A $750M Fabless Chip Company, and the Foundry That Makes the Chips

Credo's $750M DustPhotonics Deal, Astera Labs' aiXscale Acquisition, and the Beneficiary No One Is Watching

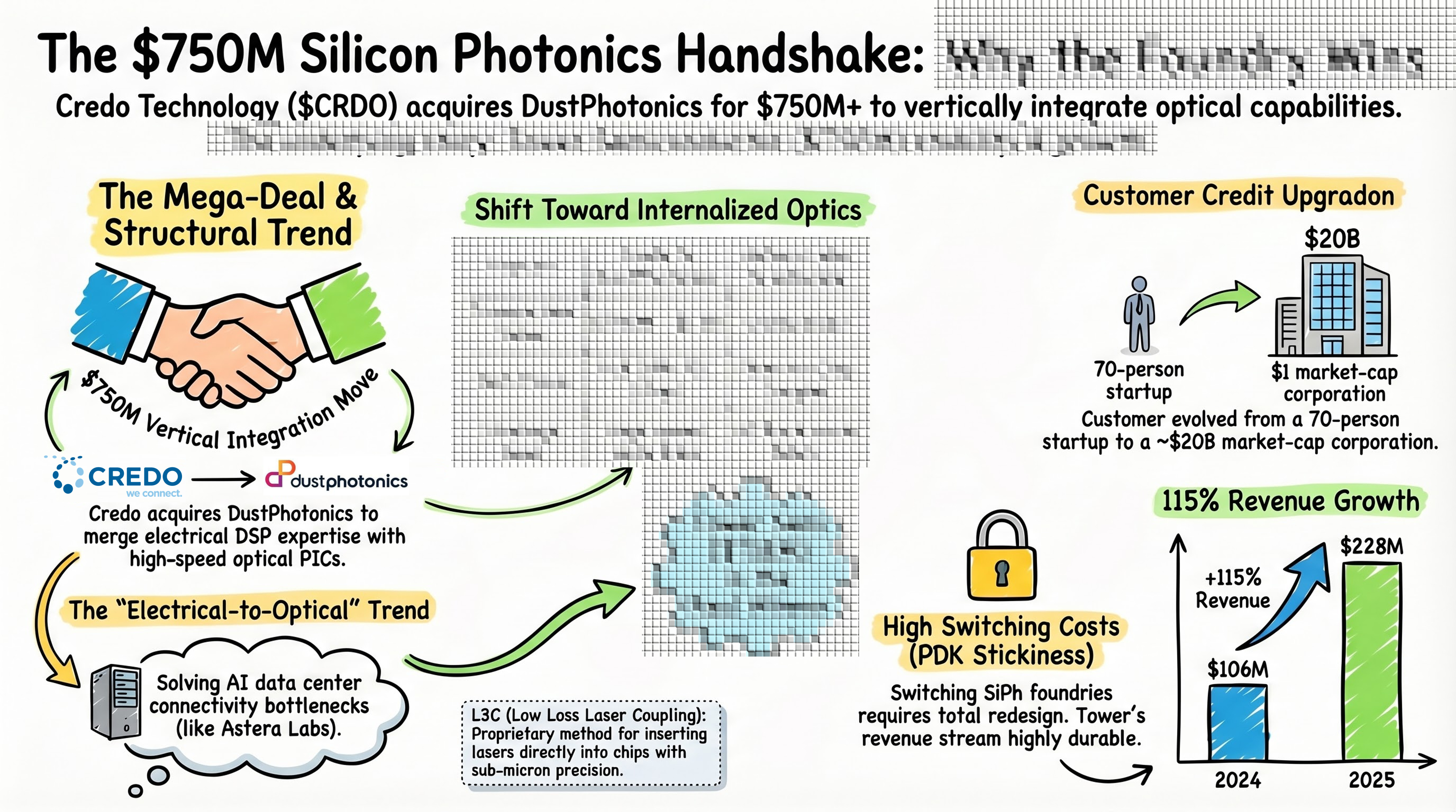

DustPhotonics, an Israeli silicon photonics (SiPh) startup that raised $100M in total funding, has been acquired for $750M (up to ~$1.3B including earnout). The buyer is high-speed connectivity company Credo Technology (NASDAQ: CRDO). This article examines the verification limits of DustPhotonics’ core L3C (Low Loss Laser Coupling) technology, compares the deal to Astera Labs’ acquisition of aiXscale Photonics, and analyzes the real significance of this deal from the perspective of the fabless SiPh PIC model and foundry Tower Semiconductor (NASDAQ: TSEM). Conclusion: the most stable beneficiary of this acquisition is not the company that designed the chip, nor the company that bought it, but the foundry that manufactures it.

