InP Makes the Light. Fiber Carries It: Same Cycle, Different Bottleneck

$GLW $APH 5803.T 5801.T 5802.T 601869.SS 010170.KQ | Global AI Datacenter Fiber Supply Chain Analysis

Abstract

The price of G.652.D bare fiber in China went from RMB 15.5 per fiber-km in May 2025 to RMB 81.9 in May 2026, roughly 5x in a year [1]. Not because silica ran short. Because AI datacenters are adding optical paths faster than preform and high-count cabling capacity can keep up. And this shortage does not move on one global price. In the US, local production and hyperscaler qualification set the price. In China, domestic supply and demand is pushing bare fiber up. Japanese makers sit between the two, raising prices on high-density cable. In the last piece I covered the paradox that the more silicon photonics wins, the more InP light sources sell. This one is about the road the light has to travel. I convert Korea’s 8.4GW and the global pipeline into fiber strand counts and core-km, and break down which company takes which value pool. One preview: even as transceivers jump from 800G to 1.6T, fiber demand does not fall. Why that happens is the back half of this article. The tickers this time: $GLW, $APH, Fujikura (5803.T), Furukawa (5801.T), Sumitomo Electric (5802.T), YOFC (601869.SS), and Taihan Fiberoptics (010170.KQ).

Contents

190GW Does Not Flow Into One Supply Chain

Where the 16x and 36x Multipliers Actually Come From

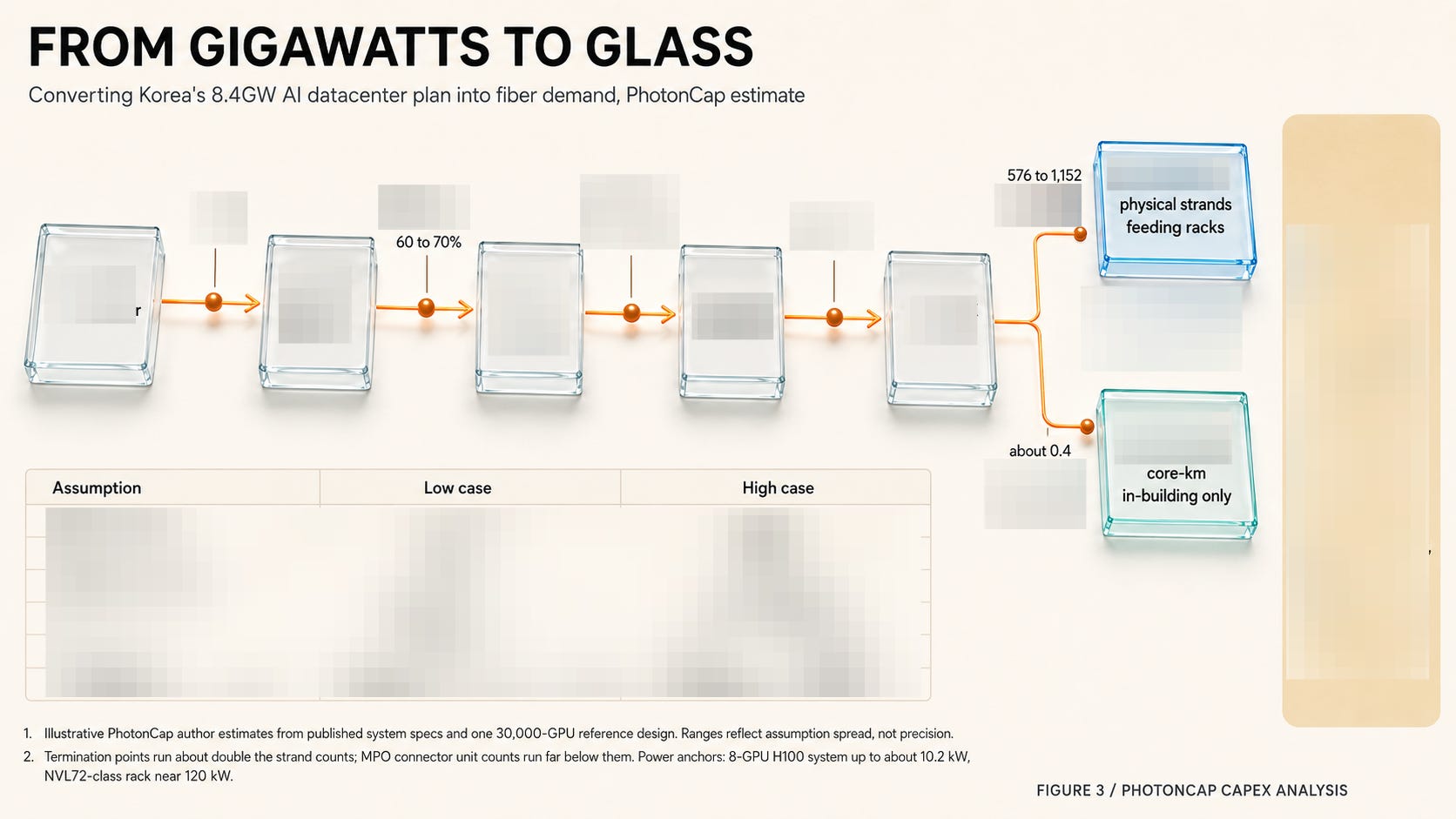

Converting GW into Core-KM

The Regional Supply Map: The Spec Is Open, the Door Is Shut

Same Shortage, Different Price Zones

The Fiber Paradox

Scenarios

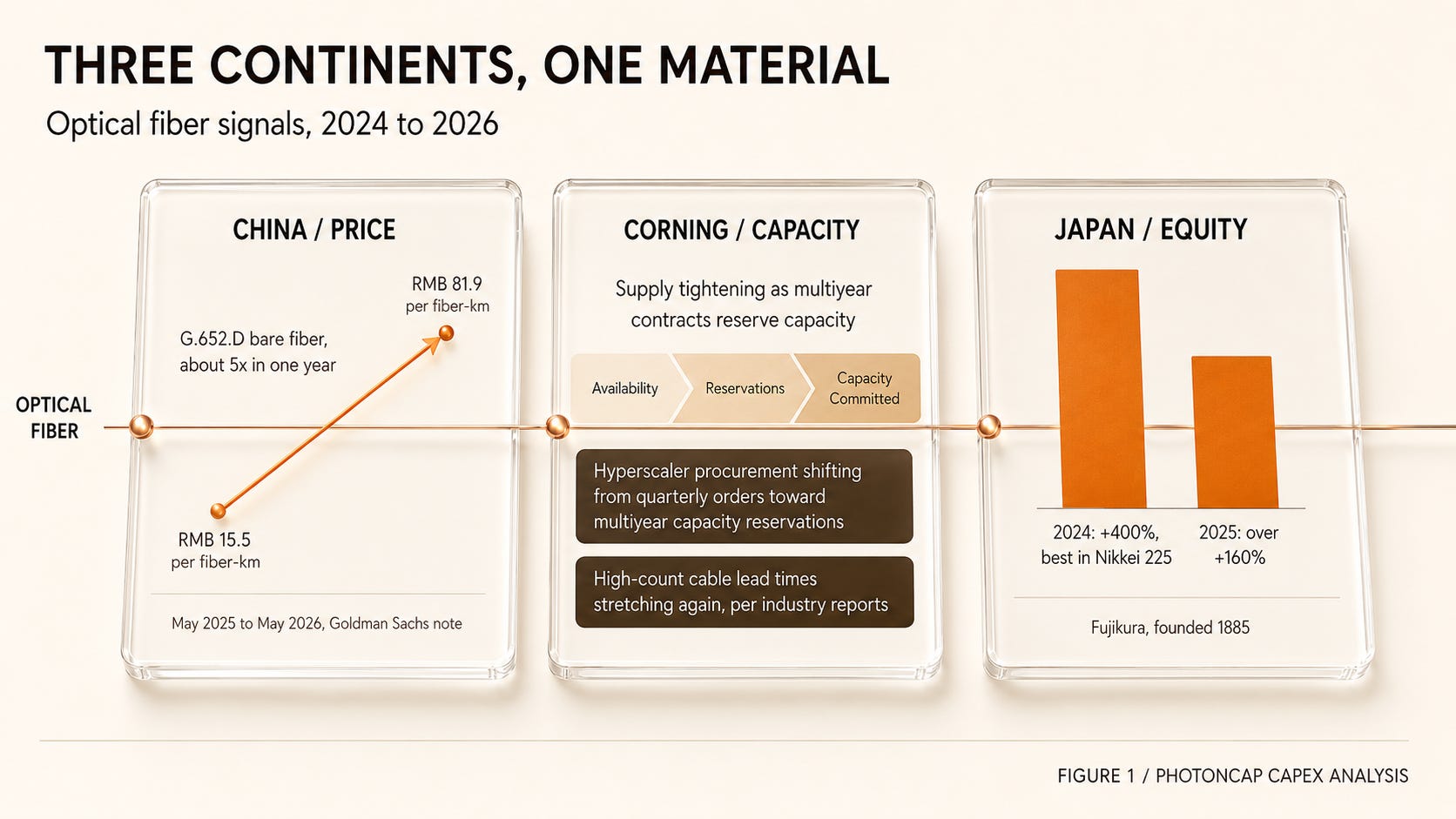

Optical fiber that sold for RMB 15.5 per fiber-km now sells for RMB 81.9.

