Harmonic (688017.SS, China) makes the same strain wave reducers as primary supplier to Tesla Mexico, market cap ~$4.7B, +89% since KOID inception. Nabtesco (6268.T, Japan) is the global #1 in RV cycloidal reducers, strong in industrial robots, market cap ~$3.4B, 1Y +20%. Schaeffler (SHA.DE, Germany) is the integrated incumbent in bearings plus planetary roller screws plus rotary actuators, market cap ~$9.4B, 1Y +90 to 100%. SPG (058610.KQ, South Korea) is the only domestic player producing all three precision reducer types (planetary, strain wave SH, and cycloidal SR) in volume [28]. Even by global standards, it is a rare integrated challenger that combines planetary, strain wave, and RV lines into one portfolio (Germany Neugart specializes in planetary, Japan Harmonic Drive in SH, Japan Nabtesco in RV). Per Korean media reporting, SPG supplies 22 reducers (20 for joints plus 2 for wheels) to Rainbow Robotics RB-Y1 dual-arm humanoid [28]. Market cap ~$2.2B (KRW 3.0T), 1Y +420% [26][27][28].

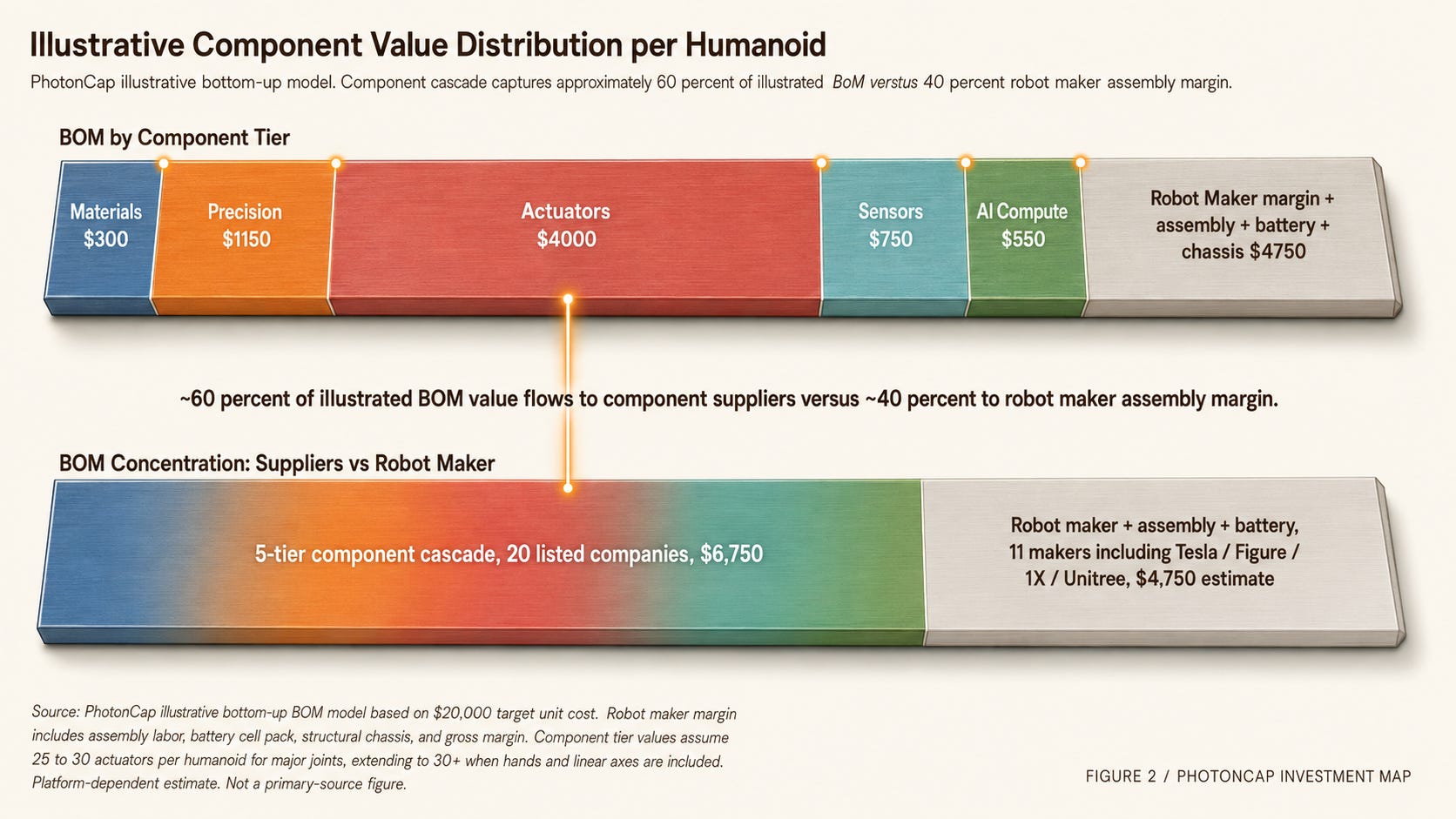

PhotonCap illustrative bottom-up BOM model (model-based estimate, not a primary source, range varies with actuator count and hand dexterity per platform): Magnet ($200 to $400) into Reducer plus screw ($800 to $1,500) into Smart actuator ($3,000 to $5,000) into Sensor ($500 to $1,000) into Edge AI compute ($300 to $800). Component cascade total approximately $4,800 to $8,700 per robot (about 24 to 44 percent of the $20K target unit cost). The rest is robot maker assembly plus battery plus structural chassis plus gross margin. Component cascade vs robot maker assembly margin ratio is approximately 60:40 in the illustrated model. That is, supplier-side capture is roughly 60 percent of illustrated BOM.

Tier 3 Actuators and Motors are 6 companies. Sanhua Intelligent (002050.SZ / 2050.HK, China) has crossed from HVAC and EV thermal into linear actuators for humanoid, market cap ~$15.7B. Tuopu Group (601689.SS, China) covers rotary actuators plus dexterous hands plus electronic skin, market cap ~$15.2B, +33% YTD. Inovance (300124.SZ, China) is China’s #1 servo motor maker, supplying Unitree and UBTech upstream, market cap ~$22.3B. Nidec (6594.T, Japan) is the global incumbent in BLDC plus coreless motors, market cap ~$30B. Moog (MOG.A, US) crosses aerospace actuator capability into humanoid joints, market cap ~$9.7B, +83% since KOID inception. ROBOTIS (108490.KQ, South Korea) holds the global academic robotics