Did Wolfpack Actually Analyze POET’s Technology?

10 Pages, 44 Footnotes, Zero Lines of Technical Analysis

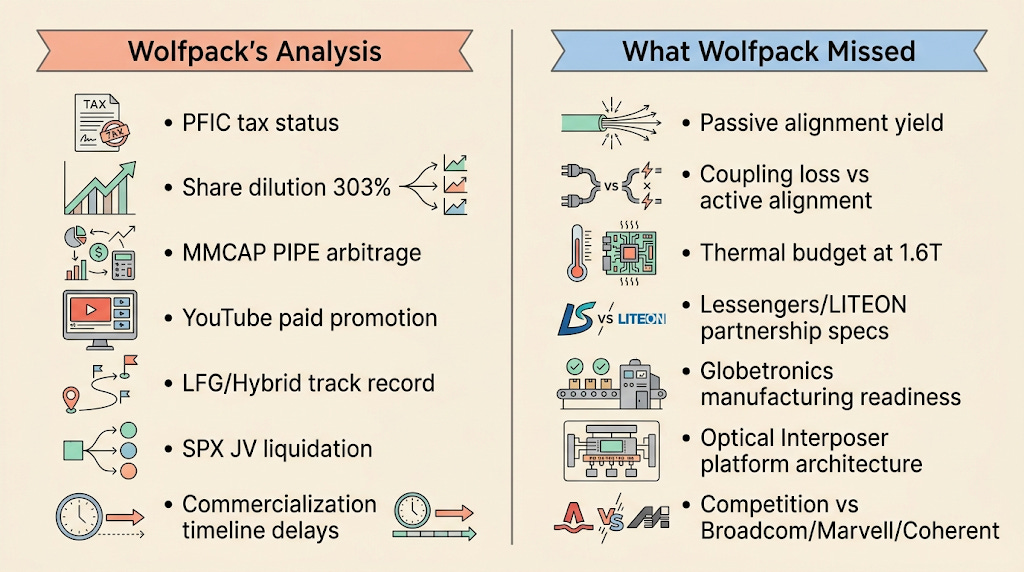

Wolfpack Research published a short report on $POET. Ten pages, 44 footnotes, zero lines of technical analysis. The PFIC tax issue and share dilution are separate matters worth examining on their own. This article reviews the report’s core claim of “seven business pivots” from an engineering perspective only, and presents five technical questions the short seller should have asked.

Contents

Intro

Are “Seven Pivots” Technically Accurate?

What Is the Optical Interposer Platform?

Five Technical Questions the Short Seller Should Have Asked

Closing

References & Sources

1. Intro

A ten-page short report with 44 footnotes. SEC filings, 13G amendment histories, tax code provisions, YouTube video links. All meticulously sourced. But zero lines of technical analysis. A short report on a semiconductor company that doesn’t discuss semiconductor technology once.

