Chinese Optical Modules Own 7 of the Top 10 Seats. So Why Are Chip Companies Still Making the Money?

Assembly Powerhouse, Chip Desert: The Structural Limits of China’s Optical Module Industry

Seven of the global top 10 optical module suppliers in 2024 were Chinese companies (including Source Photonics, acquired by Chinese capital). Innolight and Eoptolink are estimated by industry sources to supply roughly 60% of NVIDIA’s 800G volume, controlling the critical plumbing of AI data center optical interconnects. Yet the DSP chips and EML lasers inside those modules are still held by Broadcom, Marvell, Lumentum, and Coherent. Being number one in shipments and number one in excess profit are not the same thing. This article examines how the Chinese optical module industry’s “assembly powerhouse, chip desert” structure was formed, what the Southeast Asian factory migration really looks like, and whether LPO and silicon photonics transitions can change the equation.

Contents

Introduction

How Chinese Optical Modules Became Number One

Value Chain Structure: Where Margins Diverge Between Modules and Chips

DSP and EML: Two Chokepoints

The Truth About Southeast Asian Factories: Tariff Avoidance or Real Manufacturing?

Can LPO/SiPh Change the Structure?

Closing

References & Sources

1. Introduction

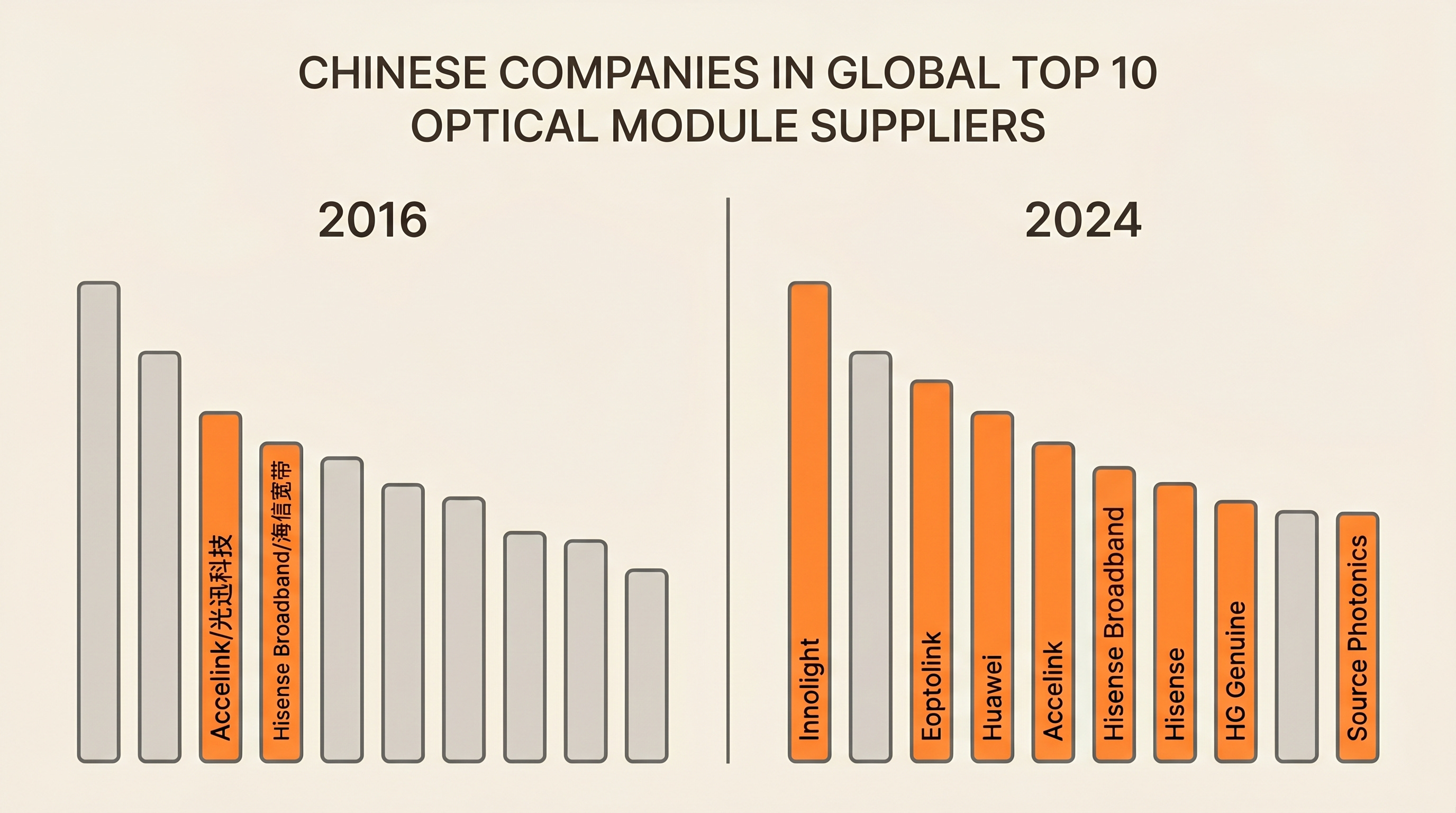

As recently as 2016, only two Chinese companies (Accelink and Hisense Broadband) made the global top 10 optical module supplier list. By 2024, that number had grown to seven.[1]

The landscape flipped in less than a decade. Innolight posted 2024 revenue of RMB 23.86 billion (roughly $3.3 billion), claiming the global number one spot.[2] Eoptolink recorded approximately 175% revenue growth the same year, jumping to third place.[1]

According to multiple industry sources, these two companies are said to have captured roughly 60% of NVIDIA’s 800G optical module volume. The remaining 40% is split among U.S. suppliers like Coherent and Lumentum.[3]

Surface-level market share and actual value chain control are different things. China leads the world in module assembly, but the critical chips inside are mostly imported. DSPs (Digital Signal Processors) are effectively a duopoly between Broadcom and Marvell, while high-speed laser chips (EMLs) are held by Lumentum, Coherent, and Mitsubishi.