$CRDO, $TSEM, $ALAB

Contents

Intro

Who Is DustPhotonics?

L3C Technology: What We Know and What We Don’t

Deal Structure and Credo’s Logic

The TSEM Angle: The Foundry Is the Real Beneficiary (paid)

Scenario Analysis (paid)

Monitoring Points (paid)

Closing

References & Sources

1. Intro

A $750M SiPh acquisition deal just dropped. But the company that stands to benefit the most doesn’t even appear in the headlines [1][2].

On April 13, Credo Technology (NASDAQ: CRDO) announced the acquisition of DustPhotonics, an Israeli company specializing in silicon photonics PICs (Photonic Integrated Circuits) [1]. CRDO shares jumped more than 10% in after-hours trading [3]. A startup that raised $100M in total funding just sold for $750M in cash [2].

Everyone is focused on Credo’s vertical integration strategy and DustPhotonics’ L3C technology. But this article won’t make any definitive assessment of the technology. The reason is simple. L3C’s performance data has never been publicly disclosed. No academic papers, no coupling loss figures, no peer review. And in October 2025, Astera Labs ($ALAB) made a similar move by acquiring German optical startup aiXscale Photonics [20]. A structural trend is forming: electrical connectivity companies are buying their way into optics.

The more important axis in this article is Tower Semiconductor ($TSEM). DustPhotonics is a fabless company (no in-house manufacturing), and all its wafers are fabricated at Tower. This relationship is five years old [4]. The real question isn’t about DustPhotonics. It’s about which fab is making these chips, under what cost structure, and for how long. If you’ve been following our previous TSEM analysis, you can probably sense where this is heading [5][6].

The market reaction lands on Credo. The supply chain profit is read at Tower.

Key takeaway: A $750M acquisition. Unverified technology. The trend of electrical companies buying optics is accelerating. The real question isn’t who makes this fabless SiPh chip, but where the orders show up as revenue first.

2. Who Is DustPhotonics?

DustPhotonics was founded in 2017 in Modi’in, Israel [7]. Its chairman is Avigdor Willenz, a serial exit legend in Israel’s semiconductor scene. He previously sold Habana Labs to Intel and Annapurna Labs to AWS [2].

Understanding the four co-founders is key to understanding the technology.

Yoel Chetrit (Chief R&D Officer): Came from Intel’s Photonics Technology Lab. He worked directly on silicon MZI modulators (Mach-Zehnder Interferometers, structures that create signals using phase differences in light) and WDM (Wavelength Division Multiplexing) chips under Mario Paniccia’s group. He has multiple publications from his 2006-2008 tenure at Intel [8][9]. In short, an engineer who personally understands SiPh device physics and process.

Dr. Kobi Hasharoni: From Compass Networks (later Compass-EOS). He researched SiPh-based router optical interconnects and co-authored a paper on 1.3 Tb/s parallel VCSEL optical links [10].

Amir Geron: Also from Compass Networks, alongside Hasharoni [2].

Ben Rubovitch (former CEO): From Mellanox and Amphenol TCS, with a manufacturing/operations background [11].

In its early days, the company built 100G/400G multimode pluggable transceivers. They even set up a production line in Thailand. But orders didn’t come. In CEO Lovinger’s words, “We shipped thousands, not hundreds of thousands” [11]. In 2021, DustPhotonics shut down the transceiver business and pivoted to becoming a SiPh PIC specialist. About 80 employees were let go during this restructuring [7], and the CEO changed from Rubovitch to Ronnen Lovinger, who had been SVP Operations at Mellanox and COO at Innoviz [11].

After the pivot, DustPhotonics became a “merchant SiPh PIC” company, selling chips to transceiver makers rather than building its own modules. The product lineup includes the Carmel (400G/800G), Oz (224G/lane, DR4/DR8), Tamar (FR4, integrated WDM mux), and Kfir series, with a roadmap extending to 3.2T [1].

Here’s the important point. All of DustPhotonics’ wafers are manufactured at Tower Semiconductor. CTO Chetrit said they chose Tower “for its mature PDK and flexible process” [11]. CEO Lovinger said he has “been working with Tower for five years” [4]. Assembly and testing are handled by Fabrinet [11].

Total funding exceeds $100M, with key investors including Greenfield Partners, Sienna Venture Capital, Exor Ventures, Atreides Management, and Intel Capital in the earlier rounds [2][7][12].

Key takeaway: DustPhotonics is a fabless SiPh PIC company built by engineers from Intel’s SiPh group. After a failed transceiver business, they pivoted to PIC-only and have been manufacturing on Tower Semiconductor’s fab for five years.