That is Chinese G.652.D bare fiber, the standard single-mode fiber before cabling. Goldman Sachs flagged the number in a June note on YOFC: roughly 5x between May 2025 and May 2026 [1].

What makes a 5x move in fiber strange is not the raw material. It is the production structure. Optical fiber is fused silica, SiO2. Silicon and oxygen make up three quarters of the Earth’s crust by mass, and even the ultra-high-purity synthetic silica used for fiber is not a scarce mineral. The money sits in the process, in synthesizing and drawing the preform, not in the ingredients. Which is why fiber spent decades at a few dollars per fiber-km, one of the cheapest components in telecom infrastructure, and why it became the poster child for cutthroat bidding during the Chinese oversupply of the 2010s. A 5x print in that market is not a raw-material shock. It means datacenter demand, rising carrier tender prices, and a production mix shift toward higher-value products are squeezing existing capacity all at once [1].

And this is not just a China story. In the US, industry participants are warning that fiber availability will tighten sharply in 2026 [2]. In Japan, Fujikura, the best-performing stock in the Nikkei 225 in 2024 at +400% [3], climbed more than 160% again in 2025 [4]. This is a company that started in 1885 making silk and insulated wire [3]. The same material is heating up on three continents at once, and it is not a wafer or a laser. It is a strand of glass. A component the industry spent two decades treating as a throwaway line item is suddenly the thing hyperscalers sign multiyear contracts to secure.

Figure 1: Three Continents, One Material - Fiber Price, Supply, and Stock Signals

In the last piece, after watching UMC and Tower both announce 300mm silicon photonics expansions on the same day, July 14, I wrote that the next bottleneck was not wafers but InP light sources. Silicon cannot make light.

The More Silicon Wins, the More InP Sells: Why UMC and Tower Both Expanded 300mm on the Same Day

But that piece had one seat left deliberately empty. The light a laser makes has to travel somewhere. Between transceiver and transceiver, rack and rack, building and building. That entire road is glass.

If InP is the bottleneck on the side that makes light, fiber is the bottleneck on the side that carries it. Same cycle, different physical location, and as we will see, a different supply structure and a different way prices move. InP was a narrow, deep bottleneck, wafers and epi, with suppliers you could count on one hand. Fiber looks like the opposite: a wide, shallow bottleneck. Companies make it on three continents, and yet prices are printing 5x and hyperscalers are locking up years of capacity in advance. Why that happens is the problem this article works through.

Bare fiber up 5x in China, supply warnings in the US, and in Japan the 2024 Nikkei champion Fujikura up another 160% the following year. Raw-material scarcity cannot explain these signals. What you need to watch is supply, demand, and capacity.

1. 190GW Does Not Flow Into One Supply Chain

Start with demand. Sightline Climate tracks 777 large datacenters and AI factories above 50MW announced since 2024, a project pipeline of roughly 190GW [5]. It is an announcement-based count, so much of it is still on paper, and the same dataset carries a caveat: of the 16GW slated to come online in 2026, only about 5GW is actually under construction [5]. Still, the number is more than enough to read direction. The reason to look at this 190GW by region is that the fiber supply chain is tied to regional qualification and production footprints. Why it is tied that way is a paid-section question. Here, the point is simply that there are three separate invoices.

United States. The core of demand. Corning’s Optical Communications revenue grew 36% year over year in Q1 2026 to around $1.85B [6], and enterprise sales grew 58% year over year in Q3 2025, driven largely by strong adoption of Corning’s Gen AI products [2]. The shape of the contracts has changed too. In January, Meta signed a multiyear agreement with Corning worth up to $6B and took the anchor-customer seat at the Hickory, North Carolina plant [7]. On June 8, Amazon announced a multiyear, multibillion-dollar supply agreement with Corning [8]. In between, the Q1 earnings call disclosed two more hyperscaler contracts of similar size and duration to Meta’s [7]. Components that used to be bought quarter by quarter are now being reserved years of capacity at a time. When a buyer locks in a specific plant as its anchor customer, it is no longer purchasing a commodity. It is renting a supply chain. The CEO of STL’s optical networking business says the US needs to add another 213 million fiber-miles by 2029. With roughly 160 million miles installed today, that means laying more than everything laid so far, inside four years [2].