The question is straightforward. China dominates modules. So why do chip companies keep the excess profit?

2. How Chinese Optical Modules Became Number One

The growth of China’s optical module industry breaks down into three phases.

Phase 1: Domestic market as training ground (early to mid 2010s)

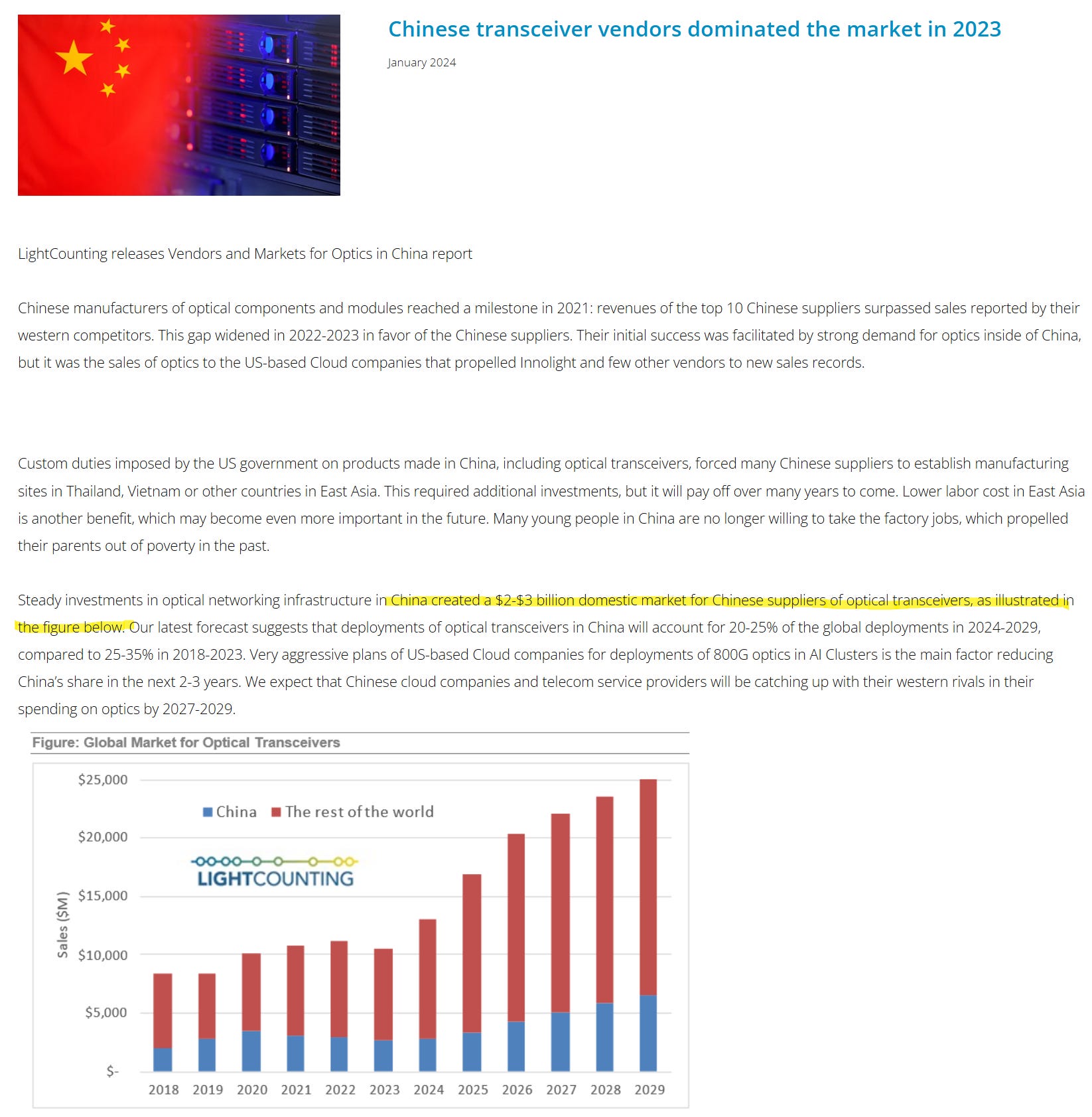

It started with 4G/5G infrastructure spending by China’s three mobile carriers (China Mobile, China Telecom, China Unicom). According to LightCounting, the Chinese optical transceiver market alone ran at $2 to 3 billion annually, and that volume became the soil for Chinese manufacturers to build mass production capability.[4]

Think of it this way: Chinese module makers first built muscle in a massive domestic “practice arena.” They produced 100G and 200G modules at scale, accumulating yield and cost advantages. That foundation later became their ticket to overseas markets.