3. L3C Technology: What We Know and What We Don’t

DustPhotonics’ core technology is L3C (Low Loss Laser Coupling), a proprietary laser integration method [13].

One of the hardest problems in silicon photonics is getting light into the chip. Silicon cannot generate light on its own, so you need to deliver light from an external laser (typically an InP-based DFB laser) into a silicon waveguide (a pathway for light on the chip). If light is lost during this transfer, the entire system’s performance suffers. Think of it like plumbing: the joint between the faucet (laser) and the pipe (waveguide) is where leaks happen.

Based on publicly available information, here is what L3C does [13][14]:

Off-the-shelf DFB lasers are inserted into a trench etched on the PIC using low-cost automated assembly equipment

Butt-coupling (directly pressing the laser output facet against the waveguide input) is applied with sub-micron precision

The entire TX (transmit) optical chain has zero free-space sections (no gaps where light passes through air)

A single laser can be split across 4 channels. For the 800G-DR8 short-reach version, a single laser covers all 8 channels [14]

The Carmel-8 PIC consumes less than 1W total in a 7.5mm x 7mm package [15]

With no free-space gaps, the PIC is compatible with immersion cooling environments [15]

That’s what we know. What we don’t know is a longer list.

Coupling loss: No figures in dB have ever been disclosed

Spot size converter design: Unknown

Alignment tolerance: Only described as “sub-micron.” No quantitative data

Laser mounting orientation: Epi-up or epi-down is undisclosed

Bonding method: Solder or epoxy is undisclosed

Academic publications: No peer-reviewed device papers under the DustPhotonics name have been publicly identified at OFC, ECOC, CLEO, or comparable venues

Patents: Multiple patents are registered under DustPhotonics on Justia [16], but the technical details require direct patent document analysis

CEO Lovinger gave a Market Focus session talk at ECOC 2024 titled “Silicon Photonics operating at 1.6 Tb/s in an Immersion Cooling Environment” [17]. This was an industry talk, not a peer-reviewed technical paper.

To be clear, this does not mean the technology is bad. A startup choosing not to publish its core IP in journals is a perfectly rational IP protection strategy. But for external investors, it means independent technical verification is not possible. Credo paying $750M means the technology passed Credo’s due diligence. It does not mean that due diligence is available for external review.

Key takeaway: L3C is a butt-couple-based laser integration technology, protected by patents. Based on publicly searchable sources, no peer-reviewed device papers under the DustPhotonics name have been identified. With performance data undisclosed, independent assessment of technical differentiation is difficult.

4. Deal Structure and Credo’s Logic

Let’s start with the deal structure.

Upfront: $750M cash + approximately 0.92 million shares of Credo common stock [1]

Earnout: Up to approximately 3.21 million additional shares upon achievement of financial milestones [1]

Per Calcalist, the total deal value including earnout at current share prices is approximately $1.3B [18]

Expected to be non-GAAP EPS accretive in Credo’s FY2027 (May 2026 to April 2027) [1]

Expected closing: Q2 calendar 2026, subject to regulatory approval [1]

Credo’s strategic logic is straightforward. Credo has been an electrical connectivity company, selling SerDes IP and DSPs. Put simply, they specialize in moving data between chips at high speed inside data centers. Adding DustPhotonics’ SiPh PICs (the “optical” side) to this creates a vertically integrated stack from electrical signal to optical signal [1].

Credo posted single-quarter revenue of $407M in Q3 FY2026 (ended January 2026), growing 201.5% year over year [19]. They were already selling ZeroFlap optical transceivers and Optical DSPs, but SiPh PICs were externally sourced. This acquisition brings that in-house.

Credo expects its combined optical portfolio (ZeroFlap transceivers + Optical DSPs + SiPh PICs) to generate more than $500M in optical revenue in FY2027 [1]. According to LightCounting and Credo estimates, the SiPh PIC market is expected to grow to $6B by 2030 [1].

So where in this structure is the most advantaged position?

Even after Credo acquires DustPhotonics for vertical integration, the fab making those chips is still Tower. DustPhotonics is fabless [1], with no manufacturing facilities of its own. And as volumes grow, Tower’s SiPh fab revenue follows.

There’s a missing variable here. It’s foundry switching cost. SiPh PDK switching costs are significantly higher than CMOS PDK switching costs. Optical structures (waveguide geometry, modulator design rules, coupling architecture) are optimized for a specific fab’s process. Switching fabs effectively means redesigning the PIC from scratch. And Credo isn’t the only one making this kind of move. In October 2025, Astera Labs acquired aiXscale Photonics, moving in the same direction [20]. One question remains. Where does this optical internalization trend show up in the numbers first?