Korea. On June 29, the government announced an 8.4GW AI datacenter plan with SK (5GW), GS (2.4GW), and Naver (1GW). 550 trillion won, groundbreaking targeted for the first half of 2028, staged operation from 2029 [9]. On top of that, on June 8 Naver and NVIDIA announced an AI factory anchored at GAK Sejong: 55MW in the first half of 2027, then 100MW, 200MW in 2028, and eventually gigawatt class [10]. One gigawatt is about 4x the maximum capacity of GAK Sejong [10]. An announcement is not a groundbreaking, but a national demand block has landed on the invoice in gigawatt units. And 8.4GW is more than 4% of the 190GW global pipeline Sightline tracks [5], one of the largest single-country plans anywhere.

China. Even with access to leading-edge US GPUs locked behind licenses and running at a trickle [11], the build continues on domestic accelerators, and that demand is part of what sits behind the 5x bare fiber move [1]. YOFC guided H1 2026 net profit up 711% to 914% year over year [12]. A fiber company guiding profit up eight-fold in a single year was not a sentence anyone would have written before this cycle. And unlike the equity moves in the US and Japan, this one is earnings, not multiple expansion.

All three regions announce demand in gigawatts. What differs is the supply chain. These three invoices go to three different sets of factories.

The 190GW pipeline is one number, but from fiber’s point of view it is three invoices, from the US, Korea, and China, each handed to a different supply chain.