Phase 2: Riding the North American cloud wave (early 2020s)

The turning point came when U.S. hyperscalers (Google, Amazon, Microsoft, Meta) began aggressively building out 400G data centers. This is where Chinese suppliers’ strengths shone: pricing, fast lead times, and volume production capacity.

Innolight established itself as a core supplier to Google and Microsoft, while Eoptolink embedded deeply into the AWS supply chain. Overseas revenue ratios surged. In Innolight’s case, overseas revenue accounted for 86.8% of 2024 total sales.[2] Most of that was North America.

Phase 3: AI clusters changed everything (2023 to present)

The number of optical modules needed per GPU in AI training clusters jumped significantly. Traditional servers needed two to four transceivers each. AI training clusters require multiple 800G links per GPU. Transceiver demand now scales proportionally with GPU demand.

The datacom optical component market is projected to exceed $16 billion in 2025, growing more than 60% year over year.[3] TrendForce projects 800G and above transceiver shipments to jump from 24 million units in 2025 to roughly 63 million in 2026, a 2.6x increase.[5]

Not many companies can handle that volume. Innolight and Eoptolink securing roughly 60% (industry estimate) of NVIDIA’s GB200-related 800G orders is not just about being cheap. There simply aren’t many suppliers that can deliver at this scale on schedule.

Here is a quick look at the key players.

Innolight posted 2024 revenue of RMB 23.86 billion (roughly $3.3 billion), making it the global number one.[2] It is widely understood to have very high exposure to North American hyperscalers, and industry channel checks suggest its 800G market share is among the highest. The company is also actively investing in SiPh and CPO. Eoptolink recorded RMB 8.65 billion (roughly $1.2 billion) the same year, with a strong presence in the North American cloud supply chain. It holds a leading position in LPO technology, and its 33% net margin is unusually high for a module assembler.[1]

Huawei is the global number one in telecom, but is focused on non-U.S. markets due to export restrictions. It is developing SiPh in-house. Accelink is one of the few vertically integrated (IDM) players in China, covering everything from chips to modules across both telecom and data center markets.

Behind them, Hisense Broadband holds a full chain from optical chips to terminal devices, HG Genuine has secured cost advantages through in-house EML chips and SiPh solutions, and TFC Optical specializes in optical components and connectors, delivering net margins close to 40%. TFC also collaborates with NVIDIA on CPO.

Looking at H1 2025 results, Innolight posted revenue of RMB 14.789 billion (+36.95%) with net profit of RMB 3.995 billion (+69.4%). Eoptolink was even steeper: revenue of RMB 10.437 billion (+282.64%), net profit of RMB 3.942 billion (+355.68%).[6]

Those growth rates are impressive. But here is the important question: who in this value chain is actually capturing the most profit?

Key point: The growth of Chinese optical module companies came from playing the “plumber” role in AI data centers. They don’t design the building, but the building doesn’t run without the plumbing. The question is where the critical components inside that plumbing come from.

What matters is not shipment volume but which layer retains the profit. China assembles the 800G modules, but the highest excess margins go to whoever controls the DSP and EML. That is what we need to examine.