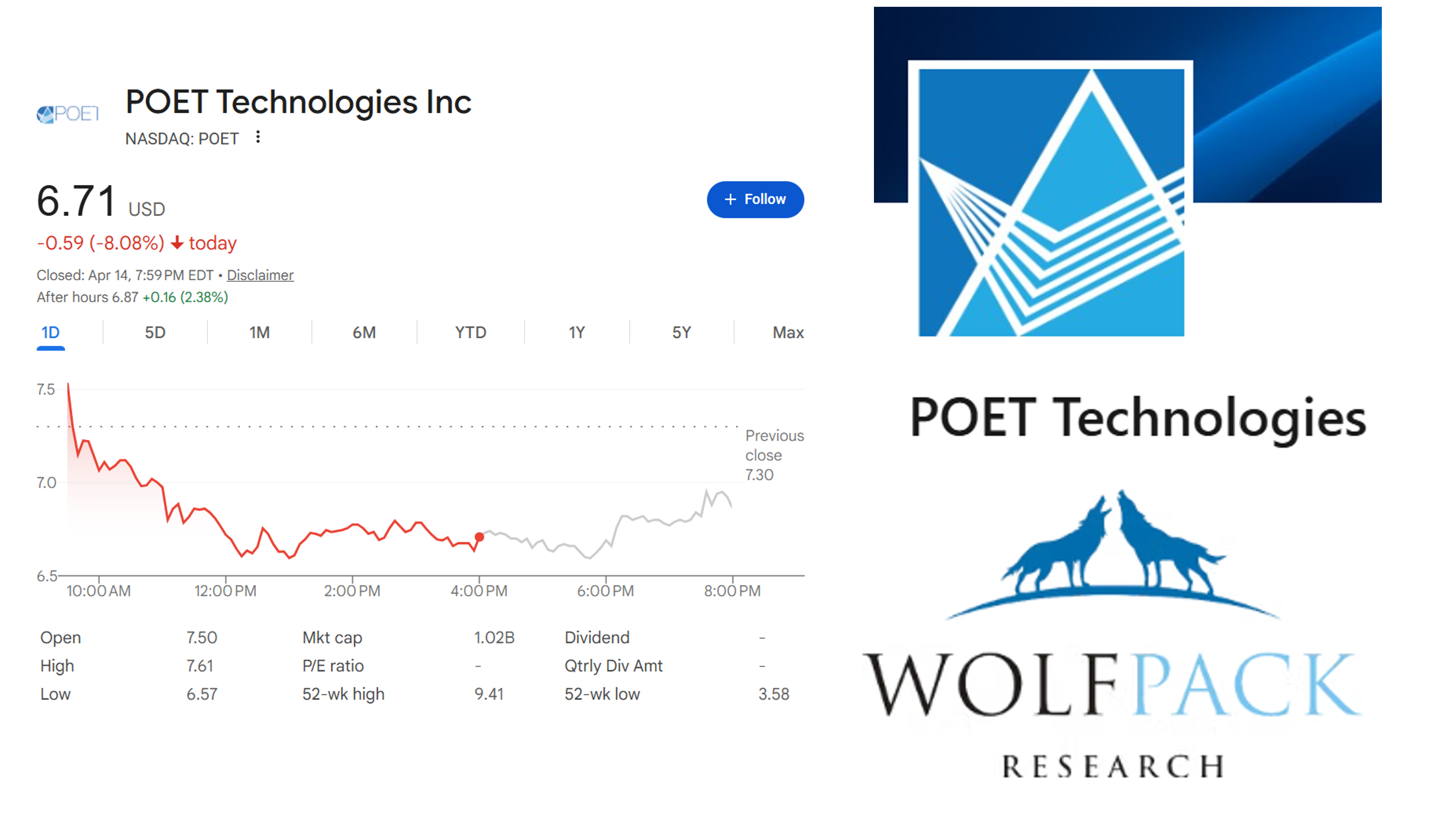

This is Wolfpack Research’s short report on POET Technologies, published on April 14.[1]

The report attacks on two main axes. One is the PFIC (Passive Foreign Investment Company) tax issue, and the other is share dilution combined with paid stock promotion. Both are claims worth independent scrutiny, and the PFIC numbers in particular come from audited financial statements, so they are not something to dismiss lightly.

But this article won’t cover those.

This article examines Wolfpack’s “seven pivots” claim from an engineering perspective only. This is not a defense of POET, nor is it an endorsement of the short seller. It fills in the part that was missing from a report that analyzed a technology company without analyzing its technology.

2. Are “Seven Pivots” Technically Accurate?

Wolfpack claims POET has undergone seven business pivots in the past decade.[1] Here is their list, verbatim:

Monolithic GaAs semiconductors (until 2017)

LIDAR for autonomous vehicles (2018)

IoT (2020)

5G interconnects, PON/GPON (2020)

Medical devices, DenseLight (2017 to 2019)

VR/AR (2018)

AI Infrastructure (present)

Laid out chronologically, it looks damning. The narrative of “a company that just swaps signboards to chase whatever is hot” writes itself.

The problem is that this list was compiled by extracting keywords from IR materials without understanding the underlying technology architecture.

POET’s core technology is the Optical Interposer, a wafer-level PIC (Photonic Integrated Circuit) platform. Depending on what laser you place on top and what detector you attach, the same platform can produce a LIDAR engine, a 5G PON engine, or an 800G/1.6T engine for AI data centers.