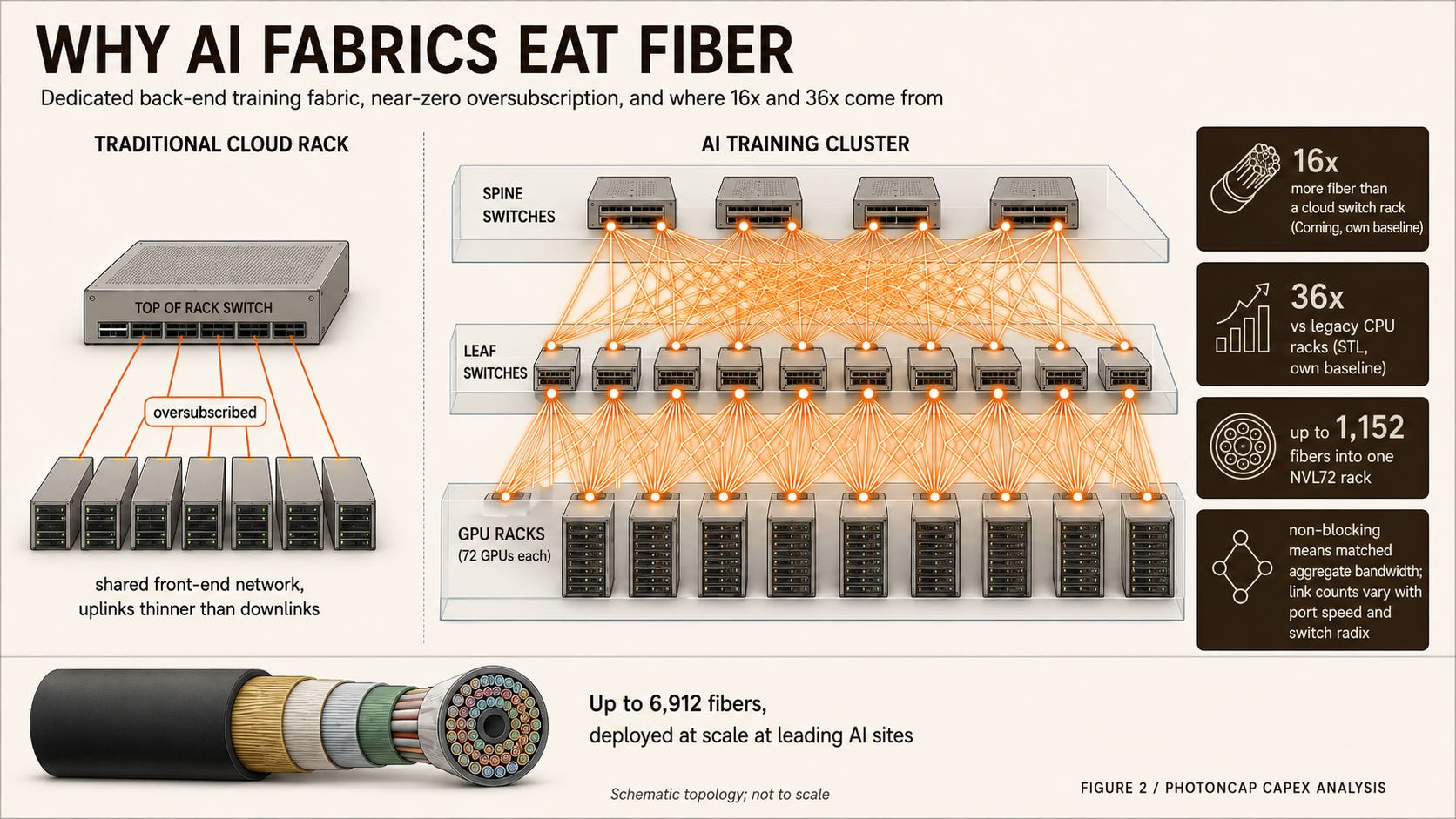

2. Where the 16x and 36x Multipliers Actually Come From

Network topology decides how much fiber an AI datacenter eats.

Cloud datacenters already carry heavy east-west traffic between servers. What changes in an AI training cluster is not the existence of east-west but its intensity. A dedicated training back-end fabric gets built separately from the front-end network, every GPU gets a high-speed NIC, and oversubscription gets pushed toward zero. A near non-blocking design means the spine-facing uplink bandwidth matches the total GPU-facing downlink bandwidth of the leaves. That is a bandwidth statement, not a link-count statement; actual link counts depend on port speeds and switch radix. And as clusters grow and tiers get added, aggregation links keep stacking on top of the GPU-facing links.

That is where the vendor multipliers come from. One caveat first: these multipliers are vendor estimates with different baselines. Corning’s head of fiber and cable says a 72-GPU node like NVL72 needs 16x more fiber than a traditional cloud switch rack [2]. STL’s CEO says an AI rack needs roughly 36x more than a legacy CPU rack [2]. Different denominators, so you cannot merge them into a single “16x to 36x” range. What they share is the conclusion that the order of magnitude changes whichever baseline you pick. AFL, the cable assembly house, gets more concrete in its reference architecture: up to 1,152 fibers feed a single NVL72 rack, and leading AI sites are deploying ultra-high-count cables that pack 6,912 fibers into one jacket [13]. Telecom cables run tens to a few hundred fibers. This is a different class of product. And the number of companies that can even build this class of cable is small. Folding and rolling ribbons to pack thousands of fibers into one jacket is each maker’s weapon in its own right, and it is where the commodity story about fiber quietly stops being true.

Figure 2: Why AI Fabrics Eat Fiber - Back-End Fabric, Oversubscription, and Vendor Multipliers

The signal that this layer has been promoted to an investment target has already fired. NVIDIA made four direct photonics investments this year: Coherent, Lumentum, and Marvell in March, $2B each, and then the fourth on May 6 was Corning. Per the official announcement, the deal bundles a multiyear commercial and technology partnership with a 10x expansion of US optical connectivity capacity, three new plants in North Carolina and Texas, and more than 3,000 jobs [14]. On the equity side, NVIDIA paid $500M for warrants (15M shares at $180 plus a 3M-share pre-funded warrant) that could ultimately give it a position worth up to roughly $3.2B if fully exercised [15]. Separately, Jensen Huang described an additional multibillion-dollar prepayment to help fund Corning’s new US factories. The first three companies make and process light. Only the fourth builds the road the light travels on. I covered the structure and meaning of that deal in a separate piece in May.

Coherent, Lumentum, Marvell, and Now Corning: NVIDIA’s 4 Photonics Bets and the Path of Light

Coherent, Lumentum, Marvell, and Now Corning: NVIDIA’s 4 Photonics Bets and the Path of Light

NVIDIA made four direct investments into photonics companies in 2026. Coherent and Lumentum got $2B each on March 2, Marvell got $2B on March 31, and on May 6 Corning got a $500M warrant deal plus a multi-year commercial partnership. The first three sit in the transceiver, laser, and DSP layers, the companies that generate, control, and interface with light. The fourth one, Corning, makes the medium that light actually travels through: optical fiber, cable, and connectors. This article walks through why NVIDIA’s fourth bet went to a different layer, and why the connectivity layer matters as much as the transceiver layer.

So reading gigawatt announcements as fiber demand is not a metaphor. It is arithmetic. Gigawatts set the accelerator count, accelerators set the rack count, and topology multiplies the racks. Every step in that chain is a number you can put a range on, which is exactly what the next section does.

That is as far as public sources take you. In the paid section, I convert this demand into actual strand counts and core-km, work through why a market that looks like a standardized commodity keeps new suppliers out, and then calculate why the 1.6T transition does not shrink fiber demand. The last question matters most. Like the Silicon Paradox in the InP piece, there is one result here that runs against intuition. One hint up front: the answer lives in how fast clusters are growing, not in the transceiver roadmap.