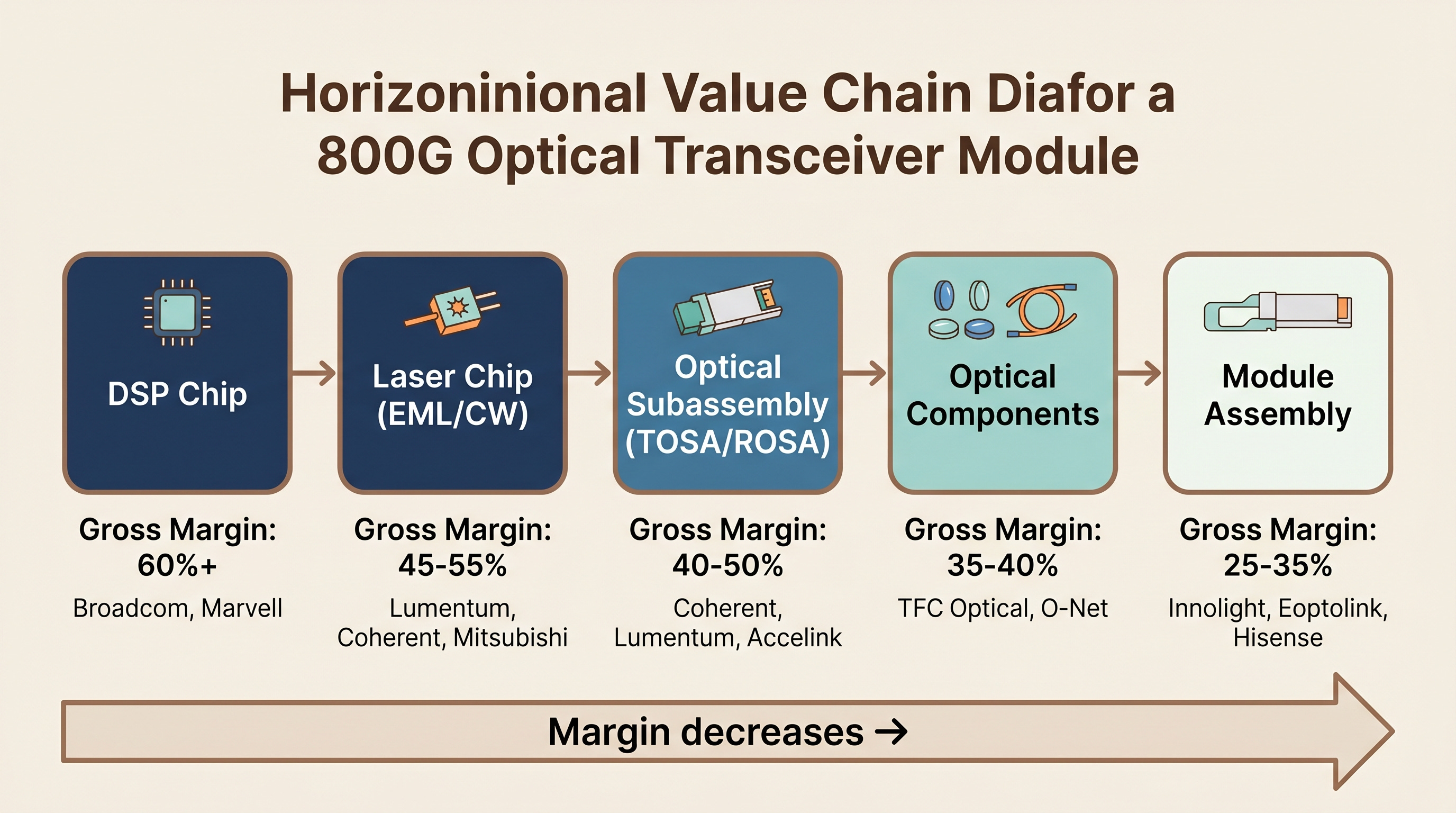

3. Value Chain Structure: Where Margins Diverge Between Modules and Chips

Break down a single optical module and you get four main components.

Laser source (EML, VCSEL, or CW laser): The core component that converts electrical signals to light. Think of it as the “engine” of the optical module.

Photodetector (PD): The receiver that converts light back to electrical signals.

DSP (Digital Signal Processor): The brain that cleans up signals, corrects errors, and aligns timing. Think of it as a highway traffic control system.

Optical components + PCB + packaging: Lenses, connectors, substrates, housings. Assembling these is the primary job of module companies.

This is where margin structures diverge sharply. Segment-level margins are not publicly disclosed, but company-level financials reveal the structural gap.

Starting with DSP chips: Broadcom’s company-wide GAAP gross margin is approximately 68% (FY2025). This figure includes the VMware software business, and the optical DSP segment margin is not broken out separately. Given the design IP-based, foundry-outsourced model, segment margins are presumably high, but exact figures are unavailable.

For laser chips (EML/CW): Lumentum’s company-wide GAAP gross margin was 28% in FY2025, rising to 34% by FY2026 Q1 as EML shipments surged. Coherent posted 35.2% for FY2025. Both companies mix optical components with industrial/materials segments, so the standalone EML chip margin could be higher or lower than the company average. InP epitaxy and processing require highly specialized fab technology.

Module assembly is the most transparent layer because Chinese module companies are publicly listed. Innolight posted 20 to 22% net margins in 2023 to 2024, and Eoptolink hit 33%, both all-time highs driven by the AI demand surge.[1] Meanwhile, TFC Optical, a component specialist, delivers net margins close to 40%. Even within the same optical value chain, the profit structures of components/chips and module assembly are clearly different.

One thing needs to be addressed here, though. Looking at 2023 to 2024 net margins, module companies actually outperformed chip suppliers. Eoptolink posted 33% and Innolight 22%, while Coherent and Lumentum ran at a loss or single-digit net margins on a company-wide basis over the same period. This looks like a contradiction, but it resolves once you separate the cycle from the structure. The current high margins at module companies come from temporary pricing power created by 800G capacity shortage. Demand is surging but only two or three companies can produce at this scale and schedule, giving module makers a pricing premium they would not normally have. Coherent and Lumentum, meanwhile, were weighed down by telecom weakness and M&A integration costs at the company level. That said, both are recovering fast as AI datacenter revenue kicks in. Lumentum posted +58% YoY revenue growth in FY2026 Q1, with GAAP gross margin climbing from 28% in FY2025 to 34%. Coherent improved non-GAAP EPS by +191% YoY in FY2025. Chip-side margin resilience is already kicking in. And the picture shifts further when the cycle normalizes. As 1.6T mass production ramps in 2026 to 2027 and second-tier players like Accelink and HG Genuine add capacity, module pricing will likely come under pressure quickly. Chip IP like DSPs and EMLs, by contrast, has a structurally limited number of alternative suppliers, giving these businesses stronger margin resilience through the cycle.

Selling the same 800G transceiver, the profit structure for a module assembler and a laser chip supplier look completely different.

Over the long term, what matters is not shipment volume, but where excess profit stays through the cycle. Module assembly has relatively lower barriers to entry. Even at the 800G/1.6T level, which requires sophisticated production capabilities, the structure of buying key components (DSP, laser) externally and assembling them is fundamentally “parts cost + assembly cost + margin.” As competition intensifies, margins compress. DSPs and EMLs, by contrast, have design IP and process know-how as their moats. With very few alternative suppliers, pricing power sits with the component makers.