Here is an analogy. TSMC used to fabricate smartphone application processors. Now it fabricates AI accelerators. Nobody calls that “a business pivot.” The foundry platform stayed the same. What changed was the design placed on top of it. POET works the same way. The application layer on top of the Optical Interposer changed, but the underlying platform technology was never scrapped and rebuilt.

It is true that POET has frequently shifted its target application markets. And it is also true that revenue has been nearly nonexistent through that process ($2.3M cumulative since 2020).[1] That is a legitimate criticism. But framing it as “seven pivots” is the result of not distinguishing between a platform technology and its application markets.

The transition from monolithic GaAs to InP/Si hybrid is the same story. That is not a pivot. It is the evolution of a materials platform. In the semiconductor industry, materials transitions driven by performance and cost requirements are natural technological progression, not a change in business direction. The DenseLight divestiture was a structural decision to go fab-light (a strategy of using external foundries instead of owning fabrication facilities), which reduced capex risk.

Key point: Wolfpack’s “seven pivots” list is a chronological extraction of IR keywords, not a platform technology analysis. The underlying technology, the Optical Interposer, has not changed. The application markets did.

3. What Is the Optical Interposer Platform?

Since the Wolfpack report did not cover the technology, here is a brief overview.

Building an optical communication module requires lasers, modulators, photodetectors, and waveguides connecting them all. The traditional approach is to manufacture each of these components separately and then assemble them by precisely aligning each one (active alignment). Because you need to couple light into an optical fiber thinner than a human hair, this alignment process is slow and expensive.

POET’s Optical Interposer takes a different approach. The waveguides and alignment structures are fabricated at the wafer level in advance. Active components like lasers and detectors are then placed on top, and the light couples automatically through the pre-built structures. This is called passive alignment.

Think of it like a LEGO baseplate with pre-molded grooves. You place the component into the groove and it snaps into position. The traditional method is like using a microscope to manually position each piece. POET’s method is placing it into a slot that was designed to fit.

The theoretical advantages are clear.

Assembly cost reduction: Less active alignment equipment and shorter process times. Scaling: Hundreds or thousands of engines can be fabricated simultaneously at the wafer level. Multi-product flexibility: Different laser/detector combinations on the same interposer yield different products. This is why LIDAR, 5G, and AI engines can all come from the same platform.

The critical point here is that theoretical advantages working in production are a separate question entirely. And that question is exactly what Wolfpack should have asked.

Key point: The Optical Interposer is a wafer-level PIC platform based on passive alignment. Because different application layers can be placed on the same platform, targeting multiple markets is a property of the platform technology, not a “pivot.”

4. Five Technical Questions the Short Seller Should Have Asked

The Wolfpack report focused on the fact that “POET hasn’t generated revenue” while ignoring the technical question of “why.” Revenue failure at a technology company comes from one of two causes: the technology doesn’t work, or the technology works but commercialization hasn’t happened.

These two have completely different investment implications. The first is a permanent problem. The second is a matter of time and execution.

A real technical analysis would have addressed these five questions.

Q1. Does passive alignment achieve production-grade yield?

The core risk of passive alignment is coupling loss. Active alignment minimizes loss by measuring optical power in real time and fine-tuning position. Passive alignment relies on mechanical precision, so wafer process accuracy directly determines yield.

POET has not publicly disclosed specific production yield numbers. This is the most important unanswered question.

Q2. How does coupling loss compare to competing approaches?

Active alignment-based modules typically manage coupling loss below 1dB. Whether POET’s passive alignment reaches this level, or whether there is a trade-off, is the key question. If passive alignment lands at 1.5 to 2dB, then the calculation becomes whether assembly cost savings offset the performance gap.

This data has also not been publicly disclosed. If the short seller had demanded these numbers, the report would have been far more powerful.

Q3. What is the thermal budget when scaling from 800G to 1.6T?

Going from 800G to 1.6T means either higher lane rates or more lanes. Either way, thermal density increases. The question is whether POET’s Optical Interposer can handle this heat, particularly whether thermal crosstalk becomes a problem when EMLs (Electro-absorption Modulated Lasers) and driver ICs sit on the same interposer.