standard position with its Dynamixel servo motor (used by NASA Astrobee, Boston Dynamics research labs, MIT/Stanford/CMU labs) and is crossing into Tier 2 reducer territory with its self-developed Cycloid gear DYD. Capacity expansion is underway with the Uzbekistan plant construction. Market cap ~$3.5B (KRW 4.76T), 1Y return +809.71%, the strongest outlier among the 20 listed names [29].

Tier 4 Sensors and Perception are 3 companies. TDK (6762.T, Japan) covers magnetic sensors plus image sensors plus IMU (with the InvenSense acquisition), market cap ~$60B. Melexis (MELE.BR, Belgium) is the global #1 in magnetic position sensor ICs, market cap ~$2.6B. Allegro Microsystems (ALGM, US) has a near-monopoly in BLDC motor current sensor ICs and a strong position in magnetic position sensor ICs, market cap ~$8.35B. Humanoid robots need 30 to 50 magnetic sensors per unit, one per joint, more than 2x the sensor density of an EV. None of these three companies have yet had robotics revenue priced in. Their P/E multiples are still in the automotive cyclical range (12 to 20x).

Tier 5 AI Compute, 2 companies, the platform layer. NVIDIA (NVDA, US) is the mega-cap covering Jetson edge SoC plus the GR00T VLA foundation plus the Cosmos world model, market cap ~$5.5T. Qualcomm (QCOM, US) covers the RB6 edge robotics platform, mega-cap ~$216B.

That is why the component suppliers may capture the earlier public-market alpha, even if the 11 robot makers (Tesla / Figure / Boston Dynamics+Hyundai / Agility / Apptronik / 1X / Unitree / UBTech / Sanctuary AI / Humanoid / Rainbow Robotics) capture the final system margin. The robot maker’s gross margin pool sits on final assembly plus software plus system integration, and the substantial portion of physical BOM value (in the PhotonCap illustrative model, component cascade is about 60 percent and robot maker side about 40 percent) flows to these 20 component suppliers. The cycle alpha is in the cascade, not in the robot maker race.

3. Beyond the Public Framework: 4 Groups and the Hidden Card Label

So far the picture is public information. The next layer separates the public framework from the investable framework.

The real question shifts. Among the 20 listed companies sitting on this cascade, who is fully priced and who is still auto-priced? And specifically, which 1 to 2 names in Group B Auto-Priced Hidden Layer are sitting on the largest delta between current valuation and humanoid revenue mix exposure?