Understanding this structure changes how you see the growth of Chinese module companies. Revenue and market share are dominant, but the highest-margin, hardest-to-replace layers in the value chain are still held by U.S. and Japanese companies.

There is one more variable missing here. Two components, DSP and EML. Look closely at the supply structure for these two, and what emerges is not just a margin gap but a question of who holds whose leash.

Key point: Chinese optical module companies are the best in the world at 800G/1.6T mass production. But the margin gap between upstream (DSP, EML) and downstream (module assembly) is structural. Module market share does not equal value chain dominance.

4. DSP and EML: Two Chokepoints

4-1. DSP: The Irreplaceable Brain

The DSP is the brain of the optical module. It converts high-speed optical signals to digital, filters noise, and aligns timing. In 800G transceivers, the DSP accounts for a significant portion of total module power consumption and is the key determinant of module performance.

This market is effectively a duopoly.

Broadcom: Sian2 DSP. The standard in NVIDIA’s supply chain. Used primarily by Innolight and Eoptolink.

Marvell: Spica (800G) / Ara (1.6T) PAM4 DSP families. Adopted by hyperscalers including Microsoft and Google.[14]

There is currently no mature Chinese domestic alternative for DSPs.[7] The DSP ecosystem has high IP barriers and a closed architecture. The issue is not just whether you can design a chip. PAM4 (Pulse Amplitude Modulation 4-level) signal processing algorithms, FEC (Forward Error Correction) IP, and years of accumulated customer-specific optimization data are all barriers to entry.

What is notable here is that this DSP dependency itself is why Chinese companies are aggressively pushing LPO (Linear Pluggable Optics). LPO removes the DSP from inside the module and has the switch chip handle signal processing instead. Eliminating the DSP reduces power and cuts dependence on Broadcom/Marvell. More on this in Section 6.

4-2. EML: The Physical Bottleneck

The EML (Electro-Absorption Modulated Laser) is the light source of the optical module. It is the core device that converts electrical signals to light, and is the most commonly used laser type in 800G and above single-mode transceivers.

A serious bottleneck is forming here.

According to TrendForce, NVIDIA has strategically pre-allocated production capacity at major EML suppliers, pushing EML lead times out past 2027.[5] From NVIDIA’s perspective, this is a rational move to secure stable supply for its GPU cluster modules. But it has made EMLs harder for everyone else to get.

Five companies dominate the EML market: Lumentum, Coherent, Mitsubishi, Broadcom, and Sumitomo (though Sumitomo has higher exposure to DFB/VCSEL than datacenter EMLs). For 200G/lane EMLs (the next-generation spec required for 1.6T transceivers), Lumentum is the most aggressive front-runner, while Broadcom and Coherent have also officially presented 200G EML capabilities.[8]

Chinese companies are attempting EML localization. Zetta Semiconductor announced a mass-producible 100G PAM4 EML at OECC 2025, and followed up with a 200G per wavelength PAM4 EML at ACP in November of the same year.[9] Changguang Huaxin has been supplying 56G PAM4 EMLs since 2023. Accelink is the only domestic company producing 25G EMLs in-house.[2] But mass production at the 100G/lane and 200G/lane level still has a long way to go. The domestic localization rate for 25G and above high-speed optical chips in China remains below 15%.[7]

The bottleneck structure is clear. DSPs are an effective duopoly between Broadcom and Marvell, with no mature Chinese domestic alternative. EMLs (100G+) are supplied by roughly five companies, with a Chinese localization rate below 15% and mass production still in early stages. CW Lasers from Lumentum, Yuanjie, Shijia and others are in relatively comfortable supply as the technology is mature. VCSELs are led by Broadcom (including Lumentum OEM) and the Coherent (formerly II-VI) family, with Chinese companies attempting to enter.

CW lasers are in a comparatively better position. Their simpler structure and larger supplier base mean that using CW lasers as external light sources in silicon photonics modules, instead of EMLs, is emerging as an alternative to the EML shortage.[5]

Key point: DSP and EML are the two structural dependency points for the Chinese optical module industry. DSP is a Broadcom/Marvell duopoly. EML is a physical supply shortage. Neither bottleneck is likely to be resolved in the short term, and this is the background for Chinese companies aggressively pushing LPO and silicon photonics.

5. The Truth About Southeast Asian Factories: Tariff Avoidance or Real Manufacturing?

Chinese optical module companies have been moving production to Southeast Asia for some time. The direct trigger was U.S. Section 301 tariffs (25% on Chinese-origin products).[4]

Looking at current overseas production bases: Innolight operates Thailand as its primary base for North American shipments and has added a Mexico facility. Eoptolink also uses Thailand as its main base, with 1.6T volume ramp-up in progress there. Hisense has facilities in Thailand alongside a direct production site in New Jersey, U.S. CIG and Linktel have production bases in Malaysia.

The logic is straightforward. Chinese-origin products face Section 301 tariffs (25%) directly, while products made in Thailand or Malaysia may face different treatment depending on country-of-origin determination and whether substantial transformation is recognized. That said, producing in Southeast Asia does not automatically mean non-Chinese origin classification.