POET is co-developing a 1.6T 2xDR4 optical transceiver module with Lessengers, targeting Q2 2026 for samples.[2] If those samples actually ship, they will provide the first data point on thermal performance.

Q4. What are the actual specs of the Lessengers 1.6T 2xDR4 engine?

2xDR4 is an architecture with 4 lanes at 200G each (PAM4) to make 800G, bundled in pairs to reach 1.6T. What needs verification: actual modulation speed per lane, extinction ratio (the contrast ratio between light on and off states), BER (bit error rate) performance, and power consumption.

Currently available information is at the architecture level. Measured specs will only be available after Q2 samples.

Q5. What is the manufacturing integration readiness at LITEON/Globetronics?

POET announced a strategic collaboration with LITEON Technology in March 2026 to co-develop next-generation optical communication modules.[3] Prototype target is late 2026 with production planned for 2027. Separately, POET is building wafer-level assembly and test lines at Globetronics in Malaysia,[4] close to its long-term wafer foundry partner Silterra Malaysia.

The question here is: does the Globetronics line actually have the equipment and processes to perform passive alignment assembly for POET’s Optical Interposer? Is wafer-level test (WLT) capability in place? Is there a Known Good Die (KGD) screening system established?

This is the critical bottleneck for production transition and the most direct indicator of whether POET’s “fab-light” strategy actually works.

5. Closing

Wolfpack’s PFIC analysis and dilution structure analysis may be independently valid. The numbers come from audited financial statements and present real tax risks for U.S. investors. That is outside the scope of this article, and readers should evaluate it separately.

But analyzing a technology company without a single line on its technology means half the analysis is missing. The “seven pivots” framing is a product of not understanding the difference between a platform technology and application markets. The fact that words like passive alignment, coupling loss, and thermal budget do not appear once in a ten-page report is the evidence.

Being technically skeptical about POET is entirely reasonable. There is no production yield data. Measured specs have not been disclosed. And commercialization timelines have been repeatedly delayed. A short report built on those points would have been far more effective.

Whether POET’s technology works or not will be determined by the Q2 Lessengers 1.6T samples and the Globetronics production line ramp. Not by a short seller’s tax code analysis.

The transition from electrical to optical interconnects in AI data centers is happening whether POET succeeds or fails. Whether POET’s Optical Interposer can claim a position in that transition will ultimately be decided by the answers to the five questions raised above.

References & Sources

[1] Wolfpack Research, “We Believe POET Is A Obvious Stock Promote, Has Created An IRS Nightmare: US Holders Have Until April 15th To Act” - Published 2026.04.14, $POET short report (PDF, 10 pages)

[2] POET Technologies & Lessengers, “Expand Partnership to Deliver 1.6T 2xDR4 Optical Transceivers for AI Network Connectivity” - Published 2026.03.17, Q2 2026 sample target

[3] POET Technologies & LITEON Technology, Joint Development of Optical Modules for AI Applications - Published 2026.03.16, prototype target late 2026

[4] POET Technologies, Form 6-K Exhibit 99.2 - Q1 2025 interim disclosure, Globetronics Malaysia assembly/test line and fab-light strategy

Disclaimer: This article is an independent, engineering-driven technical analysis published by PhotonCap. All content is based on publicly available information and is intended for educational and informational purposes only. Nothing herein constitutes a recommendation to buy, sell, or hold any security. The author may hold positions in securities discussed and may transact at any time without notice. Readers should conduct their own due diligence before making any investment decisions.

Long POET since first tranche in April 2022. Too early, but continued to build to what is now an obesely overweight position in common and POET 01/15/2027 5.00 calls. Expect to sell the calls and perhaps the lion's share of the position as they get their 15 minutes in the not too distant future...

The PFIC filing is a PITA. We've already extended so will add a Form 8621 choosing the QEF option once the AIF is filed.

Apparently, even with a re-domicile to the US the PFIC is still in effect effecting future realized gains.

I would suggest “The second is a matter of time and execution, at a competitive cost.”