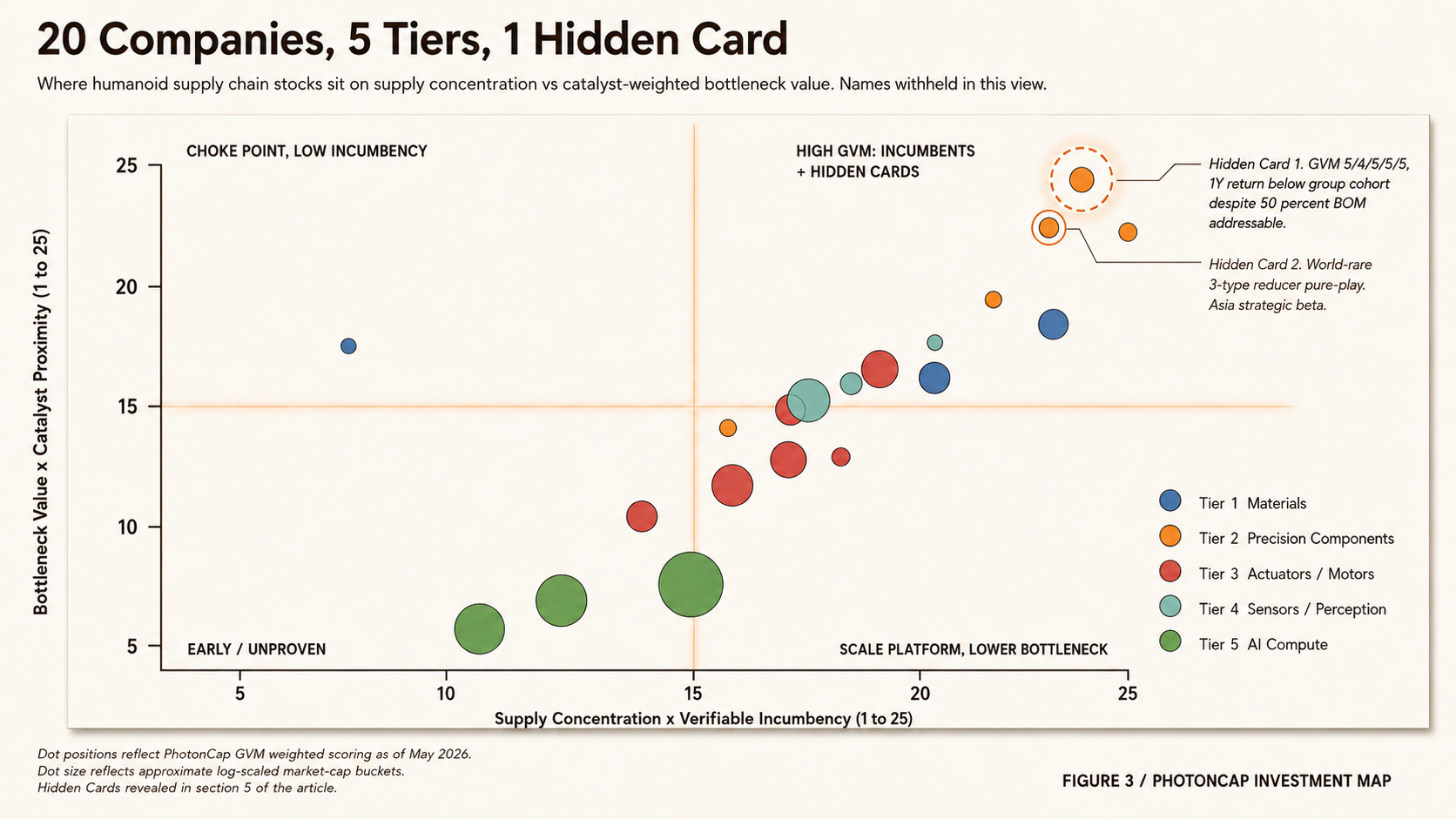

[Figure 3: GVM Positioning Scatter (names withheld)]

This article scores the 20 names along PhotonCap’s GVM framework (Technology Barrier, Supply Concentration, Bottleneck Value, Verifiable Incumbency, Catalyst Proximity) and groups them into 4 thesis categories: Group A Fully Priced, Group B Auto-Priced Hidden Layer, Group C Material Choke Pure-play, Group D Platform Beneficiary.

Three thesis frames open in this article.

Why does Hidden Card 1 sit in the same Tier 2 Precision Components position as Schaeffler? Specifically, the GVM scoring breakdown of why that position is a Visibility Discount Zone.

Why is the geographic split (US 6 / China 5 / Japan 4 / South Korea 2 / Europe 2 / Australia 1) almost identical to the LEO satellite supply chain pattern? What that implies for re-rating sequence.

Why does the Tier 2 Precision Components bottleneck position trade at 1x to 5x P/S while equivalent positions in semiconductor (ASML, Tokyo Electron, Applied Materials) trade at 8x to 12x P/S? The robotics premium gap.

Among the 20 names, the company sitting in the largest valuation gap right now is hidden under just one ticker. Hidden Card 1 is the single most-mispriced name in the Tier 2 Precision Components position. Hidden Card 2 is the secondary hidden position with rare integrated 3-type reducer pure-play exposure.

Tesla Optimus Gen 3 reveal (originally expected in Q1 2026, slipped toward mid to late 2026) / Figure 03 follow-on deployment (rumored 2026 H2) / Goldman Sachs supply chain re-survey (scheduled). Which names are most directly exposed to each catalyst.

If you would like the full identification, valuation gap analysis, GVM scoring breakdown, scenario mapping, and monitoring points, the paywall opens below.