The reality, however, is not that clean.

Issue 1: Components still come from China and Japan

Thai and Malaysian factories “assemble” modules, but a significant portion of key components (ceramic substrates, optical subassemblies, PCBs) are imported from China or Japan. Ceramic substrates, for example, often come from Japan’s Kyocera or Germany’s Heraeus. For the finished product to qualify as Thai in origin, “substantial transformation” must occur in Thailand.

Issue 2: U.S. CBP is stepping up enforcement

U.S. Customs and Border Protection (CBP) is intensifying its crackdown on Southeast Asian transshipment. Investigations into country-of-origin fraud, where Chinese products are relabeled in Southeast Asia for export, are underway, with Vietnam and Malaysia as primary targets.[10]

As of 2026, enforcement has intensified further. The DOJ launched a dedicated trade fraud task force in 2025, and CBP country-of-origin fraud investigations have been increasing in frequency.[11]

Issue 3: The ambiguous boundary of “substantial transformation”

For optical modules, whether the work done at Thai/Malaysian factories qualifies as “substantial transformation” is a gray area. It is unclear whether simply placing components on a PCB and putting them in a housing counts as “transformation,” or whether optical alignment, burn-in testing, and calibration must also be included. CBP makes determinations on a case-by-case basis, so risk remains for module companies.

In practice, the Thai factories of Innolight and Eoptolink perform processes well beyond simple assembly. Optical alignment, high/low temperature testing, firmware loading, and final inspection all happen in Thailand, so the “substantial transformation” argument is not entirely weak. But with U.S. policy trending toward stricter enforcement, this remains a variable to watch.

HG Genuine’s approach is also interesting. It claims that 400G single-mode products using in-house EML chips or silicon photonics solutions achieve $25 to 30 in cost savings compared to competitors.[2] The strategy is to absorb tariff impact through a combination of chip self-sufficiency and overseas production.

Key point: Southeast Asian factory migration is largely motivated by tariff avoidance, but substantial manufacturing processes have been relocated as well. However, component origin issues and intensifying U.S. CBP enforcement remain risk factors from 2026 onward.

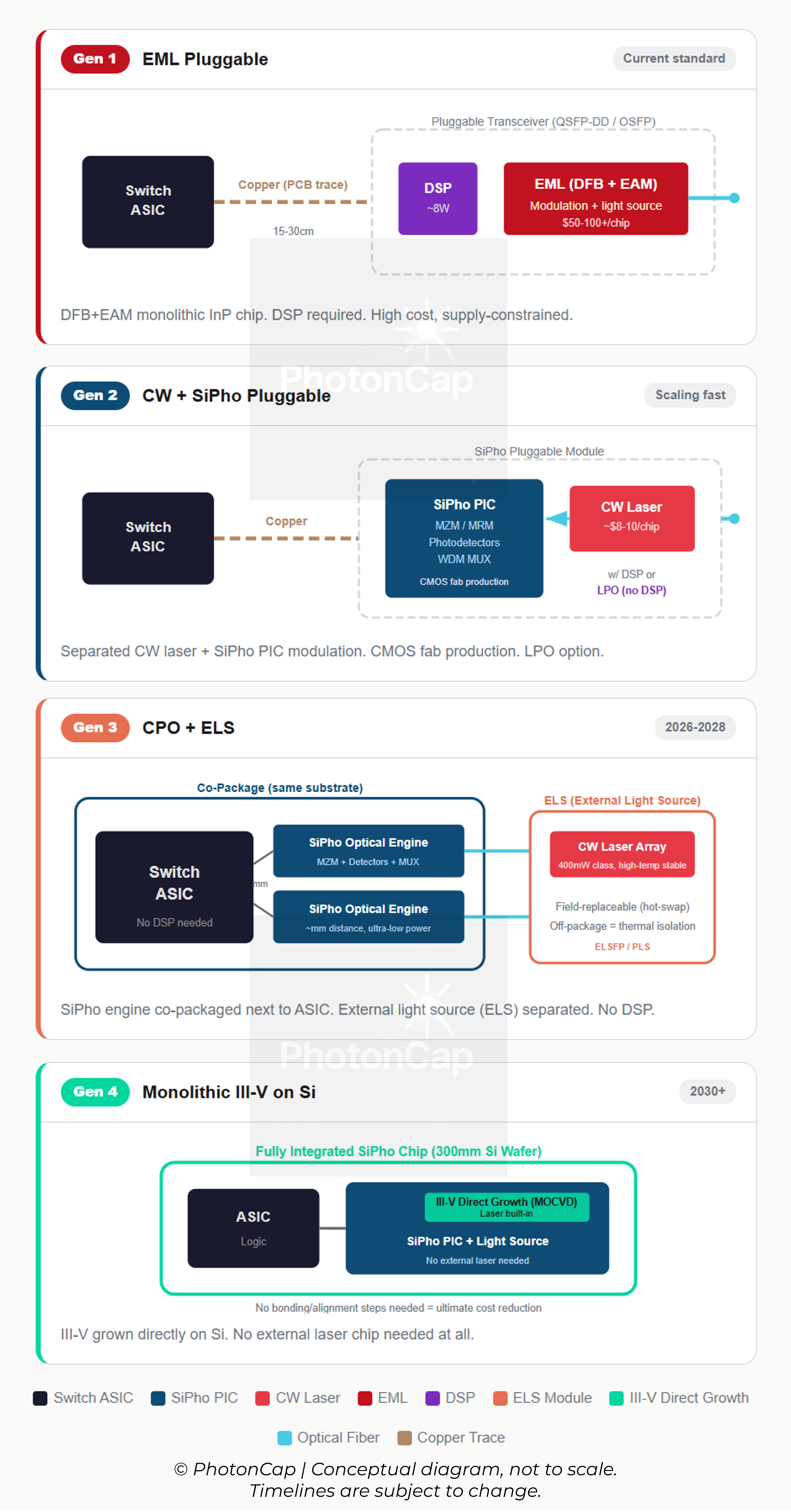

6. Can LPO/SiPh Change the Structure?

Tariff risk is a short-term variable. What changes this structure over the medium to long term is technology.

Three technology paths could alter the “assembly powerhouse, chip desert” structure: LPO, silicon photonics (SiPh), and CPO (Co-Packaged Optics). Each affects the value chain structure differently. The diagram below shows how light source architecture evolves across generations. Moving from Gen 1 (EML Pluggable) to Gen 2 (CW+SiPho) relieves the EML bottleneck. Moving to Gen 3 (CPO), the module itself disappears.

Figure 3: Light Source Architecture Evolution in Silicon Photonics

The Silicon Photonics Light Source War: Same Problem, Three Solutions (Small Cap)

Intro Sivers Semiconductors (OTCMKTS: SIVEF) surged +63.62% and QD Laser (TYO: 6613) jumped +33.39% over the past five days. What do these two microcaps have in common? They’re both light source suppliers for silicon photonics (SiPho).

6-1. LPO: Eliminating the DSP

LPO (Linear Pluggable Optics) removes the DSP from inside the optical module and has the switch chip handle signal processing instead. The module becomes “dumber,” but power drops and cost comes down.

Why Chinese companies are pushing LPO hard is clear.

DSP cost makes up a significant portion of module BOM (bill of materials). Removing it improves cost competitiveness.

Module-level BOM dependence on Broadcom/Marvell decreases. (System-level dependence remains, but the chip the module maker directly purchases is gone.)

Both Innolight and Eoptolink are founding members of the LPO MSA (Multi-Source Agreement).

But LPO is not a complete solution.

LPO does not eliminate Broadcom/Marvell dependence. It moves the DSP function from inside the module to the switch ASIC. The company making that switch chip is still Broadcom or Marvell. Module-level BOM dependence drops, but system-level silicon dependence remains. LPO also only works over short distances (mainly intra-rack, a few to tens of meters). Longer reaches still require DSP-based retiming. Standardization is also incomplete, requiring per-customer interoperability validation.

6-2. SiPh: Reducing EML Dependence

Silicon photonics (SiPh) integrates optical circuits on a silicon wafer. It can leverage existing semiconductor CMOS processes, making it favorable for mass production.

In SiPh modules, CW lasers (continuous wave lasers) serve as the external light source instead of EMLs, and modulation is handled by ring modulators or MZI (Mach-Zehnder Interferometer) modulators on the silicon chip. CW lasers are structurally simpler than EMLs and have more suppliers, enabling a workaround for the EML bottleneck.[5]

SiPh penetration in the 800G market was about 10% in 2024 and is expected to reach 20 to 30% in 2025. Industry estimates suggest it could reach 30 to 40% in 1.6T once the technology matures.[12]

Chinese companies’ SiPh capabilities are also coming up fast.

Innolight: Global number one in 800G SiPh module market share. SiPh mix above 40% in 2025.[13]

Eoptolink/Innolight: Some Chinese brokerage analyses estimate SiPh chip self-sufficiency above 80%, though official confirmation is limited.[13]

Accelink: Has SiPh subassembly capability through TOSA/ROSA vertical integration.

But SiPh foundries (wafer fabrication) are still centered in the U.S. and Europe. GlobalFoundries (GFS), Tower, and TSMC are the major foundries, and SiPh-dedicated foundry capacity in China is still at an early stage.

6-3. CPO: Questioning the Module Maker’s Reason to Exist

CPO (Co-Packaged Optics) places the optical engine inside the same package as the switch chip. The transceiver module disappears entirely, and optics move down to the chip level.

NVIDIA’s unveiling of its own CPO switch at GTC 2025 made this direction concrete. At the time of the GTC 2025 announcement, a 3.5x improvement in power efficiency over conventional pluggables was presented. NVIDIA’s current product page now claims 5x improvement.[14][15] Network resiliency improves 10x, resulting in 5x sustained application runtime. NVIDIA targets Spectrum-X Photonics for commercial availability in 2H26.

If CPO becomes widespread, the role of optical module assemblers fundamentally changes. Pluggable modules shrink, and optical engine plus chip packaging capability become what matters. This favors chip companies like Broadcom, Marvell, and NVIDIA.

That said, CPO is unlikely to replace pluggables quickly. It is currently applied only in specialized AI cluster environments. General-purpose data centers still prefer the flexibility of pluggables (easy swap, upgrade). Commercial deployment begins in 2026, but pluggable shipment volumes are unlikely to drop significantly over the next three years. CPO and pluggables will coexist for a substantial period.

Summary: How the Three Technologies Affect Chinese Companies

LPO favors maintaining “assembly powerhouse” status. Removing DSP cost lowers module cost. But it only partially addresses “chip desert.” The dependency shifts from the module-internal DSP to the switch chip, and it only works over short-reach links. SiPh also favors the “assembly powerhouse” direction. It leverages CMOS mass production capability and routes around the laser bottleneck by using CW lasers instead of EMLs. But SiPh foundries (GFS, Tower, TSMC) are overseas, so the form of dependency changes rather than disappearing. CPO is the opposite. It reduces demand for module assembly itself, making it unfavorable for Chinese module companies over the medium to long term. CPO is a domain led by chip companies (NVIDIA, Broadcom, Marvell).

In the end, LPO and SiPh are favorable for Chinese companies in the near term. SiPh in particular can route around the EML bottleneck while using CMOS production capability, which is precisely why Innolight and Eoptolink are investing heavily. But if CPO expands over the medium to long term, a structural shift that reduces the value-add of “module assembly” itself could arrive.

Key point: LPO and SiPh lower Chinese optical module companies’ DSP/EML dependence, but dependence on the top of the value chain (chip IP, foundries) does not fully disappear. CPO is the medium-to-long-term variable that could redefine the role of module companies altogether.

7. Closing

In the span of a decade, Chinese optical module companies have claimed 7 of the top 10 seats and secured core supplier status in the AI demand segment. Thanks to the 800G capacity shortage, module companies are currently posting higher net margins than chip suppliers. When the cycle is good, even the plumber makes money.

But cycles do not last forever. As 1.6T mass production ramps and second-tier players add capacity, module pricing will inevitably come under pressure. DSPs, EMLs, and foundries, by contrast, have a structurally limited number of alternative suppliers, giving them stronger margin resilience when the cycle turns. Over the long term, excess profit stays not in assembly, but in chip IP.

Optical interconnects in AI data centers are moving closer and closer to the chip level, and that direction will redraw the division of roles between China and the U.S.

8. References & Sources

[1] 2024 Global Top 10 Optical Module Suppliers : LightCounting 2024 global optical module Top 10 rankings and Chinese company performance

[2] Optical Communications Industry Deep Dive : Chinese optical module company 2024 financials and technology overview (Chinese brokerage research compilation)

[3] Pluggables, Power, and Geopolitics: 800G/1.6T Optical Transceiver Battle : 800G market size, NVIDIA supply chain Chinese company share estimate (secondary analysis)

[4] LightCounting: Chinese transceiver vendors dominated the market : China domestic market size $2-3B, Southeast Asia factory migration background

[5] TrendForce: AI Data Centers Ignite Laser Shortage : 800G+ shipment projections, NVIDIA EML pre-allocation, CW laser as alternative

[6] Nvidia Orders Surge: InnoLight and Eoptolink Dominate 800G : Eoptolink H1 2025 financials (+282.64%), 1.6T product status (industry channel information)

[7] CIOE: DSP bottleneck and optical chip localization : DSP localization bottleneck, 25G+ optical chip localization rate discussion

[8] Top Silicon Photonics Stocks 2026 : EML market structure overview (secondary analysis)

[9] Zetta Semiconductor: 100G PAM4 EML Breakthrough : Mass-producible 100G PAM4 EML (OECC 2025)

[10] US Tariff Updates: China, Southeast Asia scrutiny : CBP transshipment crackdown, country-of-origin fraud investigation trends

[11] DOJ: Trade Fraud Task Force : DOJ/DHS trade fraud task force launch

[12] Optical Module Market Deep Dive : SiPh penetration projections (800G 20-30%, 1.6T 30-40%, secondary analysis)

[13] Optical Module Research Notes : Innolight SiPh mix estimates, company-level supply chain details (Chinese brokerage channel check)

[14] Marvell PAM4 Optical DSP Portfolio : Marvell PAM4 DSP product lineup (Spica, Ara, Nova, Perseus)

[15] NVIDIA Silicon Photonics: CPO Product Page : NVIDIA CPO 5x power efficiency, 10x resiliency improvement (current product spec)

[16] The Silicon Photonics Light Source War: Same Problem, Three Solutions (Small Cap): PhotonCap’s Article

Disclaimer: This article is an independent, engineering-driven technical analysis published by PhotonCap. All content is based on publicly available information and is intended for educational and informational purposes only. Nothing herein constitutes a recommendation to buy, sell, or hold any security. The author may hold positions in securities discussed and may transact at any time without notice. Readers should conduct their own due diligence before making any investment decisions.

I think people are saying the the pluggable optical transceiver is still needed for CPO. But more chips moving from the transceiver to CPO package on board.

But you need to fit the EML in the transceiver and other chips and components to transmit that data to other PCB chipsets.

Nobody seems to know how the value chain will shift tectonically in the CPO high penetration era.

But innolight and eoptolink share price, based on forward P/E valuation do not seem to suggest value compression in CPO era in the 1.6T

I don’t know the answer yet. Maybe it’s just A-Share AI concentration premium that A-share investors don’t care about 1.6T massive transition. That’s 2H2027 growth story.

I'm surprised that you haven't mentioned $FN in the context of module assembly. Do I understand correctly that that's the only non-Chinese assembler? Where do they fit in this structure?